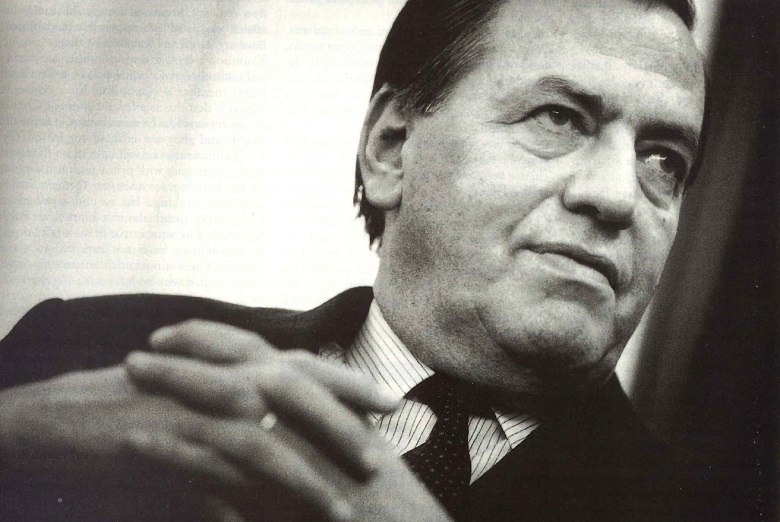

This head of the Deutsche Bank is strikingly popular. Colleagues and competitors not only respect him for his quiet strength but, without exception, they like him for his personal warmth and legendary fairness. Any ambitions he may have had, they say, never interfered with his sense of duty and obligation to others. This was most obvious when Herrhausen, his predecessor as speaker, was assassinated in November 1989: when his colleagues immediately voted Kopper to be speaker, he asked that the job be shared. In a matter of minutes, Kopper, the lifelong Deutsche Bank employee, succeeded to a post that many viewed as the second most powerful in Germany.

However it is measured, Deutsche is one of the world’s largest banks: it probably the single most powerful financial institution anywhere. In spite of having a small market share by the standards of other countries, it dominates German banking – its profits in the first 10 months of 1993 were greater than the combined total of the next five largest German banks. It is even Germany’s seventh largest life insurer, in direct competition with Allianz, which is forging closer links with Dresdner Bank, Deutsche’s nearest rival.

The legacy at Deutsche is awesome. The bank was created by Kaiser Wilhelm 1 in 1870. In 1918, it was stripped of its foreign branches. In 1947, the military government, determined to prevent Deutsche regaining its dominance, grouped its domestic branches into 10 separate institutions, none of which could bear its name. But it did not foresee the skills of Hermann Abs, who rebuilt Deutsche during the post-war economic miracle.

Deutsche is run in a way that is unique to Gennan private banking. The members of a German bank’s managing board, or Vorstand, inherit a tradition from 19th century banking partnerships: they are expected to behave as members of a partnership that owns the bank, even they do not. Because of that, and because of the German sense of hierarchy, a member of a Vorstand of one of Germany’s Grossbanken – or large private banks – is regarded as a person of immense importance and social status, much more so than a director of a bank in other countries. This partnership style produces rule by consensus with the speaker of the board having few formal powers, but with highly-developed skills of persuasion.

Since Kopper became speaker, Deutsche has become even stronger. When Germany unified, Deutsche built a market share in the neue Länder – the former East Germany – as big as its share of the west German market, by buying 70% of the branches of the former Staatsbank. Last month, it agreed to acquire another bank to add to its Italian network. Competitors in Spain speak of its growing presence with respect. The acquisition of Morgan Grenfell in 1990 has been a greater success than many expected, probably because Deutsche had the courage to appoint John Craven to be the first foreigner on the Deutsche board. The bank’s decision to compete directly with Allianz in insurance was reinforced with the acquisition of Deutscher Herold in 1992.

Its persistence in creating a strong presence in Asia has turned out to be an excellent decision. Internationally, the bank now ranks second to Goldman Sachs in international bond underwriting: the latest Euromoney poll ranked it first in trading international bonds. And at home, the bank’s costs have been attacked through a programme to cut staff numbers by 2,000 a year. But in spite of its success, Deutsche outside Germany remains weak in two important areas of international finance: equities and derivatives.

Critics remain, and in Germany they have been more vocal than ever. Germany’s recession has led to questioning of the elements that were believed to be fundamental to the economic miracle: the management and supervisory board systems; Mitbestimmung (co-determination by managers and elected workers’ representatives); and the powers of the Grossbanken. As speaker of Deutsche Bank, and chairman of the supervisory board (or Aufsichtsrat) of Daimler-Benz, Kopper has fought to shield both from hostile politicians and pressmen.

In the first full interview he has given since he became speaker, Hilmar Kopper spent seven hours with Padraic Fallon talking about the bank, its strategy, its board, its industrial holdings and about Kopper himself.

In 10 years’ time, Will there be two dominant financial groups in Germany?

Yes. It has already happened, and I expect it to more pronounced 10 years from now.

Do you have a vision for this bank?

No. A vision often turns into an illusion. I know what I want to happen, and how we will make it happen. And I know what I want to avoid, which is closely linked to change and volatility.

You have a strategy, not a vision. What’s your strategy?

Two-fold. To be the market leader at home, where we have seized a wonderful opportunity to grow our home base by 17 million people over the last three years. The second is to beccme a European bank.

What do you mean?

It means we want to be a retail bank in Italy and Spain, and to be a corporate bank across Europe, where we want to be strong in corporate finance, and in trading money, currencies, fixed-income, equities, and derivatives. We want to do asset management and distribute mutual funds in these countries: we are the largest in mutual funds in Europe. Our home currency is the Deutschmark, which should help.

What will you avoid?

Becoming a European retail bank, something that Crédit Lyonnais is closer to than we want to be. We are a European corporate bank, or a European trading bank, in the best traditions of a universal bank: active in guilders in Amsterdam, French francs in Paris, and sterling in London. This is what we are building, and we have built part of it.

Is that why you didn’t bid for Midland?

Yes. It is also why we didn’t buy anything in France. We were rumoured to be buying Lloyds Bank, Midland, Credito Italiano. The truth is that we never entered negotiations with any of these.

But you must have looked at them closely.

We looked at them, but we didn’t study them too closely. We don’t want to be the 10th largest bank in some European country where we never make any money.

Unless you acquire?

That would be very expensive. I don’t think you can make the returns.

Why don’t you want to be a retail bank?

Because I look around in the world today and I cannot identify a country where I wish to be a retail banker.

Would you have said that five years ago about Italy or Spain?

No. Five years ago we were already in high margin countries where no bank dominated retail: countries that we believed were behind in professionalism when it came to retailing. This is why we decided on these two countries. I cannot see any others.

In terms of your culture, are you retail or corporate?

If I am talking to a German, I stress retail, because he understands it better. Internationally, we prefer to be regarded as a corporate bank.

Like JP Morgan?

That is my favourite comparison. I mention its name with respect but I also include the Swiss banks.

Why?

Because they are viewed internationally as corporate banks, and as very good asset managers. It helps to be Swiss. I wish we could create the same international confidence in Germany and the Deutschmark, as the Swiss have done for the last 100 years. The cold war is over. Germany is a very safe and interesting place in the centre of Europe. It should be seen as such.

Is the size of the bank its greatest weakness?

I view it as a base from which to build. It is a very wide base, and it is so strong that we may be able to achieve things that other people may not wish to attempt.

Such as?

Making investments that others would shrink from. Morgan Grenfell was a significant decision, and not an easy one. We paid a full price, and we knew it. It was daring because it meant a culture clash. A big continental bank, like a very big battleship, acquires a flexible, aggressive, destroyer and makes a fleet of the two. I owe a special thanks to John Craven for that.

Why did you buy Morgan Grenfell?

