Differential guidelines by Japanese regulators might provide room for accounting arbitrage. Japanese accounting rules have required banks and non-life-insurance companies to mark to market their portfolios since April 2002. However, the prefecture/locally run pension funds (such as those of Hokkaido and Saitama), and life-insurance companies (such as Nippon and Dai-ichi, or the Policeman Retirement Fund, and the Fisheries Association Fund) are not yet subject to the mark-to-market requirement. Market sources indicate that had it not been for such accounting arbitrage, it would have remained inexplicable why the local municipality pension fund of Hokkaido held a sizable amount of defaulted Argentine yen paper.

Related

From Vision to Ambition: Evolving ESG Strategies in GCC banking

Sponsored by Mashreq Bank

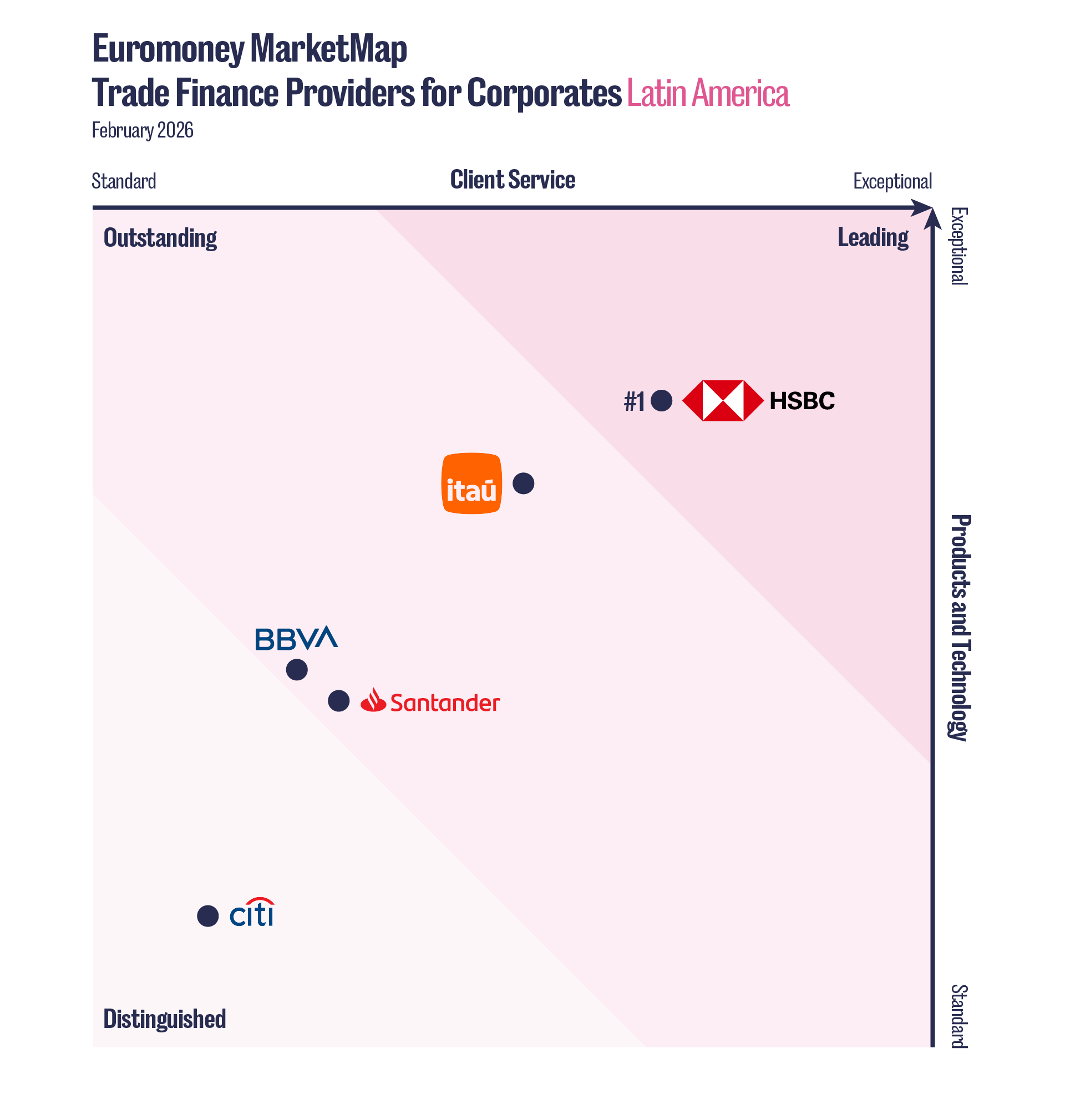

#1 trade finance provider for Latin American corporates in 2026: HSBC

Sponsored by HSBC