“The fun part is meeting the collector, going in their home and seeing amazing museum-quality works. I can’t tell you the number of people who told me: ‘I want your job’. Well, my job is more than just that. But it is very enjoyable. When you get into a person’s sacred place – their home – and start talking art, they really view you as a trusted confidant.”

Tall and angular, with a tidy shock of white hair and an aquiline nose, John Arena does indeed have one of those jobs you quietly covet. Put it in the basket along with ice-cream taster, Lego sculptor and professional sleeper.

His official title at Deutsche Bank International Private Bank Americas is ‘Subject matter expert for fine art lending’.

It’s a slightly unwieldy designation that, distilled, means ‘lending to rich people against their art collection so they can buy more art’ or splashing that additional cash in myriad other ways, from investing in a family firm, to gifting assets or capital to loved ones.

When we speak via Zoom, Arena is at his home in Miami, preparing to board a flight for Los Angeles.

He’s going there to attend Frieze, the celebrated contemporary art fair that bounces each year between LA, New York and London. This year, it lasts for three days from February 17, and it’s the 19th year in a row that Deutsche has been the event’s lead global partner.

Fine-art lending

Three factors emerge from our hour-long conversation.

The first is that he is a good listener. Arena has surely heard every art-related question under the sun, yet his responses are trim and data packed.

I’ve dealt with plenty of family office managers and very-high-end billionaires who aren’t familiar with art borrowing

John Arena, Deutsche Bank

![John-Arena-Deutsche-Bank[1]-480.jpg](https://altmedia.euromoney.com/dims4/default/368436d/2147483647/strip/true/crop/480x760+0+0/resize/800x1267!/quality/90/?url=https%3A%2F%2Faltmedia.euromoney.com%2Fc1%2F04%2Fa7461582489eae5fc5277772aeb6%2Fjohn-arena-deutsche-bank1-480.jpg)

He’s an aesthete but not a snob: his office wall is cluttered with paintings, but on further inspection, most are by his wife. They’re good, too: he points to a surrealist portrait of a lady with an elongated face and compares it, not unreasonably, with Modigliani.

The second is the shock of how little is known about this compelling corner of private banking.

Asked how much ultra-high net-worth (UHNW) individuals know about fine-art lending – particularly those liquid enough to saunter into Frieze and walk away with a daub that costs more than a penthouse on New York’s Park Avenue, he chuckles.

“The simple answer is it’s not as well-known as you may think. A lot of collectors do not grasp how to leverage against their art. I’ve dealt with plenty of family office managers and very-high-end billionaires who aren’t familiar with art borrowing.”

To illustrate his point, Arena recalls a dinner he attended late last year.

“The guy next to me had an art collection but was afraid of borrowing against it. I asked him what he was afraid of, and he replied: ‘That I could get overleveraged and lose it all’. I told him he misunderstood what an art lender does; that I want to protect his collection.”

The aim, he stresses, is to match the loan to the individual. Too large, as a share of personal assets, and it exposes the borrower to potential financial stress; too small, and he and Deutsche will have to weigh up if it’s worth their while.

“I would never make anyone a loan if it put their collection at risk,” he insists.