Because it gave us access to something that we did not have, that we were unable to develop: a distinct merchant bank culture, a distinct London marketplace culture.

It’s not exactly large in primary, is it?

We make good use of it. A very fine example of that is the Scottish and Newcastle deal. Morgan Grenfell arranged the deal, Scottish and Newcastle bought the pubs from Grand Met, and Deutsche Bank brought the money. They did not have to talk to any other bank. There are not many banks around who can do that among themselves.

Whose idea was the acquisition?

George Magan came up with the idea. He and the Hambro family had opened a little shop. He came to me and said: “Now that Morgan Grenfell’s future is up in the air, shouldn’t you buy it?” I shook my head and I said: “Oh no, we will not succeed. I don’t want to leave the battlefield beaten”. But then he convinced me. I negotiated with rhe top people at Morgan Grenfell and particularly with John (Craven), who was on the other side of the table.

We already had a small shareholding in Morgan Grenfell, then, suddenly, the French attacked. This attack was possible because Willis Faber, the biggest Morgan Grenfell shareholder, wanted to sell. The French jumped at it, and the Morgan Grenfell people did not like that. So we made a phone call suggesting that we talked.

Was there opposition on the Vorstand to buying Morgan Grenfell?

Yes. It took a lot of convincing, and it was not done overnight. We had a number of meetings, at which I spent hours trying to convince some of my colleagues that we should pay what they considered a very full price.

Were you the main advocate?

Yes. I did all the negotiations in London. I stayed at the Hilton as Mr Smith.

Will you buy something as big, or bigger than that, soon?

There is nothing on our immediate agenda but if an opportunity fits our stratcgy, we will seize it.

Are you prepared to take risks?

Yes. We took a big risk when we bought Mr Flick’s shareholding in Daimler-Benz to stop it being sold to the Shah. We took another when we tried to do something similar for Fiat, when Gadaffi sold his shares. And took another when Mr Flick’s son wanted sell all his industrial holdings. I’m not talking about success or failure: I’m talking about this bank’s approach to risk.

Will Allianz and Dresdner become closer?

Yes, perhaps not in ownership terms, but I believe they will in terms of policy. I expect them to be much more coherent in their approach to markets. But I would like to add something. I feel that a bank owning an insurance company is a better fit than the other way around. I have very little to prove this, but I sense that regulators do not like non-banks owning banks, whereas the other way arond makes more sense.

Could the combination of Allianz and Dresdner become larger than Deutsche?

I do not know how to measure it because volumes in insurance companies are completely different to banking. I believe we will be larger in banking, while they will continue to be much larger in the insurance.

Is Dresdner’s cross-shareholding in BNP a threat?

No. I do not yet fully understand it. I watch it with great interest, because I have very serious doubts whether a co-operation between banks will make sense, because banking has to do with taking risks. Does co-operation work when you take on risks, but you don’t know what risks? Who is responsible in the end if something goes wrong; I was at the helm of one consortium bank with seven banking shareholders. I have seen consortium banks breaking apart. When it was all over, I had learnt a lesson.

Are you satisfied with your move into insurance?

We are far ahead of the crowd. People have paid no attention to our acquisitions insurance. We have set up an insurance company in Spain and we will do the same in Italy. The German move into insurance was very important for us, because it added new products, particularly life insurance which in Germany is the best after-tax asset management product. We decided we would create the product ourselves, and not use someone else’s. Generally, profits come slowly in insurance, but this has grown very fast: it’s been an amazing success. We decided to go further, and bought majority in Deutscher Herold. We also own 30% of Gerling. The result is that now our clients have an alternative.

To Allianz?

Yes.

How did Allianz view the competition from Deutsche Bank?

There was a misunderstanding to begin with. That’s now all in the past. Insurance companies have bought into banks.

But the initial reaction was fierce, wasn’t it?

It was an over-reaction. It was probably because we didn’t explain ourselves clearly. This is finished now.

What are your relations now with Allianz?

Very good. Henning Schulte-Noëlle [chief executive of Allianz] is on our supervisory board.

Doesn’t that put him in a difficult position?

No. I talked to the supervisory board the other day about our strategy in insurance. He saw this on the agenda and he very kindly offered to leave the room. I said: “No, why don’t you stay? We have no secrets, and perhaps you can give us some good advice.” As everyone knows, we are a 10% shareholder in Allianz.

Will you buy other insurance companies?

No, because the rules are different. In this country it adds something important to our domestic retail business: an outside salesforce. As a bank we have to sell out of our bricks and mortar. With 1,600 outlets, this is expensive. They are very often closed when a client has time to come and talk to us. Now our people can sell products outside banking hours.

You mentioned change, but even Deutsche’s fans say the bank is very bureaucratic. Some businesses have co-heads. Every letter needs two signatures. Can you change the bank fast enough to meet change in your markets?

We are not forerunners; we are slow movers. But when we decide to do something, we do it with a lot of energy. We may enter the revolving door last, but we may emerge first. We like to consider things carefully before we move. We may miss a few gimmicks here and there. We may miss some intentionally; a lot of them are short lived. We do not follow fashion. We may miss something because we have not been able to identify it as more than a fashion. But basically we have got it right. We move more slowly because we are bigger. But we are restructuring our organization to be more flexible in segments and to adapt faster to market requirements. I believe we have achieved that, at least on the domestic market.

But you haven’t achieved it in international equities or in derivatives, have you?

That is true. In derivatives we were slow to build volume, but we were slow on purpose. We may continue to be slow. not in the range of what we offer, but on how much business we do. On equities I couldn’t agree more. This is the area where we have a lot to do, and where we are just starting.

What’s your international equities strategy?

Organic growth outside Germany. We are the market leader in this country, but not in Europe, where London is the centre. But soon we will be the first German institution to acquire a seat on the Paris stock exchange. We are active in equities in Amsterdam. We would like to do more in Italy. We are active in Spain. In New York we have CJ Lawrence, and Morgan Grenfell (Asia) in Singapore and in other Asian emerging markets.

But Deutsche cannot mobilize large amounts of equity quickly for clients outside Germany. Is that an ambition?

Yes. We must be able to tell any big European company that we are able to raise large amounts for them, in any currency, in all markets, just as we can in Germany today.

How?

It would have to be grown, and I do not think it can be grown out of Frankfurt. Our base for European equities would be London.

And the US?

It would be very difficult to do the same there because of the power of the US firms. We will grow what we have organically: we have no ambitions to be Deutsche Sachs, or Deutsche Lynch, in the US.

You wouldn’t buy a special bracket firm?

The answer has always been “No”. We need our commercial banking business in the US: if we had moved into investment banking and brokerage, we would have had to give that up. Yet it’s an integral part of what we do.

But the restrictions are disappearing.

We have exchanged grandfathering for Section 20. Now we’re free to grow both sides of the business.

If the opportunity arose, would you buy a special bracket firm?

If we saw a genuine opportunity, we would look closely at it.

Could you manage a US investment bank – or the investment bankers?

This is the biggest drawback. The values are so different from ours that German talent would be out of place. We would go to bed every night feeling less confident than now. We would rather grow CJ Lawrence by adding to it.

Is Credit Suisse’s investment in First Boston a success or a failure?

When they first set it up, I was scared stiff.

Of what?

As a competitor. I said: “That’s it. Look at Zurich, London, New York, Tokyo. The world.

That frightened you?

Absolutely. I thought this is a non plus ultra. That they would be dominant within months. Fortunately for us, unfortunately for them, that didn’t happen. On the contrary.

Is that why you’ve never done the same?

It continues to make me cautious. We’ve always been extremely cautious – some say slow – in the US. I’ve seen so many other Europeans not able to manage their North American investments.

So buying Lehman, or anything else, is not on your agenda?

That’s right.

How will you build up in European equities?

