World’s best bank

Illustration: Angus Cameron

|

|

| World’s best bank |

| View full results |

In the first three months of this year Bank of America enjoyed the most profitable quarter in its history, with net income of $6.9 billion, 30% ahead of the year before.

That performance was driven in particular by rising loans (up 8%) and deposit balances (up 6%) in its consumer bank, which already serves one in two US households and pulled in $3.6 billion of pre-tax profit on $9 billion of revenue for the quarter, 9% higher than the first quarter of 2017.

Those are eye-catching growth rates in an already prodigious business with 67 million customers.

|

IN ADDITION |

|

|

|

It is not so long ago that shareholders and analysts would grumble that while the management team had done a good job of repairing Bank of America after the crisis, it still wasn’t much of a growth story and that returns, although steady, weren’t much above the bank’s cost of equity of around 9%.

They are not grumbling now. The share price that had rattled along at between $16.50 and $17.50 from the end of 2013 to the end of 2016, started climbing last year, doubling in value from November 2016 to the end of the first quarter of 2018. Market capitalization rose from about $165 billion to over $330 billion in March this year before settling down to just over $307 billion in mid June, as big banks sold off on fears over Fed tightening and trade wars.

That propels it to now being the world’s third largest bank by market capitalization behind only JPMorgan and Industrial and Commercial Bank of China. Bank of America ranked seventh in the world by this measure as recently as 2016.

“We don’t declare an ambition to be the biggest bank in the world either by market capitalization, by assets or by any other measure,” Brian Moynihan, Bank of America’s chairman and chief executive, tells Euromoney. “Having that as your aim would be a good way to make mistakes. But if dealing with our customers – doing the right business with the right clients, taking appropriate risks – happens to take us to being the biggest bank in the world, then that’s fine by us.”

Moynihan is quietly spoken, not the kind to outshine Jamie Dimon on Institute of International Finance chief executive panels or to proclaim his advice to those that haven’t asked for it, like the federal government or the president of the United States.

His brain sometimes seems to be ticking over all the numbers of the different markets the bank operates in faster than his voice can keep pace with.

“One of the qualities I most admire in Brian is his humility, which isn’t always prevalent among CEOs,” says Jack Bovender, a former chairman and chief executive of Hospital Corporation of America, and now lead independent director on the board of Bank of America. “But Brian is also very smart and he’s very quick. I have had occasion to remind him that if he listens to the pace at which I speak [Bovender has a measured, southern drawl] that’s also the pace at which I comprehend and that he might want to bear that in mind.”

Bovender came on to the board in 2012, two years after Moynihan became chief executive.

“Brian may have been less well known at first, though not any longer, given how the company has performed,” says Bovender. “He has matured into a superb leader.”

And don’t mistake humility and disinclination to pronounce on public policy for lack of confidence.

“I respect all our competitors,” Moynihan tells Euromoney. “But they don’t scare me.”

Progress

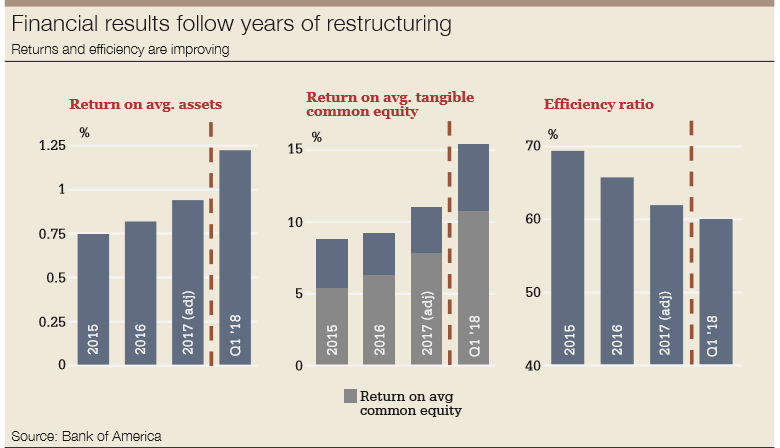

In the first quarter of 2018, with its three global divisions – global wealth and investment management, global banking and global markets – all performing well, the group as a whole achieved a return on average common equity of close to 11% and a return on assets of 1.2%, with an efficiency ratio of 60%.

It is unwise to judge any bank on one quarter, of course, but this seems to confirm progress that was already evident in strong full-year 2017 results, when the bank achieved $29 billion of pre-tax profit on $87 billion of revenue, with an efficiency ratio of 63% and a return on tangible equity of 9.4%.

“We didn’t clear the last major settlement with the Department of Justice until the third quarter of 2015,” Moynihan reminds Euromoney. “If any investors were waiting for that, then the company had already changed a lot by then. But it was only from 2016 onwards that they started to see normalized earnings.”

Paul Donofrio, chief financial officer, develops the thought.

“There was a time when investors couldn’t see the underlying growth because as well as settlements, we were still taking charges from writing off legacy assets,” he says. “Maybe they still needed to be convinced even when we talked about the transformation and the momentum inside the new core of the company. As you’re exiting businesses and products, it doesn’t really look like growth when revenues go from $120 billion to $80 billion. But then costs went from $100 billion to $55 billion.”

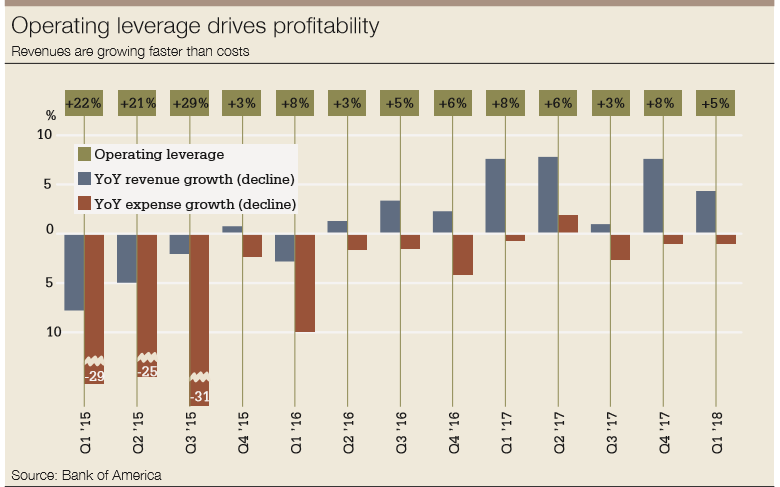

The most recent financial report confirms a now long-running trend: this is a bank that has consistently shown positive operating leverage. The first three months of this year marked the 13th consecutive quarter – now dating back to the start of 2015 – in which Bank of America has grown revenues faster than expenses.

