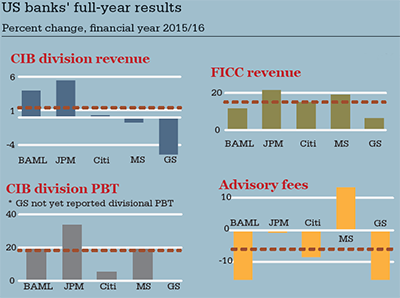

CIB revenues rose at JPMorgan, Bank of America Merrill Lynch and Citi (just), but fell a bit at Morgan Stanley. A tough year for equities, equity capital markets and advisory always adds up to a tough year for Goldman Sachs, so it was no surprise that revenues fell most there, by 5.5%.

However, cost-cutting and lower provisions meant that pre-tax profits at the CIB divisions rose overall by 19%, although these figures exclude Goldman Sachs, which does not report the profitability of its divisions until it files its 10-Q with the SEC in the coming weeks. JPMorgan topped the pile, with a 34% rise, having topped the FICC revenue gains and avoided a drop in equities.

|

|

|

|

|

Source: Bank earnings announcements. Results exclude |

The banks made more of their overall profit from CIB than they had in 2015. The $56 billion total profit those divisions generated, again excluding Goldman, was about 53% of total profits, compared with 47% the year before.

At a group level, revenues fell overall by 2%, although with very mixed performances. Goldman and Citi fell, JPMorgan was up a little, while BAML and Morgan Stanley were fairly flat. As with the CIB divisions, profits showed a different picture, however, with everyone rising, except Citi, and an overall gain of 6%. Goldman’s 19% rise stood out.

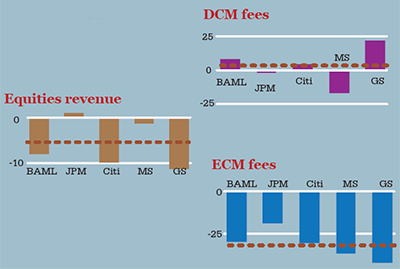

The corporate and investment bank product lines were not a pretty sight in 2016. In fact the only product that saw revenues rise year-on-year was fixed income – mostly in sales and trading but also with a small gain in DCM.

Fixed income sales and trading revenues were up by about 15%, with all five banks registering gains. This was enough to outweigh the equities fall and lead to overall sales and trading revenues climbing by 7%.

JPMorgan was up the most in FICC, by 21%, although it is worth noting that Morgan Stanley pulled off an outsize gain of more than 150% in its FICC division in the fourth quarter of 2016, albeit from a very low base one year earlier. On an annual basis, Goldman Sachs recorded the lowest gain in FICC, of just 6%, but it still made more than Morgan Stanley, even with the latter’s 19% rise.

Debt capital markets underwriting fees showed a less spectacular performance, up just 4% year on year. Goldman saw a whopping 22% gain, while Morgan Stanley could not replicate its secondary markets performance in primary, seeing its fee revenue fall 17%. The others were either flat or up.

DCM apart, the story of the year was one of falling investment banking revenues, with ECM fee revenues down 32% year-on-year and advisory falling by 6%. All banks saw big falls in ECM, with Goldman down by 42% and most of the others not far behind. The least affected was JPMorgan, dropping 19%, but still managing to be the only bank to break through the $1 billion mark for fees.

Advisory was a similar story. Here Morgan Stanley was the only firm to see a gain in fees, of 13%. BAML and Goldman were down about 15% – although, at $2.9 billion, Goldman still accounts for about one-third of the overall pot. The result was that all investment banking product revenue fell by almost 8%.

Overall, the picture is not good in terms of momentum. Taking FICC, equities, DCM, ECM and advisory, in 2016 each bank was up in two, down in three, on a full-year basis.

The reason for optimism lies in the fourth-quarter numbers. Over that period BAML, JPMorgan and Citi were up in three, with equities accounting for most of the difference. Morgan Stanley rose in four, while Goldman lagged with just two increases.

Headcount fell in 2016 by 1.5%. A year ago, the big five employed 772,000 staff. Twelve months later, 11,000 of them have gone. Goldman and Citi have hacked away the most, losing 5% to 6%, while JPMorgan has added 4%. The real pain on the cuts happened in 2015, however. Some 30,000 have left since the first quarter of 2015.