By finding people and hiring them. This is very high on our agenda. We don’t want a Big Bang solution: we want to grow Deutsche Bank people talent.

Wouldn’t that be a very different culture?

Yes, but we can live very well with a completely different breed of people, including people who require a completely different type of remuneration. We already do. There are dozens of people in Deutsche Bank who earn more money than I do, but I’m happy as long as they make more money for the bank than I probably do. Perhaps we may end up, two or three years from now, by making a quantum leap, but we would certainly start by putting our intellectual infrastructure right first.

Are you implying that this is under intense discussion by the board?

Yes. It definitely is. It is a major point on our agenda.

Is the same true of derivatives?

No, because those discussions are finished. The important decisions are behind us. This is almost true on the equity side, but not to the same degree.

What visible results will flow from the decisions on derivatives?

You will see us more in the market.

Swiss Bank Corporation made its quantum leap by buying in Chicago. Have you considered something similar?

We looked at O’Connor because it was also offered to us. We were not ready for it then because we did not believe we had the, let me call it, managerial infrastructure here in Frankfurt to take O’Connor under our wing, and to understand and know every second what they were doing.

Are you ready now?

Yes.

And are similar acquisitions on your agenda?

Let us say that we are keeping our eyes and ears open.

[Article continues below box]

| Kopper on Kopper |

|

You grew up in the countryside in west Prussia, in what is now Poland. What was that like? It was absolutely a country life. Half of it was during the war, but the war was so far away – at least until early 1945 – that there is very little I can remember that had to do with war. There was the occasional visit of a wounded friend who stayed with our family for some weeks, and I remember the radio bulletins but I did not, like so many other people, see bomb raids or anything like that. I wasn’t conscious of war. What happened to you in 1945? We became refugees. My mother had four kids, and my father was a soldier. My mother had never cooked in her life. We had cooks and maids and many servants. I was taken to school every day during the war in a wonderful horse-drawn carriage, with someone in full uniform with a whip in front, and driven back four miles every day after school. We were absolutely unable to do things for ourselves. Did your family come from there? Yes, from the region south of Gdansk. They went there in 1592, when they were allotted land by the then Polish kings. How traumatic was it to become a refugee? It was a great adventure. I was 10 when we escaped. The tough times came immediately after that, from April 1945 when we were in a place south of Hamburg which then became the British zone. I remember American troops and British troops moving in, and there was still some fighting. We had to make a living. My mother and us four children worked on a farm. We were in all sorts of black market deals. We caught trout in the river, and bartered them with the British officer’s mess for cigarettes, which we then bartered for fresh eggs, which we then bartered for white bread. It was a horrible time. There were nights and days when we almost froze to death. But, looking back, it was the most interesting and formative period in my life. Because it made you tough? No, because it made me responsible. I had to care for myself and for others. It brought me values that I still cherish: getting things done; being reliable and loyal; standing by others; keeping your eyes and ears wide open; being able to approach people. It’s said you don’t have any enemies. Is that true? No, I have enemies. I make no secret of it when I don’t like people. I tell them so. I’ve learnt that the hard way. Alfred Herrhausen always told me if you don’t want to be caught, tell the truth and nothing but. You will not be always be liked, but you will be respected. Where has telling the truth made you enemies? Probably earlier in my career at the bank. Certainly in business life. I’ve never cared much about it. I’ve always treated my superiors with respect, but I have never bowed too much to them. I have got into a lot of trouble in my career when people wanted approval for something and I said “No”. I often say to people here: “Please remember that you’re being paid for saying ‘No’ or coming up with something better. You are not paid to say ‘Yes’.” I’m impatient and I hate stupidity. If someone is stupid and lazy I find it hard to keep my hands in the pockets. Do you ever lose your temper? Unfortunately, yes, I sometimes do: probably more in private than in business, although it happened much less in recent years. Maybe it has to do with age. Have you mellowed? Yes, but sometimes I sit here and swear. To yourself? Yes, and sometimes also to people from the bank who are with me at the time, If something is awful, I say how awful it is in words that would have to be deleted from the records. When you look back on your career, what were the most difficult moments? The periods of utter frustration early in my career when I was doing repetitive, dull jobs: doing the same thing for months, even years, and not seeing a result at the end. Not being able to talk to superiors because they didn’t care about you, and they wouldn’t listen. These were times when I felt completely neglected and underpaid. When I married, my wife in her first job made more money than I did after seven years at the bank, and I thought that wasn’t right. One looks back now and laughs at all this: how one struggled to raise one’s monthly salary by 20 marks. I think about this now much more because I suddenly realized that in April 1994 I will have been 40 years with the bank. That is almost one third of the time this bank has existed. How do you relax? I have a strange ability to pull down the shutters and not think of the bank when I enter my home, if I have no paperwork with me. I do the same when I am listening to music, talking to friends or family, I can even do the same on holidays. It’s an immense gift. I’ve never had in my life what I call the replay at home. What’s that? I only experience the bad things once, and that’s when they happen. I’ve never come home and spent the evening telling my wife what went wrong during the day. I never talk business at home. Do you read a lot? Yes. Recently, I’ve reverted to history books: the good ones. I’m highly selective, because I have someone who does all the pre-reading and selection of the very good books for me: my wife. She is a librarian: this is why she can read very fast. Sometimes I like to read modern literature, and then I will go through a spree where I will read four Updikes in a row. Who are your favourite characters in history? I single out Talleyrand as someone immensely interesting. Bur there are others, like Disraeli, and there is the never-ending fascination with Bismarck. Do you read books in English? Some, particularly if the translations lose the gist of the language. I’ve read a lot of modern German literature, and I praise myself, or rather my wife, for having been able over the last 20 years to obtain a good supply of East German literature. That was helpful when unification came. Even knowing about the loving tractor was useful in its way. What’s that? In socialist books there was a red tractor that loved a nice little Party girl out in the country. It was unbelievably bad. Are you a sportsman? Not as much as I was. I did a lot of running and I played a lot of soccer, and at school we played a lot of handball. I then played for many years until my middle thirties. I played a lot of table tennis which I loved because it was fast, and I love fast sports. Are most of your personal friends powerful people in Germany? No. My best friends are those I have had for 40 years. They have nothing to do with my profession. Some have made a very good career in business, but some are not in business. The older you grow, the fewer new friends you make, but here and there you make new friends and those, almost invariably, do not come from my profession. My closest friends come from the arts and from non-business areas. It’s fun to talk to people who have very different ideas. Do you talk business with your friends? No. I talk about politics and cultural life: about the theatre, music, literature, modern painting. It is a variety of topics that has nothing to do with my work. |

Michel David-Weill of Lazard Frères says there are no investment bankers in Germany or Japan. Do you agree?

It’s changing now, but broadly he is right. Perhaps the talent has been lost. Perhaps it has to do with German companies, who we find hard to convince that they should pay for advice: in this country, good advice from your bank is free. Very recently we have forced some of our people who give advice to send invoices. Some of our clients grumble at paying for advice, something that has involved us in a lot of work. But they would not hesitatate for a second to pay a higher fee to an Anglo-Saxon firm. The client’s reply to us is: “To compensate you for what you have done, which we appreciate, you may take a good chunk of the deal in your books.” Which means risk. And they not only offer it, they expect us to do it.

Is that changing?

Not in Germany. We must first remove the belief of many Deutsche Bank people that the ultimate success of a transaction is measured by what you take on your books.

Proprietary trading is a big piece of your earnings. Does that worry you?

No, not at all. We are very conservative. In some areas we are too conservative. We trade rather than take positions.

But you take positions.

If you are a trader, you have to, but the aim is to trade with as little positioning as possible, preferably intra-day or overnight. This is probably too much of a holy cow at Deutsche Bank, but it’s kept us out of trouble. We’ve also missed some opportunities. But we have done remarkably well with our proprietary trading: we are among the leaders in the world. If you add up the earnings from proprietary trading of the next five German banks, the combined total would be less than ours.