Well-capitalized – perhaps over-capitalized – well-funded with $1.3 trillion of deposits and big liquidity buffers, increasingly efficient and with low charge offs reflecting a lean risk appetite, Bank of America is becoming a money-making machine for its owners.

Generating more earnings than it can profitably redeploy across its businesses without compromising its risk profile – which its leaders refuse even to contemplate – last year it returned $15.9 billion in capital to shareholders through a combination of dividends and share repurchases. That accounts for 90% of its profits. Regulators limit banks from returning more than their annual net income in capital to shareholders, so it is pretty close to the line.

Moynihan offers an extraordinary sounding statement: “We will never have to issue another share of stock in this company’s history.”

Surely this is an outrageous hostage to fortune?

The US and global economies have been growing since 2015 and that plus low interest rates have kept non-performing loans in tight check. That growth, as well as high valuations in financial markets, have been sustained by extraordinary central bank policy now slowly being withdrawn in the bank’s biggest market. Investors worry about the eventual impact on banks of a reduction in the Federal Reserve’s swollen balance sheet and credit losses rising off their lows.

There’s enough business for us to do with multinationals outside the United States. If you become too localized, you can become very exposed to a particular economy – Brian Moynihan

But for now rising rates actually help Bank of America. It has also become a deposit-gathering machine, and as US rates tick up from their lows they boost income and returns. US tax reform currently provides another bounty, while the bank’s own vast stores of data suggest that US consumers are spending and business owners are borrowing and investing at a healthy clip.

“Based on the customer activity we observe, we see consumer spending up 9% this year, coming after 6% growth last year and 3% the year before,” says Moynihan. “Companies are starting to draw on their lines once more and they won’t borrow money just because it’s cheap when they already have a lot of cash from earnings and tax reform. They’ll only borrow if they have something to do with that money. They are investing in their businesses once again.”

Everyone is bullish on America at Bank of America. What happens when the turn comes, as it inevitably must?

“We might possibly slow down the rate of share buybacks, but we won’t need to raise fresh capital,” Moynihan tells Euromoney. “We are generating billions of dollars of excess capital each year.”

Brian Moynihan, Bank of America’s chairman and chief executive

Some analysts suggest that the firm could operate against the economic and other risks it faces with maybe one-third less capital than it has – a surplus now tied up in various regulatory buffers. The bank certainly feels it has more than enough equity to safeguard against bad debts, market selloffs and operational risks. Increasingly regulators seem to agree. Senior executives believe that it now has the kind of fortress balance sheet that enabled JPMorgan to grow market share and bolster its brand so strongly after the last crisis and that now sets up Bank of America to outperform in the next.

Critics suggest that instead of waiting for this to happen, it should seek to press home its advantage now and increase market share around the globe while non-US banks, especially in Europe, lag behind. They suggest that if it made acquisitions outside the US now – maybe in Europe where banks are cheap, albeit for a reason, or perhaps a securities joint venture in China – it could cement a position of global leadership.

Moynihan, a lawyer by training, enjoyed working non-stop on M&A deals in the first part of his career. Back then, he lived with a map of every possible combination of banks and a full analysis of potential synergies. But he has learned some lessons since.

“There’s enough business for us to do with multinationals outside the United States. If you become too localized, you can become very exposed to a particular economy,” he says.

He gives an example. “It’s what I learned in Argentina in 2000 from BankBoston [Fleet had acquired BankBoston in 1999] when we got ourselves in between the government and its own citizens. They devalued what they owed us and maintained the value of what we owed them. Basically, in a single day the bank lost all the money it had made in Argentina in the preceding 75 years.

“So now when people come to me pitching investments and acquisitions and tell me things like: ‘You don’t understand. Country X is back’. I tell them: ‘No. I really do understand.’”

Wake-up call

Bank of America can still trip up now and then, like any lender. It lost $292 million last year on a margin loan to South African billionaire Christo Wiese secured by shares in Steinhoff, which collapsed in value after disclosure of accounting irregularities. The bank retained an outside legal firm to investigate what Moynihan described as an unhappy wake-up call. Many large banks made the same mistake. But it stood out more at Bank of America partly because the firm is now noted for its controlled risk appetite.

Bank of America, like all banks that were hit, has had to re-assess its approach to extending and structuring large margin loans with no recourse to other collateral than a single illiquid stock. Such single stock loans grant borrowers the option to walk away from their obligation if valuations fall precipitately, without a requirement to post other security. Bank of America evidently was not as good as it should have been at valuing that option.

Banks may have become used to analyzing such exposures in line with Fed stress tests, which may examine the impact on capital if broad equity markets fall 50% or 60% through a recession and market downturn lasting several quarters. In this case, the value of the collateral fell by over 90% in a matter of days.

The issue went all the way to the top.

“We have a phrase in the south, maybe you have something similar in the UK, where a person gets taken to the woodshed,” Bovender tells Euromoney. “It means they get asked some fairly direct and tough questions. Management identified this matter for review to understand fully what happened and brought it to the board to discuss it in great detail.

“Of course, we expressed disappointment at how it happened. No one in management made any attempt to hide anything. We went through a deep dive and I believe we have come out with a better understanding of all the issues and, as a result, improved processes.”

It was an unwelcome loss that hurt morale in parts of the bank. And in the first quarter of this year, total corporate investment banking fees were 15% lower than the stellar first quarter of 2017. But this is hardly a sign of an institution running out of control.

|

|

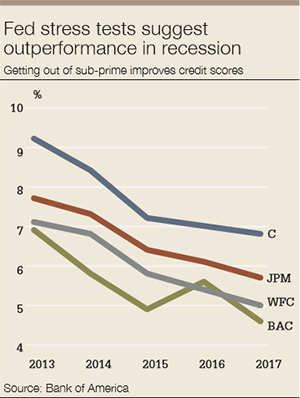

Last year’s Federal Reserve stress tests found that in a severe economic downturn, Bank of America would suffer lower losses than any of its peers.