Secured market

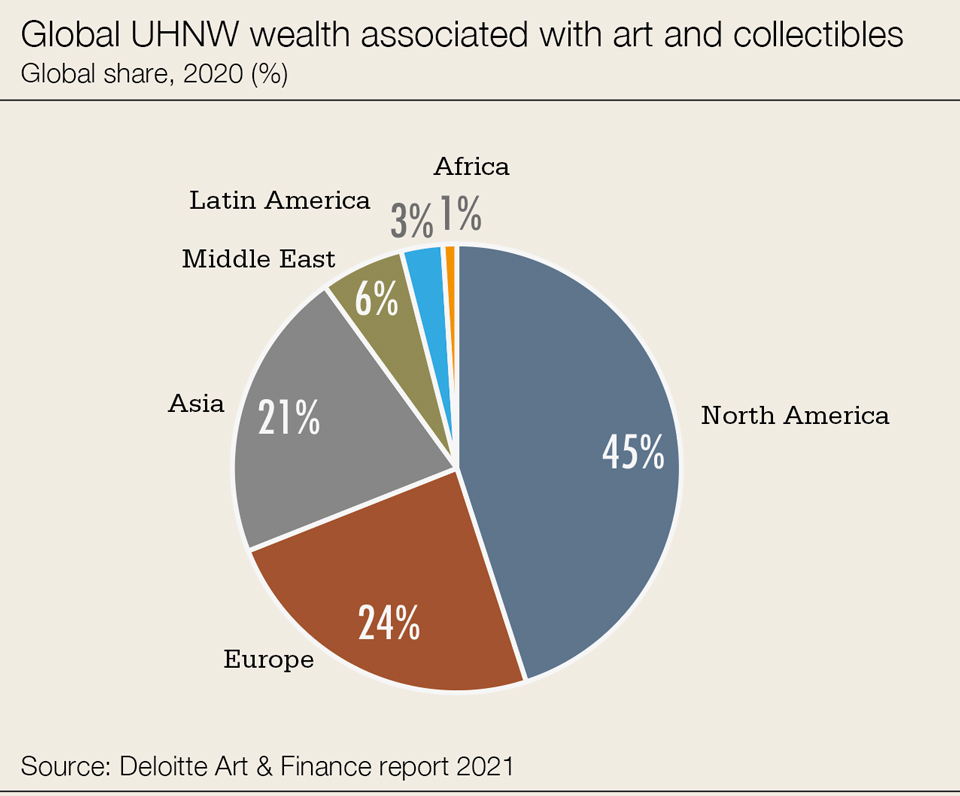

The final factor is how integral art lending has become to big private banks. In its latest Art & Finance report, Deloitte put the total personal wealth of UHNW owners of art and collectibles at $1.49 trillion in 2020. It projected the art-secured lending market to be worth $31.3 billion in 2022, up 11% year on year.

What makes this private wealth service so compelling for Deutsche, or its main competitors in this space – JPMorgan, Bank of America and Citi – is its ability to drive deal-flow and business across multiple divisions and product lines.

Any serious collector likely has relationships with several financial institutions, sprawling across wealth management, investment banking and corporate banking.

So, Arena’s role is not just to generate new business, but to drive value through Deutsche. “We refer clients across the bank,” he says. “I’ll be in New York in a couple of weeks, where I’ll meet with one of the investment heads to talk about how our team, particularly in the art-lending space, can help to cross-fertilise business in other parts of the bank.”

What Arena and his peers at rival lenders do – take JPMorgan’s art curator Charlotte Eyerman, or Citi’s global head of art advisory & financing Suzanne Gyorgy – is not rocket science. Arena himself admits as much.

“When you make things complicated, people have a hard time understanding. I’m not saying art lending is an easy proposition, but it’s a simple proposition. And simplicity is the key to being able to sell and structure that proposition.”

Once an art collection is appraised – Arena likes to use third-party experts at auction houses such as Sotheby’s or Christie’s – he gets to work. If a collection is worth $50 million, Deutsche will typically disburse a loan worth up to 50% of the assessed value, or $25 million. It is typically structured as an interest-only revolving line of credit, allowing the client to draw against the facility at will.

The trickier part of Arena’s job is getting business through the door in the first place.

You might think it easy to figure out who owns a lot of art. You’d be wrong. The obvious names are well known, but there is no complete database out there. Collections grow and wither over time, mirroring life and the wealth cycle.

Listening – always having your antennae working – helps a lot. Arena recently found himself deep in conversation with an ultra-wealthy individual, who suddenly mentioned his love of the Impressionists.

“We didn’t even know he had a collection,” Arena says. “It turned out it was worth over $400 million. He never listed it in a financial statement because he didn’t look at it as a financial asset. He looked at it as the aesthetic value of what he bought it for.”

As you’d expect, there is no ‘normal’ day in Arena’s line of work. There’s a lot of emails and phone calls. But he describes serving UHNWs as a “unique proposition”, with credit solutions “personally tailored” to the individual’s exacting needs.