Deutsche Bank’s 1993 profits from outside Germany are said to be greater than your domestic profits. Is that true?

On a net basis 1’m happy to say it seems to be true for 1993. This is the proof that our earlier decisions to develop outside Germany were right.

Which areas?

Geographically, above all Europe. This was the core philosophy: Europe first. South-east Asia has also been a terrific success for us.

Has the growth been in corporate banking or capital markets?

Both. Proprietary trading, plus straightforward banking but with an ever increasing value-added in lending. It’s much more structured finance than simple lending. Structured finance is the future.

Are you optimistic about the earnings prospects for the bank through the 1990s?

Yes, but I am not euphoric. We will continue to cut costs. We must be a high-quality, low-cost producer. This is something we should do when we are doing well, and not wait until our backs are to the wall. There are moments when you ask yourself: are you cutting the right expenses? Are you not cutting those nice little businesses that may blossom three years from now? I do not think we are, but I watch that very carefully.

You’re cutting staff in Germany by 2,000 people a year. Do the plans you’ve announced to cut more still stand?

They stand. We know what we will be doing in 1994, when it will probably be another 1,500. This is a significant departure from the growth in staff we have seen over the last 30 years. This is the third year we have done it. By next year we will have reached 6,000. This is already a significant number. I haven’t seen many competitors, not only here but in other countries, doing the same.

They do it when they’re under pressure.

They not only have redundancies, but they close branches. We don’t do that.

Because you regard your branches as part of your equity?

They are. I couldn’t imagine this bank without its retail base in Germany. I would be afraid to enter into activities abroad without that solid base.

Tell yourself: ‘Deutsche Bank is not the bank that I own, but the bank that owns me’.

Aren’t you a one-currency bank in international capital markets?

We’re certainly a Deutschmark bank.

Will you change that?

Not as such. We do deals in plenty of other currencies, but I see no reason why we should artificially move away from a growing stable currency, particularly in the European context.

Aren’t you exposed to periods when the Deutschmark will be out of favour with issuers?

Yes. This is why we grew our London primary market operation. We have done very well in dollars over the last few years – including Australian and New Zealand dollars.

As we speak, Deutsche is second in the league table of international bond underwriters. But if you strip out Deutschmarks, you’re number 19. What will you do about that?

Focus much more on the other currencies. 1993 was an exceptional year: we have done so much Deutschmark business for sovereigns and supranational borrowers that they found it difficult to give US dollar business as well. The problem is that when you are a leader, you can’t have it all.

That makes it tougher for Rainer Stephan, doesn’t it?

But they are active with their Frankfurt colleagues on the Deutschmark side: they also make money from this.

Do London and Frankfurt still mistrust each other?

No. The co-operation between our people here, and in London, is far beyond the early stages, when they viewed each other with suspicion.

Are you pleased with the performance of the capital markets team in London?

Yes, wholeheartedly.

Do you have any reservations?

No, but we should grow more, and be better at distribution.

Is it true that international capital market business is not viewed seriously within the bank, except as a public relations exercise?

There is some truth in that. But this is because until a couple of months ago primary and secondary in Deutsche Bank were different responsibilities, right up to board level. We’ve changed that.

By putting them jointly under Schmitz and Breuer?

Yes. Primary is much closer to trading and sales than before. But there used to be a taboo in Deutsche Bank that the two could not be put together. Yet we make most of the money by selling the paper, not from the fees on the primary side. As a result, there was always a perception that we did not make a lot of money from capital markets. The prinary guys had some good years, they had very poor years, but consistently a lot of money was made. We pushed the two together and we now have a structure that I think is state of the art, and we left behind a cherished Deutsche Bank holy cow that was there as long as I can remember. There were big fights at the top over this: turf battles, someone saying: “These are my people, your people are not supposed to yell at mine.” We lost market opportunities by handling it that way. I respect my colleagues involved for seeing it, and agreeing without hesitation to change it.

Who do you credit for that?

The whole group, but particularly Ronaldo Schmitz and Rolf Breuer.

Did you knock their heads together?

Never. We sat down and discussed it. We produced a paper. The people under them became involved. They began to haggle with each other, and we said: “No, we decide this at board level.” And we did. When we decide something at Deutsche Bank, we come with one opinion that is shared by everyone. Some people call this a unanimous vote: I always say we never vote. We discuss. And if, at the end of the discussion, no one knows any better, we say: “That’s it.”

Some nasty journalist at the Bild Zeitung is far more powerful that I am

Does the board work purely by consensus?

Yes. Sometimes it is a consensus that has been achieved after a very hot debate. But it has worked for 120 years. It has served Deutsche Bank well.

The style is said to have originated from the old partnerships in Germany. Is that true?

Yes. Our forefathers saw themselves as partners in Deutsche Bank, even though they weren’t. It is something all of us value highly. It’s very often misinterpreted, misunderstood. People call us the 12 apostles, or the politburo. But it’s not a club. There is no feeling of what I call buddyism. Even among themselves, they are not on first name terms.

Vorstand members call each other Doctor Breuer, Doctor Schmitz and so on?

The doctor may be omitted.

So it’s Breuer and Schmitz – but it’s not Rolf and Ronaldo?

That is correct.

Even in a private room on a Tuesday morning?

At the regular Tuesday morning meeting no one calls each other by their first name.

Why not?

Tradition. We want to avoid the wrong impression that we are a very special group: that we are shoulder-slapping buddies, and that: “If you say ‘Yes’ to my problem, I will OK yours”, or “I’ll tell you how good you are, if next time you tell the rest how good I was”. We don’t do that. The rule is that you never praise each other.

Do you criticize each other?

Yes, we do, but in a detached way. You are not expected to yell at each other Having that barrier may mean we lack something as a group by not calling each other by our first names. But it stops us from doing certain things badly.

So Cartellieri would say: “I think we’re weak in mergers and acquisitions”, but he wouldn’t say: “Schmitz and Craven are not good at M&A”?

Right. He would not say: “You fouled up”. He may do so in private: I don’t know, and I don’t care. We need to criticize ourselves because it stops something going wrong. There is one thing that is so important for all 12 of us. When you look in the mirror in the morning, you have to tell yourself: “l have a very interesting job, but it’s only for a given number of years, and then it ends. Deutsche Bank is not the bank that I own, but it’s the bank that owns me.”

Because a board cannot live a normal life?

Yes. You are elevated. You are someone special to a lot of other people, not only in the bank but also outside. When it’s all oser, you are Hilmar Kopper again, and that’s it. Whatever you do, base your thinking on that simple fact.

Being on the board of a Grossbank is said to make you very special in Germany. Is that true?

Yes. It is easy to let that go to your head, to forget that it doesn’t make you a different person.

When you meet on Tuesday mornings, do you have a set agenda?

We have always the same agenda. There are 15 headings, and you put each item under them.

What are the headings?

The first one is always the famous one of dates: appointments, meetings and so on. Then there is personnel, loans, capital markets and so on.

How does the board make decisions?

By the previous Friday afternoon everyone has a paper on anything to be discussed. The paper will indicate whose paper it is, it will be signed and it will indicate at the top which board member will present it. Very often there is no discussion. We look at it, and then he starts: “Then there is my paper on…” and all of us look at him, and he says: “Oh, that’s it?” and we say: “Yes, that’s it – passed.” Sometimes a discussion develops, and that may end in the paper being rejected. In a group like this, when everybody says “Yes”, you only once say “No” for fun, because they will look at you, and you must explain. If you do not have very good arguments, it’s certainly the last time you say “No” just for fun. But one out of 12 may have damn good arguments and the other 11 may look at each say: “He is absolutely right.”

What role do you play at board meetings?