This June the Fed released results of its latest test of how large US banks’ end of 2017 balance sheets would fare under severely adverse conditions, with a two-year decline in GDP of 8.9%; unemployment at 10%; the home price index down 30% and equity declines of 65%. Once again, it judged that the percentage loss rate of total loans would be lower at Bank of America (5%) than any of its US peers, including JPMorgan (6.4%), Wells Fargo (5.5%), Citigroup (7%) and Goldman Sachs (9.7%).

And it is not just in lending that the bank’s prudent culture is evident.

Its global markets business as a whole did not suffer a single loss-making day on any trading day in 2017, although individual business lines will of course have taken hits.

“You cannot underestimate the value of the franchise,” says Thomas Montag, the former Goldman Sachs partner who, as well as being chief operating office at Bank of America, now heads all of the businesses that serve companies and institutional investors, including middle-market commercial and large corporate clients as well as the global markets sales and trading businesses.

“A lot of the trading we do – in treasury bonds, municipal bonds, FX, for example – is inherently low risk, and we have real pockets of strength such as trading muni bonds, which has great links both to capital markets and to Merrill Lynch as a product for wealth management clients,” he says. “And yes, like every bank, there will be areas where we take hits on any given day, for example when Italian government bonds dislocated, but not of a size that the trading businesses as a whole lose money.”

Investors waiting for Bank of America to juice up trading revenues in response to a lightening of the regulatory load on US banks should not hold their breath. The diversification of the global markets business and its tight risk control has made it profitable on 98% of trading days in the last five years. The global markets balance sheet goes up: value at risk remains stable.

It has required a tremendous investment in technology to connect everything behind the scenes to support our customer-first view of the world – Dean Athanasia

Outside the bank, rivals look at this and wonder. The question now is not if Bank of America can succeed but whether it could aim for something close to domination, or at least attempt to surpass JPMorgan. Its markets businesses had total average balance sheet assets of $678 billion in the first quarter and earned a return on average allocated capital of 17%. For the full year 2017, it brought in net income of $3.3 billion for a 9% return on allocated capital.

“It has a really good investment bank and it’s really good at wealth management and, of course, it has a huge domestic bank that’s very strong in the middle market,” says the head of a rival institution. “But although Bank of America has done well, it is possible that this period, when the other US banks are really pressing home the advantage as the Europeans retreat, will eventually be judged a missed opportunity. And I do wonder what it might achieve if it took that markets balance sheet up maybe towards $1 trillion.”

But it simply won’t, partly because the bank does not want the wholesale side of the business, where investors judge earnings to be inherently more volatile and thus lower quality, to outweigh consumer.

|

| Paul Donofrio |

“If you look back to the business mix going into the crisis, we actually had too much exposure to consumer back then,” says Donofrio. “Right now, the balance between consumer and wholesale is much closer to 50/50 and we like that. We couldn’t deliver the products and services our wealth management clients and mid-market companies want without a global markets business that we have built to scale. I wouldn’t trade the set of businesses Bank of America has today with that of any other bank.”

Valuation considerations matter more to the bank’s senior executives than a short-term boost to revenue or even profit. “Today investors understand that our earnings are sustainable and likely to grow,” says Donofrio.

The question now becomes: can they trade on a higher multiple on the expectation not just that earnings volatility at Bank of America will be low through the cycle – certainly much lower than through the last cycle – but also that it will be lower than competitors’?

Bank of America ran a total balance sheet of close to $2.3 trillion in 2017. The global markets balance sheet was $639 billion. Global banking, which includes investment banking and underwriting, as well as global transaction services and large corporate lending, ran with total assets of $416 billion. Combined, global banking and markets account for just over $1 trillion of assets, or 45% of the group balance sheet, and the bank wants to keep it at no more than 50% of the company.

The bank’s leaders call this part of responsible growth, which is now the single key article of faith inside the institution and a mantra its senior executive repeat with sometimes off-putting regularity. It can sound a bit dull, although, even as memories of the financial crisis start to fade, being dull should surely still count as a virtue in banking these days.

We’ve built Erica for the here and now. She’s not yet ready to talk to real people at third-party companies on my behalf. But we’ll see what comes in the next five years – Michelle Moore

“An enterprise as large as this, one that clients depend on, has to be able to lend through the cycle. It cannot lend heavily and earn heavily only in the good times and then disappear,” says Moynihan.

“What that in turn means for us is that not every dollar of revenue is a good dollar. Yes, we absolutely have to grow, with no excuses, but not by chasing a dollar of revenue from the wrong client nor by doing the wrong piece of business for the right client.”

It can come across as a little pious, but there is cold business logic behind this.

“Markets are only now finally recognizing that this company has fundamentally changed,” says Donofrio. “In fact, it changed years ago when Brian Moynihan re-wrote the risk underwriting standards, though it wasn’t obvious when we were still running off legacy assets. We simply won’t make loans to people if we suspect they might not be able to service them in the next recession.

“Perhaps the most important thing Brian did was to give us all a purpose, which everyone at Bank of America can explain: and that is to help customers better live their financial lives,” he continues. “The purpose is not to make money off customers.”

Maybe he glimpses Euromoney’s eyes rolling.

“The point is that if we fulfil that purpose, we will make money and we will make it through the cycle. We just needed the financial results to show that, and those results are now coming through.”

New markets

The bank is also doing a lot to grow. It is moving into new markets, like Denver and Minneapolis. And it aims to do more with existing customers.

“Only one in three people we have a relationship with uses one of our credit cards,” says Donofrio. “Two out of three get a mortgage with somebody else. There’s a lot more that we can do with the customers we already have. We don’t need to create new products and try and sell to anybody that will buy them from us, irrespective of whether they need them.”

Moynihan took over as chief executive in 2010 following the ouster of Ken Lewis. Lewis had led Bank of America since 2001, succeeding Hugh McColl, the former marine who built Charlotte-based NationsBank into a truly national institution through a long series of acquisitions culminating in Bank of America itself. McColl chose that brand name for the national bank he had built. Lewis picked up the baton from him and shared his enthusiasm for growth through acquisition.

His time at the top of it ended with the misjudged acquisitions of Countrywide and, in the teeth of the hurricane, Merrill Lynch, which together brought vast exposures to the sub-prime crisis. Even were it not for Countrywide and Merrill Lynch, Bank of America would still have been affected by the financial crisis, but it had managed to buy its way into the very heart of it.