Guarded assets

Deutsche doesn’t lend to just anyone with a few frames on their wall. It’s rare for a private bank to foreclose on a personal loan made against a private collection. Arena can’t remember it ever happening – and he’s been in the business for 27 years.

That’s mainly because he deals with one of the most zealously guarded assets in the lives of the super-rich. He reckons the typical collector has a minimum net worth of $100 million, of which up to 15% is invested in art. That number extrapolates upward, to $1 billion/$150 million, $10 billion/$1.5 billion, and so on.

Once the rich get the art bug, they tend to stay smitten.

“UHNW clients are collectors, and the definition of a collector is they have no more wall space: they love to buy art, they’re always adding to their collection,” he says.

So, Arena’s depiction of art lending as a “simple proposition” is a bit misleading. To assemble a revolving line of credit for a client is basic work. Once created, it sits there until the client suddenly needs liquidity and draws it down, partially or in full.

But getting to that stage is anything but straightforward. Because credit solutions are tailored, they require lots of calls with a client, their lawyers and family offices, and so on. When dealing with a client, particularly a new one, Arena looks at their entire portfolio.

Should client and collection press all the right buttons, the bank will look to go ahead with a loan.

But, Arena adds, “if they have an art collection that isn’t qualified in terms of what we would lend against when analysing the financials, we will seek to offer a different credit solution, but not necessarily against their art.”

There are no hard and fast rules. The market is secretive, unregulated and financially opaque. To make good decisions critical to bank and client, the pivotal figure – Arena, in this case – must be good with numbers and know the industry’s key players.

Throughout our conversation, his love of art shines through, as does his passion for old movies. His favourite film is ‘Casablanca’, with ‘The Wizard of Oz’ a close second. With commendable understatement, he describes Vincent van Gogh’s ‘The Starry Night’, part of the permanent collection at New York’s Museum of Modern Art, as “pretty good”, and the painting he would take with him to the proverbial desert island.

Great art, he insists, changes the observer for ever. No one who gazes upon a Vermeer or a Rothko ever forgets the experience.

“When you see an iconic work of art up close in person, it will resonate with you. It will speak to you, and you’ll feel it.”

Thus speaks a man who clearly cannot wait to get up every morning to do a job that many want.

The art of the deal

The first big financial institution to actively lend against art on behalf of wealthy clients was Citi, back in the 1970s. But it was all a little ad hoc at first. Only later did private banks begin to bring structure and direction to the market.

John Arena joined Citi’s private bank in 1995 and began to wed his love of art with a facility for numbers.

“Those two are pretty blended in me,” he says. “I’m pretty sure there’s not another institution out there that has a person who has those two skills combined. They either have the art, or the credit, but not both together.”

Ten years at Citi was followed by 16 at Bank of America. Then came the jump in January 2022 to Deutsche Bank International Private Bank. The titles on his business cards may have varied slightly, but his job does not. He tracks down business, travels when it’s possible, builds tailored loans for clients, and listens – a lot.

The last point is key, because you can learn everything you need to know about art from a collector. Direct a conversation to a client’s private gallery and the lights come on, he says.

“They will talk for a long time about their collection and how they put it together. They put a lot of human hours into determining how they’re going to buy works. They’re very passionate and emotional about their art assets.”

Art never stands still. Value is influenced by very human factors such as the desire to compete, win and own.

Prices are elastic and adjust to prevailing fashion. In October 2021, Sotheby’s auction house entered the metaverse, creating a forum for digital collectors to buy non-fungible avatars and limited-edition ‘generative’ art built by algorithms. Sales of NFT art and collectibles in August 2021 were $1.03 billion, according to Deloitte, against $3 million in the same month a year earlier.

Back in the real world, Arena and his colleagues and clients face a busy year ahead as leading art fairs look to get back to business as usual. Art Basel Hong Kong will likely be cancelled again in 2022, as cases of the Omicron variant mount in the isolated Chinese city.

But three Frieze fairs are slated to take place: in Los Angeles (February 17-20), New York (May) and London (October), interspersed by the latest iteration of The European Fine Art Fair, in the Dutch city of Maastricht in June.

Each will be buzzing, and Arena plans to attend them all.