I chair the panel, as it were. We handle things in a peculiar, but traditional, order. The most recently appointed board member sits on my right. But when Ellen [Schneider-Lenné] was, we asked her to sit in my old place, which is exactly opposite me. I like to see her sitting where I sat. We go through the agenda and then suddenly something pops up that is not on it, there’s no paper, because someone has said something. Then I say: “We will not discuss this today, because it’s too important: we must prepare ourselves well to have a good discussion and find a solution.” Sometimes I come in with questions, and I say: “I have seen this paper, could someone please explain to me what it means?”

I am responsible for our contacts with the outside world, and in particular with the media. Because our agreement is that all my colleagues speak to the media on their field of responsibility – which I think is a must – I may say that I like what they said, or what they wrote. I may also say I did not like what they said or what they wrote, or that I felt that there was a bit of trespassing into the area of the general policy of the bank, and this was something that we should not have done. In general, it is better to dispose of all of this on a Tuesday with all of us there, instead of with each other in private.

When do the board meetings begin?

Usually at 10 o’clock, although there is an increasing tendency to start at nine. Very often we may have half an hour with people from the bank making a presentation, followed by a discussion, particularly if it is something new. If it’s an issue we need to go into in depth, it may take us two hours, because we get very involved, particularly when we’re learning from some of the younger people.

When do you finish?

Sometimes we are through by lunch. Last Tuesday we were there until 3 o’clock.

Meeting every Tuesday sounds a ponderous way of making decisions. Why don’t you meet once a month?

Because there are things we believe we should discuss together. Take the minutes, where there is another rule. The minutes are written by the youngest by seniority. That’s an excellent way for him to get involved and introduce himself to a variety of topics. The minutes are very short. Very often we talk about things where we do not make a decision, because a decision has not been asked for. Something may have happened in Germany that we may discuss for half an hour, about what it means for us. We may talk about strategy in different fields. Twice a year we meet for two full days and discuss a variety of very far-reaching topics – things that you never can do in half an hour, where you need preparation. This is where a lot of strategy is decided. Most of the time is used to inform each other.

As a communications forum?

Yes. After three or four months, John [Craven] said: “This is entirely new to me. This is so unlike any British board meeting: it’s like sitting around a table over lunch.” Sometimes the conversation is very light. Someone may even tell a little joke, and say: “You know who I met? He told me so and so.” This is a wonderful way to communicate: like partners where, in the good old days, they would have their offices next to each other, with open doors, and they would walk around.

Or even one big room.

Yes. I saw that in Brazil, at Bradesco. All the partners sat in a big room.

Do you wish you could do that?

Yes. And we sometimes do. I sometimes walk over to one colleague, and we sit down and we talk for half an hour, or I will phone and ask: “Could we meet at seven this evening?” We will not go for dinner, we will sit and talk often about personal things, the family, the good things and the bad things that you encounter. This is a tremendous glue. Even though we do not use first names, we care for each other. We are still civilized, and we respect each other. All board members must maintain that respect.

What does it take to become a board member?

Above all, it takes luck. Your name, your face must, at the right moment, be remembered by the people who decide.

How young can you be?

I was 42. We keep on telling ourselves that we should take younger people, but you also look for the mature person. So there is a trend, whether we like it or not, that people are normally over 50. But not necessarily. Jürgen Krumnow and Ellen Schneider-Lenné were both under 50.

Was she the first woman on the board?

Yes. And she is not a representative female. She is there because I would say she is our best man. We expect a strange mixture from our people. Obviously, proven loyalty and integrity. But then there has to be flexibility, and personality. He doesn’t have to be the best professional, but it is very important that he brings a necessary new ingredient to the group. We are strong when we are different. I would not like to have three rather similar characters on the board. I would rather have 12 different personalities.

Does it have to be 12?

No, there is no maximum. We were 13 for years. We will be 11 in 1994 when Zapp retires, but we may replace him.

As you meet once a week you can’t have a board member based in Tokyo or New York. Doesn’t that make you introspective?

We try to compensate for that by having people on the board who have lived overseas.

Like yourself?

Or even longer than I did. Ronaldo Schmitz spent years abroad. Ulrich Cartellieri spent years in New York when he was young. We like to have people from different backgrounds, though we have a pronounced preference for home-grown. Very few have come to us from outside, from industry. Now Ronaldo is the only one.

Herrhausen was another.

Yes, and you could say Wilfried Guth was one.

What powers do you have as speaker?

It’s not the same as being chief executive or executive chairman of an Anglo-Saxon corporation. It works by persuasion.

Do you use your powers of persuasion at board meetings, or individually with the other board members?

Both. I use it frequently at board meetings, and individually in many cases. It’s part of my role. At board meetings I have to give direction. Sometimes I have to put my foot on the brake. Someone may wish to dash away and I have to slow him down. This is a convoy in many ways. We have to allocate resources, and we have to get our timing right. It is my duty to see that this is observed.

You’re said to have removed some of the aura of mystery of the speaker’s job, compared with Herrhausen. Is that true?

Yes, I did it on purpose. It is absolutely necessary to guide the people in the bank, and to open the bank so the public understand it better. There is a tremendous mistrust and mystique surrounding banks – and in particular Deutsche Bank.

Is that why you changed the perception of the speaker’s job?

Yes. I felt we must become more transparent. We must be able to explain better what we do, and why we do it. To explain our role in the economy, our role in society. When you take away some of the mystique you may look more human, but that is exactly how we should look.

| Herrhausen’s legacy |

|

On the morning of November 30 1989, one month before his 60th birthday and a week after the announcement of Deutsche Bank’s takeover of Morgan Grenfell, Alfred Herrhausen was killed by remote-controlled bomb while being driven to a meeting in Bad-Homburg. Herrhausen had joined Deutsche as a member of the Vorstand in 1970, having spent his entire career at Vereinigte Elektrizitätswerke Westfalen in Dortmund. He became co-speaker 15 years later and, when F Wilhelm Christians retired in 1988, the first sole speaker at Deutsche Bank since Franz-Heinrich Ulrich. He was the first of the post-war generation to lead the bank, free of any timidity over its role in the war. Outspoken, eloquent, charismatic, intense, complex – he was a man who excited reaction, and one who relished his power. “The question is not whether we have power, but how we use it,” he said. Herrhausen was true to his word, not only in masterminding Deutsche’s expansion into Europe and its diversification into management consultancy, insurance and investment banking, but also in his outspoken support for German reunification and as a close adviser to Chancellor Kohl. His prominence made him a target for the Red Army Faction who are believed to have murdered him. Did Herrhausen behave more like a chief executive than you? No, I would not subscribe to that. When Alfred Herrhausen became joint speaker, he had already served more than 15 years on the board, when he behaved like everybody else. Of course, his personality was Alfred Herrhausen. He was able, and willing, to project things differently than others. This was his strength, and it made him different, but he was still one of 12 different people at any time. What do you mean? I’m talking about his culture, his ability and willingness to go about things, to express himself in a unique way. This was his personality. It evolved over 15 years. It was only when he became speaker that this came to the foreground. There was a great deal of injustice over the way Alfred Herrhausen was perceived. People were unfair about him? Yes, some overdid it to the extremes. They created a mystique that wasn’t there, and wasn’t intended by him. He was a down-to-earth human being. There was something constantly on his mind: he did not consider himself – and he believed that others did not consider him – to be a Deutsche Bank person, because he came from the outside, and he came in as a board member. And because of that he was perceived as a spokesman on Germany rather than the bank? Yes, because public matters were always of special interest to him, long before he became speaker. But when that happened people suddenly listened, because he was speaker of the Deutsche Bank. Was he an expansionist? Yes, I think he was. I think he had nightmares about the future development of the bank: he had great insecurity and fear about that, something that most of us did not share. What did he worry about? He was worried about our size and profitability, comparing us to other banks. We were unable to put him at ease. Sometimes he was almost depressed and I never understood why: there was no reason to be negative, we were moving. I think he felt that he should change a Iot of things at the same time, not realizing that this is an organization that you cannot change in a fortnight. You can stay on the bridge, and yell “Change!” and it will be at last eight months before the stern of the ship moves three degrees. This made him impatient, and he suffered. Would he have overexpanded the bank? No. But it would have been up to the full board under our constitution, to decide on this. I was a little afraid that there was more of a danger of over-exposing the bank. In what way? In political and public terms. This is a very difficult issue, because there are first of all 50,000 people in the bank who want to identify with you, and then, my God, you have to deliver. He used the word “global”. You are said to dislike that word. Is that true? Please forgive him. He was there when the words global and mega were in. He had to pick them up and talk about them, so he talked about the mega-bank, the global bank, and the global player. When he died it was already very obvious there was no mega-bank or global player. There probably never will be, or someone will try it, and fail. I was in an unrewarding position because we wanted to get away from being asked about our global role, to prepare people for what we thought the future would be. We have done that, and I am grateful to everyone who helped. It’s said that Herrhausen taught the bank not to be ashamed. Is that true? He left a tremendous legacy of putting Deutsche Bank back into proportion, the way he dealt with the big issue of power. We still benefit from that. No doubt about it. He had the courage to say: “Don’t be ashamed to be Deutsche Bank, don’t be ashamed of being Germans.” |