“The Merrill Lynch culture was quite out of control and the consumer businesses weren’t much better,” recalls a veteran who has left the bank. Moynihan, who had run Fleet Boston, one of the many lenders NationsBank acquired during its decades long roll up of medium-sized regional banks, had to spend his first years at the top cleaning all this up.

“The fines and the work associated with overhauling the bank, including getting out of 65 businesses after 2010, which we had to do simply in order to survive, cost much more than any losses on the sub-prime assets,” recalls Moynihan. “We went through hell. And we don’t intend to go back. We divested sub-prime mortgages, sub-prime auto loans, sub-prime home equity loans and the rest as fast as possible. Other banks might take a different view. And that is their right, of course.”

Never forget that the societal licence you have as a bank is a special one. People trust us with something that is absolutely central to life – their money – that they might not trust a technology company with – Brian Moynihan

It is not the tone of a man inviting a debate.

“All the strategy work at this bank has been done and though it may be reviewed, it won’t really be revisited,” says Donofrio.

“The strategy was worked out between management and the board and there was no dissonance,” confirms Bovender. “It is a risk-balancing strategy and it is also a long-term strategy based on building relationships of trust with clients as they move through their financial lives and being very transparent with them rather than selling them products that may be inappropriate or injurious.”

If they take less risk, banks have to be highly efficient to generate acceptable returns because margins on credit to good-quality corporate and consumer borrowers are thin, especially in a still-low nominal interest-rate world. Moynihan is treading a path that other skilled chief executives have also chosen, including António Horta Osório at Lloyds and Jean-Laurent Bonnafé at BNP Paribas. But he is leading a much bigger institution, one that in the years after the crisis regularly faced calls for break up from regulators fearful of the systemic vulnerability from banks too big to fail and from shareholders who initially thought its complexity might make it too big to succeed.

The response has been to reduce and standardize the product offering to a still-large range of customers including individuals, small and big companies and investors in the US and mainly large companies and institutional investors in the rest of the world. It now does basic banking. But it does it well.

|

| Dean Athanasia |

“If you go back just five years, Bank of America offered around 1,400 products and had many different types of mortgages, home equity loans, consumer loans, checking accounts, investment accounts,” says Dean Athanasia, who sits on the bank’s executive committee as co-head of consumer. “Today, it’s about 65 core products, with which we serve 67 million customers.”

It has been a profound change that enables the bank to manage much more efficiently. It has cut not just lower-level staff as it simplified the product offering and automated the associated processing but also layers of middle managers overseeing them, typically by not replacing managers that left over the last three years.

“We’ve gone from more than 25 credit card offerings to five, and from more than 20 types of checking account to just three,” says Donofrio. “And that in turn has helped us go from eight different teller systems to one unified system; from 15 fraud and claims platforms to just one, while improving fraud detection; and from 64 worldwide data centres to just 14. The way to generate an acceptable return is to keep things simple. You can’t do that if you’re still running 34 different operating systems. Fixing that, modernizing what we sometimes call the bones of the company, is where we were investing most heavily until quite recently.

“In future,” he says, “we will be able to invest more in relationship management and the customers’ user experience.”

And Moynihan relates this back to his earlier argument that acquisitions – already off the table for the bank in its home market for regulatory reasons due to its close to 14% market share – are also a non-starter overseas.

“When I look back to the previous period when this bank performed best, it was probably from 1999 to 2003 or 2004 when it wasn’t doing acquisitions,” he says. “We cannot do them anyway now in the US. But if you think of our three-year planning cycle, we simply couldn’t have made the long-term investments we have in our technology – taking data centres from 64 to 14 and all the rest – if there was also the prospect of doing IT integrations of acquired banks, for example.”

Far from being too big to succeed, the bank now has a scale advantage that few competitors aside from JPMorgan and Wells Fargo can hope to keep up with. It is almost a Warren Buffet-like moat.

“And yes,” Donofrio says, “we do feel a responsibility to serve the broad population of the US, so we will provide simplified checking accounts to less financially secure customers, but ones that don’t allow them to go overdrawn. Because guess what? When you overdraft people, you need armies of staff in call centres just to deal with their complaints.”

Staff mission

Today Bank of America looks like a supremely well run large bank, settled on its strategy – which some still criticize as unambitious, but which its management considers appropriate to a controlled risk appetite and carefully defined customer profile. For a number of years now it has been doing two important things: improving its operational efficiency and investing heavily in new technology to bind its customers to it more closely.

Large banks rarely do such a good job for shareholders – now that leverage is much lower and proprietary trading cut – unless they are also doing a good one for their customers. In the consumer business, Bank of America has sought to be the primary relationship bank, the one through which customers with higher FICO scores receive salaries and make regular important payments. That is the mission for its branch staff, who have not for years now been paid anything as vulgar as commission on products sold.

The bank sets great store by its preferred rewards programme, which offers incentives to retail customers based on how much business they do with the bank and the level of balances they maintain.

“Preferred rewards starts with customers establishing their main checking account with us that they use to receive their salary and pay their bills” says Athanasia. “Then if the customer holds a minimum level of combined balances with us across all accounts, they become eligible for enhanced rewards, including zero account fees, higher savings rates, discounts on home and auto loans, $0 trades through Merrill Edge and the free use of any bank ATMs”.

The more assets a customer holds with the bank, the higher the level of awards they receive back in a tiered scheme, starting with gold for those maintaining $20,000, platinum for $50,000 and platinum honours for $100,000. And if the customer keeps accumulating net worth, to say over a $500,000, they will likely be referred to a Merrill Lynch financial adviser, one of the famous ‘thundering herd’.

“It’s a tremendous programme, and when new customers see it, lots of them set out to bring their assets to Bank of America and work their way up through it,” says Athanasia.

Perhaps surprisingly, other banks have not yet seemed ready to compete with their own equivalent programmes. That in turn comes back to the simple and efficient model.

“It has required a tremendous investment in technology to connect everything behind the scenes to support our customer-first view of the world,” says Athanasia. “We really are no longer organized in silos, with the credit card division or the mortgage division making independent decisions about the customer without considering the full relationship. We are no longer run by individual product divisions as we were in the past. We are now run as one customer division that makes the best decision based on a holistic view of each individual customer.”

If it sounds a little too nice to be true, rest assured: it is all perfectly self-interested.

Those kinds of affluent customers now tied into the bank are also the source of vast quantities of sticky and low-cost deposits. Indeed, the ability to grow deposits across the franchise without overpaying for them looks quite extraordinary. Bank of America argues that its rewards programmes and increasingly highly-rated digital offerings are compensation enough for these deposits. Interest paid on them won’t climb much even if the Fed does keep raising rates.

We don’t look at revenue regionally. Is cash management for the US subsidiary of a French multinational, French or US revenue? I tell our people that I just don’t care. And what’s more, they should be glad that I don’t – Brian Moynihan

Those deposits are likely to stay with Bank of America because customer satisfaction is going up. The attrition rate on customers enrolled in preferred rewards is just 0.5%.

“Our latest data is that 81% of customers now rate us 9 or 10 on a 10-point scale,” says Athanasia. “Several years ago, only 70% were in that range, so customer satisfaction is at an all-time high and will go even higher. And this is all the result of rolling out preferred rewards, investing in mobile solutions, redesigning our service centres and branches, and integrating the different parts of the bank so that we know our customers better and can take care of them for any of their financial needs across checking, saving, investing, borrowing and transacting. We will always be there for them.”

In addition, the information content in these accounts assists risk management. So, when the oil price decline hit energy companies in Texas hard, Bank of America was able to keep a close eye on its exposures partly by monitoring aggregate changed behaviours across the accounts of consumers not even employed in that industry.

“We had some criticism over responsible growth at first from investors who suggested we were only talking about it because our competitors were growing faster than us,” Moynihan recalls. “But then we saw rapid growth in commercial real estate in Texas, for example, and some providers had to pull back. By contrast because we hadn’t grown too fast during the good times, we didn’t have to stop lending through the downturn in the oil price in early 2017. Rather we kept putting on new loans at pretty much the same rate.”

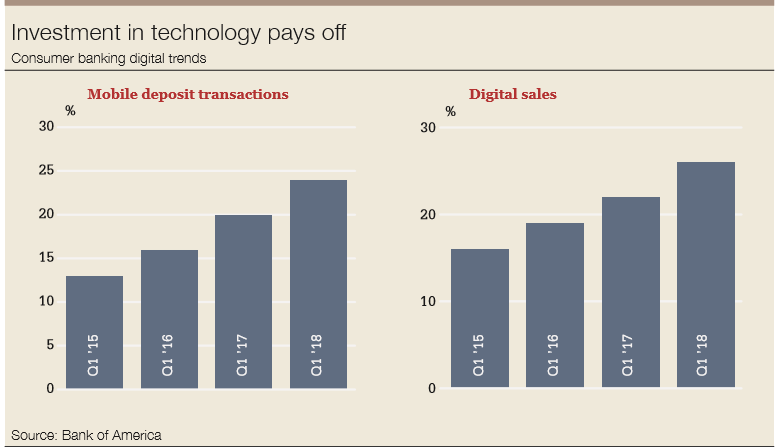

The bank has invested heavily in the technology to support all this as the industry goes through its digital transformation. The bank spends $3 billion a year, from a total annual technology budget of $10 billion, on growth initiatives in digital and mobile. The bank reached 25 million mobile users in the first quarter of this year, up from 19.6 million two years ago. Erica, the new chatbot launched on March 15, initially to customers in Rhode Island, already has one million users.

|

|

|

Michelle Moore |

“Customers can ask Erica for their balances and to make payments, but Erica can also help with things like budgeting or learning about credit,” says Michelle Moore, head of digital banking. “Erica can tell customers how much they’ve been spending at Amazon, at the grocery store or dining out.

“By the end of the summer, Erica will use predictive insights to help customers. Erica could tell a customer about the upcoming annual payment for a gym membership or magazine subscription to give customers the chance to proactively take action. Erica could also let you know where you use your credit card so you proactively update the number in the event you lose or replace a card. ”

Can Erica find me a better deal on utility bills?

“We’ve built Erica for the here and now,” says Moore. “She’s not yet ready to talk to real people at third-party companies on my behalf. But we’ll see what comes in the next five years.”

Bank of America was also quick to integrate Zelle, the person-to-person payment by mobile and email channel, into its mobile app in 2017. In the first quarter of last year, Zelle handled $4 billion of direct payments between individuals. By the first quarter of 2018 that had risen to $9 billion.

Moynihan lays out the latest milestones for Euromoney: “In April 2018 for the first time, the number of people taking a picture of a cheque and depositing it using their mobile phone exceeded the number of people coming into a branch and handing the cheque to a teller.”

Half of all cheques are now deposited at ATMs, with roughly 25% handed to tellers and 25% paid in by mobile phone. Moynihan says: “It’s not so long ago that tellers had to deal with 75% of cheques.”

It is almost surprising that 25% still go to tellers. But banks have to be cautious of not taking new technology too fast beyond the point their own customers are ready to follow.

“I do sometimes ask myself why take up isn’t even faster,” says Moynihan. “We can nudge customers onto mobile and digital channels, but we don’t want to force them.”

The bank calls its approach to consumer banking a combination of high tech and high touch. The bank reckons around 26% of its sales, including new card and account openings, mortgages and auto loans, are now transacted through digital channels against an average across US retail banks closer to 12%. The trend gives Moynihan confidence that efficiency gains will continue.

“For all this talk of a cashless society, we still see $250 million a day go out of our ATMs and a similar amount from our branches via tellers and we still take 400,000 calls a week,” he says. “But these are often now to make appointments to come into the branches. And if we know what people are calling about and when they intend to come in, then we can staff accordingly. And that makes us much more efficient.

“We are moving to a world where people come into branches only for the difficult things. So, for example if a customer whose parent is sick wants to talk about getting power of attorney, we can run through what they’ll need to do. With more straightforward, fewer credit card and checking account offerings, the technology can easily handle the regular transaction flow. Our staff can spend much more time on relationship management.”

Quartz tech

All this technology investment is not just for consumers. In the global markets division Bank of America has been investing in the equities business improving capabilities in electronic and algorithmic trade execution, raising the balance sheet but not pushing value at risk because the associated exposures are mostly very short term.