Did you ever believe you would become speaker?

No, not really. There might have been a chance at one time. While we had two speakers, Christians and Guth, I think it escaped a lot of people’s thinking that they would not both retire at the same time. When Christians retired there was the inevitable issue of whether we should we continue with two speakers or just one. There was a variety of views on that, but if, at any time of my life there was a normal chance, it would have been then rather than later.

Were you disappointed?

No. Not at all. I was so happy with what I did. I was not burdened with all that a speaker has to do which takes so much of your time. I felt that changed abruptly on November 30 1989.

Once you had recovered from the shock of Herrhausen’s murder, did you expect to be named?

It happened very fast. Herrhausen was assassinated at around 9am. I was in Düsseldorf when I was told the news and I jumped in the car. All the board members rushed to Frankfurt, by plane, by car, I don’t know what. We were all here shortly after noon. Two hours later we met, and the decision was taken. It took only half an hour. We did not make the announcement, out of respect. This was Deutsche Bank at its best. We are able to make decisions very quickly – much faster than others.

Were you surprised by the decision?

Yes. I advised against appointing me alone.

You felt there should be co-speakers?

Yes, and they said: “No way.”

Did you know who you wanted to be co-speaker with you?

Yes, I felt there was a very logical choice.

Was it Weiss?

I would not like to mention the name, but I think all my colleagues know.

You have a very strange system where a board member is responsible for one of the bank’s businesses for a specific area of Germany, and for an overseas area.

Except me: I don’t have an overseas area.

How can, say, Krumnow manage the tax affairs, and still be responsible for Lübeck, Hamburg, Africa and Scandinavia?

Krumnov’s central responsibilities are financial controls and accounting. The reason each board member is responsible for a domestic region is that this is a federal country. Clients in the regions like to meet someone from the board: and they are entitled to do so. The matrix means that he will have in his domestic region colleagues with prime responsibility for private banking, for asset management, or for corporate banking. He is not expected to know every detail about a branch in north Germany. The same is true of his international responsibilities: he is not expected to speak Swahili. There is not much business in Africa today: that is why he has such a big domestic area.

How closely can a board member be involved in a region?

The purpose is to keep all board members involved in our domestic business. They know what the markets and problems are in their region: this makes our discussions much more meaningful.

Don’t you ask too much of your board members?

It is an awesome problem, because it takes so much time. We have often asked ourselves whether we should cut this regional domestic responsibility. Invariably we have come back and said “No”, because a lot of our decisions on the domestic market are much better than the ones we see being made around us. It will continue.

Is that also true internationally?

I think so. We all travel a lot. I remember Ronaldo Schmitz telling me, after he had been on our board for a couple of months, “My God, I thought that on the Board of BASF we worked like devils. But that is nothing compared to what I do here”.

Doesn’t it make impossible demands on you all?

We frequently put in 14-hour shifts, and often work weekends, but this is a service industry. We must go and see our clients. We don’t expect them to come and see us.

Are the demands on the physical energy of the board members too great?

We sometimes think so. But when we ask what we can do about it, we come up with ideas that weed out some tasks and shed others to let other people do the jobs, but we always come back to square one: that is, if we want to maintain this level of involvement, there is no other way.

Don’t you feel you and your people are remarkably underpaid compared to US investment bankers?

I sometimes ask myself whether the others aren’t remarkably overpaid. We think we are fairly treated. During the last five years we had only one raise. We didn’t even care to ask because we thought it was not the time to molest our chairman. Eventually, I went to Christians and he said: “Oh yes, I apologize, I forgot about it.” Remuneration is not very important. Perhaps we are rewarded by the perception that we have been lifted into the clouds, and by the power that we are supposed to have. But we are not worried by what we see in other industries.

Is each board member sentencing himself to a much harder life when he joins the board?

Enormously. When I was told that I would be put on the board I said: “Wait a moment, I’d like to consider this.” I was looked at in complete disbelief. Then someone laughed, and said: “My God, you’re still joking.” I said: “l am not. I would like to talk it over with my wife. Because it will change our lives.”

Are you saying you didn’t want it?

Of course I wanted it. But I was aware that it would change my life and, to a certain degree, the life of my family. That is exactly what happened.

Does the Aufsichtsrat ever interfere with the Vorstand?

No, it cannot. By law, the Vorstand runs theb business. But one can argue that running the business also means giving it a certain direction. This is where an Aufsichtsrat may interfere. You are supposed to discuss the major directions with your Aufsichtsrat, but that happens less and less in this country because half of the Aufsichtsrat are employees or union members. The competence of a German Aufsichtsrat has suffered tremendously since co-determination.

Because the union members interfere?

No, because most of them do not know anything about banking. How can I expect an employee representative to give good advice to my credit committee? He may be willing but he doesn’t have the professional background.

Is co-determination a stupid system?

It has been taken too far. We have had it for 20 years, so it is too late to change it. There is a big argument in Germany about corporate governance, yet no one has considered what the powers of a supervisory board are. People say: “These idiots on the supervisory boards, why didn’t they notice? They should known better, they should have re-directed the executive board.” This is a total over-evaluation of what a supervisory board can do.

You’re chairman of the supervisory board of Daimler-Benz. Can you tell the Vorstand at Daimler-Benz how to run the business?

Not at all. I wouldn’t dare to. If, as chairman, you are not satisfied with the way the company is run, you can talk to the executive board. If that does not work, all you can do is fire them and install new board members. That is the power you have. Otherwise you have to rely on what they tell you.

Do Guth or Christians interfere with you?

No, not at all.

Seipp is said to intervene at Commerzbank.

I don’t know about that, but I believe we have a very special culture at Deutsche Bank. It has developed over the decades, and I believe it is followed impeccably by both boards. I sometimes ask myself: “Have I told Christians everything I should have told him?”. Sometimes I have not, and then he reminds me, telling me that he’s read a little remark in the press and asking what is it all about? And then I have to apologize. But when he has a question, he would come through me exclusively. He will not go down in to the bank and make enquiries of one of my colleagues. He believes that I am his contact.

How often do you talk to him?

Generally every week. Right now I haven’t talked to him for two weeks, and I must call him. I will try to get him tomorrow from the car because in less than a week we have a supervisory board meeting, and there are things I need to clear with him in advance.

By law, the Aufsichtsrat appoints each executive director. In reality, how does it work?