It is about to go live with the single firm-wide pricing and risk management system, Quartz, which encompasses front-, middle- and back-office functions across the global markets businesses. Years in development, this will allow for a clear end-of-day view on trading P&L and aggregate risk exposures derived from multiple asset classes on a single platform.

|

| Thomas Montag |

“Quartz has taken a lot of work by a lot of people,” says Montag. “It is a huge advance on the period after 2008 when we first joined the trading businesses of Merrill Lynch and Bank of America and had to cobble together the best of different systems for many separate business lines, just to get through the crisis.”

Will customers feel a difference when Quartz goes live? “Not directly,” says Montag. “But our finance department certainly will and our risk department. And customers will be dealing with a bank even more confident that it is on top of all the risk and position data in real time.”

A lot of the chief executives that Euromoney speaks to now like to say they are really running a technology company not a bank. Moynihan isn’t buying that, however.

“Never forget that the societal licence you have as a bank is a special one,” he says. “People trust us with something that is absolutely central to life – their money – that they might not trust a technology company with. We have to be on top of all the technology of course, but we are in a very particular personal service business.”

Moore, head of digital, agrees.

“We’ve been following the data for years as mobile has become increasingly central to our customers’ lives,” she says. “We have 10 million customers whose only channel to us is mobile. That’s equivalent to one of the 10 biggest banks in the country on its own. And almost everything you want to do with a bank – open a checking account, get a mortgage, buy a car, make investments – you can now do in our app quickly and efficiently. When you used to apply for a mortgage, you would have to fill in forms with maybe 300 information fields. As a Bank of America customer, we prefill most of the information for you, leaving you with probably 10 required fields to complete and perhaps take maybe 15 minutes or so to complete.”

Moore sees mobile and branches working together: “There will always be financial matters that customers want to talk to a person about, and no amount of digital capability will ever replace that.”

US initiatives

Talking to Moynihan at Bank of America’s office in Paris about how he wants the bank to grow that service business, Euromoney hears a lot about new initiatives in the US.

Almost by oversight, the roll up of regional banks in the 20 years before the crisis that built Bank of America somehow left it underrepresented in nine of the 30 biggest cities in the country. It has addressed this recently by opening financial centres and branches in Cincinnati, Cleveland, Columbus, Denver, Indianapolis, Lexington, Minneapolis, Pittsburgh and Salt Lake City.

“Denver is already at $2 billion of deposits and Minneapolis at $1.5 billion in just three years. And we are happy so far. But it’s a 10-year development process,” says Moynihan. The return on invested capital plan typically holds that these investments should be profitable within three to five years.

“We couldn’t plan for organic growth like that were it not for our operational excellence,” he adds.

Operational excellence is the catch-all term for the bolstering of the bank’s bones, simplifying products, retiring 18,000 redundant apps and duplicative processes, the single teller platform, reduced data centres and the rest. Part of operational excellence is also connecting divisions of the bank so that, having identified the right customers to deal with, Bank of America can try and do more with them.

This all works much better in the home market, where the product offering spans everything from consumer to wealth management and from small and mid-market business banking up to investment banking and capital markets, rather than outside America where the bank deals mainly with multinational corporations and institutional investors.

Is it really a global bank?

“We actually have more funded corporate loans outside the US than inside the US right now,” says Moynihan. “We set out almost 10 years ago to build our global transaction services business patiently and steadily, and stuck at it while some banks that had the same ambition have not been able to stay the course. But we don’t look at revenue regionally. Is cash management for the US subsidiary of a French multinational, French or US revenue? I tell our people that I just don’t care. And what’s more, they should be glad that I don’t.”

Euromoney has reported extensively on the build out of Bank of America’s global corporate and investment bank. It remains a global leader by volume and fees in investment-grade bond underwriting and loan arranging and has pulled itself up the M&A adviser rankings.

In March, it was named a lead adviser to RWE of Germany in a complex $74 billion asset exchange with E.On involving the sale of a big stake in Innogy. It is the biggest deal announced this year in Europe, a landmark transaction that promises to transform the German energy sector, creating two national champions with differentiated businesses: one in energy generation, including renewable, the other in transmission through customer networks.

Last year, it lead-advised a consortium of Hillhouse Capital, CDH Investments and the management of Belle International, the largest ladies footwear retailer in China and a large distributor for Adidas and Nike, on the biggest ever all-cash take-private acquisition of a Hong Kong listed company. It sole-underwrote a $3.6 billion bridge loan for the consortium for a credit in an out-of-favour sector. Bank of America’s bankers may have had their tongues in their cheeks in using the code name Cinderella for the deal, but Belle has performed well since and refinanced its debt on better terms, with Bank of America once again in the lead.

As it now looks to grow, the bank says it has the same hurdle rate of return for investments at home and abroad. For all this, it certainly sounds as if the organic growth the bank hopes to harvest is more abundant in the US, where the bank has a small army of middle-market lenders pursuing business in 90 separate markets.

“In the US, there are many mid-size companies that may have $2 billion a year in revenue and would be considered large companies anywhere else,” says Moynihan. “We have so much more we can do for these companies. For example, we think we only have a single digit market share of their capital markets business. They do a lot with the regional banks. Why not with us? I think we can win a lot more of that business, which I see almost as a form of embedded operating leverage.”

Increasingly these kinds of mid-market US companies, even ones closer to $500 million in revenue, now command a global presence, and its international reach gives Bank of America another chance to make itself useful.

“Treasury services is all about scale now,” says Donofrio. “Yes, being in 38 countries does bring some regulatory complexity, but once that machine is built, it doesn’t cost any more to move money from Michigan to India or Thailand than it does to Ohio. If we have a small manufacturer in Detroit buying raw materials from China, we will win that business in competition against a large domestic US bank because we can open accounts for the company in China, handle their payments, manage their risks.”

The bank can also advise mid-size customers strategically.

“We have been in India for 50 years,” says Moynihan. “We had our India country head recently come and talk about the Indian market to a group of mid-size US corporations and they find that very useful.”

It also wants to flex its muscles on these companies’ behalf.

Moynihan shares the story of a mid-size corporate in the US northeast that occasionally worked with Bank of America.

“It had been subject to one of those ‘I am the CFO, please immediately transfer cash’ scams and had sent $10 million out of the country,” recalls Moynihan. “Its main banks couldn’t really help this client. But because we know the correspondent banks well and do a lot of business with them, we were able to get its money back.”

It’s fair to say the bank is doing a lot more with the company now.

“It’s the kind of thing that changes the way a client thinks about Bank of America,” says Moynihan.

Sustainability is not a fuzzy thing

Bank of America is widely recognized as a leader in financing sustainable energy. And its leaders have twigged that the bank cannot thrive if the communities it serves don’t thrive too.

Bankers all love sustainability these days. Spouting about it lets them play at being good citizens and deflect the enduring criticism since the financial crisis that their industry is full of crooks who preyed on customers, looted shareholders and then came pleading to taxpayers for a bailout.

So, it is refreshing to hear Brian Moynihan take a pragmatic view.

“We committed $100 billion to sustainability before it was a thing,” he tells Euromoney, “because embracing ESG [environmental, social and corporate governance criteria] is the right thing to do economically. This is not a fuzzy, feel-good issue. Companies that balance all their constituencies, including communities as well as shareholders, customers and employees, perform better over time.”

In the energy sector, growth rates will slow in fossil fuels and eventually reach a tipping point, Moynihan suggests. Lending decisions need to take that into account.

“Now, you can’t go off a cliff on this,” he says. “In the US, 30% of electricity is still coal-powered. But we have to finance the transition to solar and other renewables. That transition may take time, but it won’t happen at all unless we start somewhere.”

Increasingly, sustainability considerations will influence credit availability to all companies, not just the energy sector.

“We deal with real companies. If they work with us and try and take their carbon content and waste production down, then that’s fine by us,” says Moynihan. “But if companies tell us they don’t care about any of that and won’t change, then we have to take that into account too.”

|

|

|

Anne Finucane |

Anne Finucane is vice-chair of Bank of America, having first come into the industry in 1995 as head of corporate affairs at Fleet Financial, making her part of what some rivals now unkindly call the Boston mafia that runs the bank.

Finucane leads the bank’s ESG efforts, stewarding Bank of America’s now $125 billion environmental business initiative, including a $10 billion catalytic finance programme to mobilize market capital into high-impact clean energy projects, which Moynihan unveiled at the UN climate summit in 2014. This year, the bank passed the halfway stage in investing that sustainability budget, with $66 billion mobilized to support clean energy, energy efficiency, water conservation, sustainable transportation and other initiatives.

Finucane says: “We are the leading underwriter of green bonds, a big issuer in our own right of green bonds and a leader in financing renewable energy, from wind farms in the North Sea to solar panels in Spain by way of land conservation in Africa.”

She also reels off a raft of other initiatives. These include a $50 million social impact fund investing in clean water in south Asia; a $50 million early stage loan fund for women entrepreneurs; and a so-called recidivism bond for the state of New York to finance programmes reintegrating released prisoners into society by offsetting the cost against the higher expense of returning those who re-offend to incarceration.

We had the chance to decide what kind of company we would like to be – Anne Finucane

“These kinds of deals can be difficult to do on our own, sometimes because the risks are too great or the returns too low or the pay-off too distant,” she says. “But we will always look at ways to work with others to get deals done, sometimes by creating tranches for different types of investor.”

Finucane defines ESG at Bank of America as being about “how we deploy our financial and intellectual capital and our technology to benefit the communities we serve.”

She claims that it permeates through the bank’s businesses.

“I look at the bond issue we led for Los Angeles to finance a change in street lighting from traditional to LED bulbs. If we didn’t have local bankers who know Los Angeles, capital markets bankers steeped in ESG round the table, that deal doesn’t happen,” says Finucane.

Like many on the executive committee, Finucane relates the embrace of ESG to the profound changes Moynihan sought to instil after 2010: “There were going to have to be so many changes for us to succeed that the thinking became: ‘Let’s just embrace this and let’s look into every aspect of the bank’. We had the chance to decide what kind of company we would like to be.”

The ‘thundering herd’ stirs once more

At most parts of Bank of America, the stretch for growth with no excuses is all about doing more with a select group of chosen customers, rather than hunting down new ones. But things are different at Merrill Lynch Wealth Management, the now US-focused firm of 14,000 financial advisers and 6,000 client associates serving millions of wealthy individuals and small businesses, with more than $2.4 trillion of client assets.

“Merrill Lynch always had the nickname ‘the thundering herd’,” says Andy Sieg, since January 2017 head of the division he first joined as an analyst back in 1992. “Well, the herd is moving again now. We are finally past the strategy first set back in 2001 of advisers concentrating on developing deeper relationships with fewer clients. We have turned the client acquisition engine back on. It’s a significant change of emphasis and there is great energy behind it.”

Andy Sieg, head of Merrill Lynch Wealth Management

That previous strategy had been set by James Gorman, now chief executive of Morgan Stanley, who in the years since the crisis has built the Smith Barney network of financial advisers acquired from Citigroup into a bulwark of his firm and a formidable competitor to Merrill Lynch. Sieg knows this well, having worked there from 2005 to 2009.

For now, the growth of low-cost index-tracking passive strategies has hit institutional asset managers harder than the retail distributors that can still charge a fee for allocating client assets among these cheap products. But leaders of the large firms that now dominate personal wealth management through the old brokerage model rest uneasy. They sense margins are set to compress.

Financial advisory in the US has always been a bit of a gig economy, with the best producers effectively running their own franchises under the brand of one of the big-name firms and periodically switching between them.

“Growth in wealth management used to come from hiring teams of advisers in what were effectively small M&A deals often at high multiples with a kind of initial goodwill payment and then generous compensation as the big wire-houses traded people between them,” says Sieg. “It wasn’t a particularly good experience for acquirers or for clients who kept having to re-paper at new firms. And regulators were raising their eyebrows.

“We have stepped away from competitive recruiting. Morgan Stanley and UBS have followed suit. But the good news is our client acquisition is ahead 65% year over year, even after eliminating adviser hiring.”

That sounds like a big increase, which makes Euromoney wonder how small the growth rate of new clients was until recently and whether or not the herd had grown a little lazy from grazing on rich pastures where it sat. That’s not wise as robo-advisory and cheap index-replicating ETFs change the marketplace and the price both for strategic asset allocation and tactical investment switches.

Sieg claims Merrill Lynch advisers have an advantage over firms like Morgan Stanley and UBS in the shape of a big consumer bank focusing on higher credit score customers, with the obvious potential to find wealthy clients among the households served.