By tradition, the selection is left to the executive directors. Then we present it to the Aufsichtsrat and ask them to approve it. So far the Deutsche Bank Aufsichtsrat has always been kind enough to do so. I am absolutely convinced that the Vorstand is the correct body to make that choice because we must live with that guy, so we will see to it that we get the very best. It has to be unanimous, and this is an issue where my vote would deliberately not be special. I like that: I hate executive boards where the chief executive has too big a say on who is on the board.

Why?

Because it magnifies trends. Our system provides that we at Deutsche Bank move in a straight line, irrespective of who is speaker. The direction may deviate slightly, but not much. In an Anglo-Saxon corporation you see very strong chief executives. That is also true of France: perhaps even more so because of the powers of the PDG. But when you look back on the courses these banks have taken, you see they have zig-zagged. Under one chief executive, the bank goes to the left. The next comes in, and wants to differentiate himself from his predecessor, so the bank swerves to the right. In our bank, we try to connect two points by a straight line.

There is a perception outside Germany that the speaker of the Deutsche Bank is the second most powerful man in Germany. Is that true?

Of course not. Some nasty journalist at the Bild Zeitung is much more powerful than I am. So is any politician. We have influence and a certain amount of power, but it carries a terrible load of responsibility.

The German government ignored you when it introduced the coupon tax. Did that show your lack of power?

If you advise them not to impose a coupon tax, they do exactly the opposite. They wouldn’t even listen to advice on some of the technical details: how to introduce it, that you should not tax interest of corporations because they pay their taxes anyway, that there is no need to have this advance system. I’ve said this again and again. Now big German corporations have their time deposits outside Germany, in Deutschmarks. It is ridiculous. All it does is generate tax revenues for the Luxembourg and British governments. I told the government that this was absolutely destructive: to no avail. I wish that more people in business in Germany would speak up. We are too few.

How friendly are you with Kohl?

He is not a confidant of mine, and I do not regard myself as his confidant. We both have the ability to talk to each other in confidence, if necessary. We both believe in each other’s integrity. Though I do not agree with many of his actions, I’m a great admirer of Helmut Kohl. I am very pleased to put this on record. He is the greatest politician this country has seen for a long period.

How much influence do you have with him?

I believe he would listen to me if I needed to talk to him. But, as Herrhausen said so often, talking to the Chancellor doesn’t necessarily mean that he buys your idea.

Because, as with the coupon tax, the political imperative can be greater?

Yes, I think that’s right. He will listen to advice, but he must make his own decision. History will show whether he is right or wrong. In the case of the coupon tax I believe it will be shown very soon that it was totally wrong.

How do you view shareholdings in other companies?

I regard them as a very valuable part of our assets. I regard them as necessary. I am not in favour of reducing them. I am in favour of shifting them. I would like to make the basket of eggs more international. I may wish to have different eggs of different colours. I would like them to be smaller, but I would like to have more of them.

What do you mean?

I would like to internationalize our holdings. There are very good companies outside Germany. Some of our holdings are too big. I would like to split them up. I’d like to see a new mix geographically, and by size. I do not wish to reduce the overall size of our holdings, because this is an important part of what this bank does. I like these assets: they are a very good and steady contributor to earnings. The influence and power they are said to give us I find totally uninteresting. They are supposed to give us power to influence and stay as the house bank. That may be a terrific dis-service to the bank. Very often these companies are offered wonderful deals by competitors. I can only encourage them, being a shareholder, to accept.

You don’t regard them as captive clients?

There are certain public deals where we have to be seen together, because we are a major shareholder. Let me explain. In Daimler-Benz, we are the biggest single shareholder with 28%. As much as Daimler-Benz would like to see a board member of Deutsche Bank cruising along in the newest and biggest Mercedes Benz to show the world how closely we associate ourselves with this company, I say to Daimler-Benz: “When you go to the Big Board in New York, Deutsche Bank must be a co-lead manager in the introduction, but we appreciate that you also need an American institution. Or when you come to the Deutschmark market with a bond issue, or a rights issue, of course we must lead manage that.” Why? Because if we didn’t, the world would say they are cross with each other. That wouldn’t be good for Daimler-Benz’s business, as much as it is not good for ours.

But you may not be the right bank to execute a particular transaction.

If we are not then they should go somewhere else, and that has happened. This is why I referred to a rights issue, where we are the right bank to do it. There is no one better. Just as I think they make the best cars. This is why I drive them, and by doing so I tell the public I believe this is the best car. It works both ways. It’s an issue of identification: it’s not an issue of power, and not an issue of being a captive client. There is a duty of identification to the outside world.

Does the CFO of Daimler-Benz feel free to use whoever offers him the best deal?

Except for very visible deals like a rights issue, yes. If he wants to borrow, he will borrow where he wants. One of their four divisions is Debis, which is a direct competitor to Deutsche Bank, It was established with our vote. How could I prevent it? As the biggest shareholder, you have a greater responsibility to go along with what a company thinks is good for it, than you are with a 2% holding because then you can be different.

Because you have to be very responsible?

Sometimes I wonder who is the captive.

Do you sometimes feel you are?

I do. This is why we have said we will sell about 3% of our holding; because I would like to see it below 25%. I don’t want a controlling interest, and I don’t want to be seen with a controlling interest. I want to reduce my dependency as a shareholder.

Is there a level to which you would like fall?

No. I will not elaborate on this, because it will immediately be interpreted as having lost faith in Daimler-Benz and trying to get the hell out of it. I am not. I will not even sell that 3% if the price is not what I think it should be. I am absolutely in no hurry. I still believe it is an excellent investment, and that’s it.

So what is the strategy towards your shareholdings?

I see companies where I would like to be a 2% or 3% shareholder.

Are you a happy shareholder in Fiat?

We are now. We like this re-arrangement now, with the family having formed that special group of shareholders of which we are a part. We’ve made peace with it. We never blamed Fiat, we blame ourselves and we blame the market.

| The Steinkühler affair |

|

As chairman of the supervisory board of Daimler-Benz, Hilmar Kopper was an important figure in what became known as the Steinkühler affair, Germany’s most public financial scandal. Franz Steinkühler was the leader of IG Metall, Europe’s largest trade union with over 3.5 million members. Steinkühler held several important posts, including one on the board of Daimler-Benz. Between March 18 and April 1 1993 Steinkühler bought Dm1 million shares in Mercedes AG Holdings (MAH). He bought them in four tranches, the last just 24 hours before the announcement that MAH was to be dissolved and its shares swapped one-for-one with Daimler stock. That day MAH shares, which normally traded at a discount to Daimler shares as they did not carry voting rights, jumped by Dm85. On May 17, Stern magazine published details of Steinkühler’s share dealings. Steinkühler admitted the deals, but insisted that he had not traded on insider knowledge. Despite the estimated Dm100,000 that he had made on the trades, Steinkühler still enjoyed widespread support. He claimed that the first he had heard of the share swap was on April 2, when Kopper announced the move to board members. Steinkühler paid the profits – and profits he had made from the purchase of Dm6,000 Fokker shares prior to their takeover by Daimler a few months earlier – into an IG Metall workers fund. Whether he had traded on knowledge gleaned from his position on the Daimler board, Steinkühler had not broken the law. It remains legal to trade on insider knowledge in Germany. Only voluntary restrictions exist against it. Daimler had its own internal regulations which executives were asked to sign. Steinkühler and his fellow worker-directors had refused to do so “on principle”. Steinkühler eventually resigned as IG Metall leader on May 25, saying that he could no longer subject his family to the constant press speculation. Two days later at the Daimler AGM, Deutsche Bank used its 29% stake to force Steinkühler to resign from the board. In July the Frankfurt Stock Exchange insider commission pointedly failed to clear Steinkühler. It announced that it “had been unable to pursue one individual who had made self-incriminating remarks because that person had not signed the voluntary code under which insider dealing is regulated in Germany”. By declining to accept the code retrospectively, Steinkühler’s case could not be investigated. For Kopper and Deutsche Bank, who had been in the forefront of efforts to stamp out insider trading, the affair was viewed as an embarrassment. Did the Steinkühler affair upset you? No, not at all. I was relaxed about this. I still maintain – and I have said this in public and was laughed at – that Steinkühler didn’t know anything about the intended remerger between MAH and Daimler-Benz. Why I felt he violated the rules is that he made two trades after he received, as a member of the supervisory board, 10 days ahead of our supervisory board meeting, a very confidential report on the year 1992, including the dividend that would be proposed. But he was not aware of the proposed merger of MAH and Daimler-Benz? I think he was not. I accused him of trading at a time when, in his capacity as supervisory board member, he was in possession of documents and information that were not available to the market. He knew that the Daimler dividend would be unchanged. And he made two trades in MAH, a paper that is a parallel share to Daimler-Benz. So he was correctly accused, but for the wrong reasons? Right. I tried to correct that, but it was never picked up by the German press because the German press could not understand it. How do you know he did not know about the merger of MAH? Because no members [of the supervisory board] were informed. I know every person that knew about this: none of them would have talked to Steinkühler. I said this in public at the Daimler-Benz AGM. I said: “l do not accuse him, and I do not fall in line with those who do. He knew about the figures and upcoming decisions when the market didn’t know. That was all.” And that’s what he acted on? To tell you the truth I don’t know, knowing him, and how lazy and arrogant he is, whether he even read the papers he was sent. I think he is innocent, but he cannot say that because then he must admit he has never read the papers, which is what I think actually happened. When I said that in a letter to him, he sent me a furious letter saying: “How can you say this?” I explained again, and he resigned from the supervisory board in a letter to me with a PS that said: “Thank you very much for your fair treatment of the matter”. Was he being sarcastic? He meant it, and I give him the benefit of the doubt. |