Across wealth management, firms are suddenly looking for liabilities to earn margin from, as well as assets to advise on and invest for fee income.

“It is very advantageous to have the best suite of mortgage products for high net-worth clients, who these days may even take out a mortgage with us before giving us their investment business,” says Sieg. “Wealth managers at other firms typically have to outsource mortgages. It differentiates us that we can offer a broad range of mortgages sometimes on customized terms more akin to structured loans to high net-worth clients. It is a good way to learn a fuller picture of clients’ finances.”

I think what the phrase ‘thundering herd’ conveys is power and scale, as well as a sense of energy in the franchise – Andy Sieg

Sieg is almost taking the firm full circle back to the 1980s, when former chief executive Donald Regan first launched the cash management account (CMA) that combined FDIC-insured deposits and checking with a brokerage investment account. It was meant to be the new cornerstone of what business consultants back then breathlessly called one-stop shopping in financial services.

“We now have the capabilities to really deliver the CMA promise,” says Sieg. Merrill Lynch sources its own deposits that can in part fund those mortgages. “And we increasingly show pure Bank of America capabilities,” Sieg says. “Right now, maybe as few as 10% of Merrill Lynch customers bank with Bank of America on the CMA platform. We want it to become natural for new Merrill Lynch clients also to bring their banking relationships with them and to know that if they have an issue with their credit card, they can ask the same Merrill Lynch people who handle their investments to deal with that as well.”

The firm has had to be bold in pushing this new client acquisition strategy, deploying a carrot and stick in the one place financial advisers are going to sit up and take notice – their compensation package.

Financial advisers (FAs) are invariably paid on a complicated commission grid. Merrill Lynch has tweaked this.

“We are adjusting the grid up and down based on whether or not FAs are growing their business both by overall client assets and also by number of clients,” says Sieg. “There’s a neutral rate of growth, around 2.5% of net new assets, below which advisers are penalized but above which they can earn an extra percentage point on the commission grid.

“As with any change, some people don’t like it. But remember that FAs can now outsource asset allocation to our chief investment office, which frees them to focus on serving and acquiring clients. There are plenty of advisers who have been highly motivated by this and see it as their opportunity to earn a pay increase.”

We are not sociolinguists, but Euromoney cannot help wondering if the thundering herd quite fits with the new register of finance, which flits between environment, sustainability, inclusion and diversity. Does it say responsible growth or does it make Sieg the old Wall Street bull now being stared down by the statue of the fearless girl?

Sieg considers.

“I think what the phrase ‘thundering herd’ conveys is power and scale, as well as a sense of energy in the franchise, energy that, with this new change of emphasis, we are now releasing.”

Bank of America resists calls to separate chairman and CEO roles

Happy to discuss its record in sustainability, Bank of America is less keen to debate what looks like a key governance issue of whether or not Brian Moynihan should be both chairman and chief executive. Moynihan himself bristles, for the first time during the interview, at the notion there is anything wrong with this.

|

|

|

Jack Bovender |

“Jack [Bovender, lead independent director] leads the board. I lead the company,” Moynihan tells Euromoney. “That’s my job. It involves dealing with regulators and politicians, and in the US that task falls to the chairman.”

Moynihan doesn’t see this as weak governance.

“The governance committee of the board decides its members,” he says.

“Executives can suggest candidates but not approve them. The board is also in charge of succession planning. It’s part of my job to ensure a deep pool of managers with experience across the company who might be candidates to be chief executive one day. I’m only 58. I’ve got a few years ahead of me yet and I’m very intrigued about what comes next in banking. But whether I have this job tomorrow or not is up to the board.”

It is easy to forget that among all the other tasks facing Moynihan when he first became chief executive in 2010, he also had to repair relations with a dysfunctional board.

The board of Bank of America had not covered itself in glory in the lead up to Moynihan’s emergence as chief executive. The shotgun acquisition in September 2008 of Merrill Lynch had been urged by the Federal Reserve and the US Treasury.

But when big losses followed from old Merrill positions and a $45 billion taxpayer bailout became essential, those same regulators ignored their own role and launched investigations into the adequacy of due diligence and whether these risks had been properly assessed or perhaps hidden from shareholders.

There is nothing I would do differently if you called me the chairman instead of the lead independent director – Jack Bovender

Former chief executive and chairman Ken Lewis took the rap. But the board struggled painfully to recruit a credible outsider – one who could not possibly be tainted by association with the Merrill Lynch deal – to come in as chief executive and repair the damage.

Rumours had plenty of big name bankers being approached – including Bob Diamond at Barclays and Michael O’Neill at Citigroup – but none were even willing to start formal interviews. Moynihan was thus undermined at the start.

“Brian had been there for six years and yet he was still deemed an outsider by many of the insiders,” says one departed veteran. “In a way, everyone was an outsider, having all come from different predecessor firms. There was no unified culture among the top executives. And there was no unity on the board either, which had directors that had originally served on boards of predecessor banks, alongside various retired generals and admirals.”

The Fed now urged an overhaul of the board and a search for more directors with relevant previous executive experience.

This process was still not complete Jack Bovender, the former chairman and chief executive of Hospital Corporation of America, was first approached to join the board, which he did in 2012.

“To give you a flavour, I was taken aside by one director who told me: ‘I just want to let you know that I did not support you coming on to this board. But please don’t take it personally. I didn’t vote for any of the other candidates either,’” recalls Bovender.

Relations now are much more collegial between the board and executive management. Bovender explains how governance works to the non-American: “It’s a matter of semantics. In the US governance model, we combine the chairman and chief executive roles. Now there are often transitions when a retiring chief executive may become chairman for a year or so, as the new CEO settles in before also becoming chairman.”

This is usually a temporary separation, says Bovender: “In the US, there is a risk if the CEO is not also the chairman after a certain period that the perception grows of a hidden problem or lack of trust.”

Even so, some shareholders have in the past required votes at the AGM on splitting the chairman and chief executive roles.

“My thought is that there is nothing I would do differently if you called me the chairman instead of the lead independent director,” says Bovender.

“I talk each quarter with regulators. I meet our shareholders often. I conduct executive sessions on the board without Brian present. I have even advised him that if the vote ever passes to split the chairman and CEO roles, that we simply do away with the chairman title. He should carry on as CEO, I should carry on doing what I do as lead independent director.”