Where will you build your small shareholdings?

There is a natural tendency to look first at Europe, then the rest of the world. I think we should do both, and we have done so. We have ideas. We have favourites. We haven’t yet moved. We’re not talking pocket money. This is why I say we would rather shift, than start from scratch. There may be a terrific opportunity in the French and Italian privatizations where they will have the noyaux durs of core shareholders, who will have anything between a 1% and 5% holding. A bank cannot afford to bury its money at a yield of 3%, but at Deutsche Bank it is part of our core policy not to think in terms of maximizing results in the short run, but to optimize them in the medium term. But there are some propositions that just do not make it.

Do you expect banking relationships to come with the shareholdings in these European companies?

Yes. As a primary core shareholder, to put it that way, I would expect to be a core bank. The investments would come first, but once l have made them I would visit the management and say: “Look here, I am (hopefully) a happy shareholder of yours, and we are also a bank. There are things that we think we could do for you, perhaps better than others. I do not expect to be able to do business with you at a better margin than the competition, but l want to be involved”.

Do you view this as a way to become a pan-European corporate bank?

Not necessarily, because it is not the reason we would invest. We have been talking, however, as if what I have tried to explain is easy to do. The problem is that once we sell something we have to pay taxes on our capital gain. This is why we are reluctant to sell something and share the tremendous capital gain 50-50 with the government. I do not believe our shareholders would like that.

Might the German tax authorities agree to roll over gains tax if you reinvest in European companies?

I wish they would, because it would be very good for the country. It would be absolutely gorgeous if it happened one day, but I do not see it. There is no discussion on that issue in this country: it is a taboo.

When you chair the supervisory board meetings of Daimler-Benz, do you question the company’s strategy?

Yes I do. Maybe not at the meeting itself, but perhaps before it. I want to be involved. It doesn’t mean necessarily that I disagree, but I will Involve myself. I want to understand it.

Do you do so as chairman of the supervisory or as the owner of 28% of the company?

As chairman of the supervisory board. I have committed to that position and I want to live up to that commitment. I have only two chairmanships, and I only have them because we are the single biggest shareholder. That creates a strong sense of duty.

You’re also on many other supervisory boards. Do you ever intervene in those?

Very rarely, and only when I am approached. Often as a supervisory board member, you’re approached in private. The chief executive may come to see you and say: “We have this terrible problem, do you have any advice?” I give them my very best advice. If a company is doing something that I regard as absolutely wrong or foolish, I would go to the supervisory board chairman in private and say what I think they are doing wrong; or I would tell the chief executive. I will say: “I don’t want to say this in public, not even at a meeting, but I think you should reconsider this.”

It is said that for German companies the shareholders come a long way down the list of priorities. Is that true?

It is changing. I hope it doesn’t change too much.

Why?

I sympathize with some of the German thinking. The term shareholder value has been very abused, particularly in the US. The distinction I make is that, in the Anglo-Saxon environment, management feel the need to provide shareholders with results and dividends to allow them to raise more equity at a good price. Here, this is not so highly developed, and we have an abuse of rights by shareholders.

In what way?

In Germany, any shareholder with one share can say awful things, talk on issues that are completely unrelated. Like our AGM, where our shareholders talk about the ozone hole, the tropical forests, some Third World countries that we don’t even know about, and a variety of issues that have absolutely nothing to do with the bank. There is nothing to stop them. Our system provides for giving shareholders a platform. I would like to see that change: less platform, more about business and dividends and market values. Today, it’s like Speakers’ Corner, a platform for all sorts of crazy ideas. Our last AGM lasted for 10 hours. At the last Daimler-Benz meeting I had to turn off the mike. A well-known German professor accused me of being Rambo because I had to introduce a five minute time limit on all speakers. The meeting lasted from 10 am until 11.45 pm. I had to stop it before midnight.

When you look at Germany’s recent economic performance, do you feel it has lost its way?

No. What we see here is something that has been happening in other European countries and in the United States. What has happened at Volkswagen or Daimler-Benz is not as bad as what has happened at General Motors. Look at Japan. The automotive industry around the world is going through a structural crisis. I am the chairman of the supervisory board of Daimler-Benz, but I did not say to them 18 months ago: “Would you please lay off 30,000 people? We now know that the measures taken early on were not enough. We did not know it then.

The German press attacked you for not intervening. Do you feel bitter about that?

To an extent. But the analysis is so superficial. What worries me more – and it is something I cannot explain – is there seems to be some sort of global rule of inescapability: all of the big companies seem to be hit, including IBM. I am not saying that German management is better or worse than other management: the guys here are pretty good, and I know a lot of them, I trust them and I think they are able to put in place corrective measures, with determination. This is what’s happening throughout the country.

Including at Volkswagen?

It has two fanatics at the helm. I suspect they are putting it right.

Has Germany now such a high and rigid cost base that many industries will have to move out?

Some should have moved earlier, maybe not to south-east Asia, but to eastern Europe. Eastern Europe could be for the rest of Europe what south-east Asia is for the Japanese.

Are you optimistic or pessimistic about German industry?

Very guardedly optimistic. The managerial know-how and the will are there. There is still a lot of fat to be squeezed out, and this is exactly what is happening right now.

Have you had problems inside the bank on insider trading?

No, not on insider trading. We had a problem two years ago in the bank, in the Frankfurt branch where some employees were confused, shall we say, between trading for their own accounts and the bank’s own account.

What did you do?

We took out the axe. I tell you, we were unforgiving. In some cases where we fired people, the courts told us to re-employ them, which we refused, so we paid them off, which is a shame.

Is it something you feel strongly about?

Very much.

What would you do if you caught somebody in the bank doing it now?

I would react even more strongly. We are the first German bank to have created an Anglo-Saxon compliance system, helped by Morgan Grenfell and our American experience. The bank must be clean. We want to be a major market participant, and we must have the trust of other market participants. We are clean people. If we catch one [insider], he is out.

[Article continues below box]

| The Pirelli/Conti saga |

|