Australia doesn’t have a strong international reputation on climate action. Several of its recent leaders, including incumbent prime minister Scott Morrison, have sounded dismissive or even cynical about climate change. Others, notably Malcolm Turnbull, have been ousted from office for trying to do something about it.

But this country-level reputation masks real progress elsewhere. A combination of sharpened attitudes among pension funds and a willingness to change among corporates, prompts many bankers and investors to speak of a sea change over the last 18 months or so.

This is visible first of all in the capital markets. “On the green and sustainability-linked bond side we’ve seen tremendous growth over the last few years, from both the public sector and the corporate side,” says Max Thomas in the environmental, social and governance (ESG) solutions team at HSBC. “Corporate issuance is almost double 2019 volumes and we still have three months of the year left to go. On the loan side the growth has been even more dramatic.”

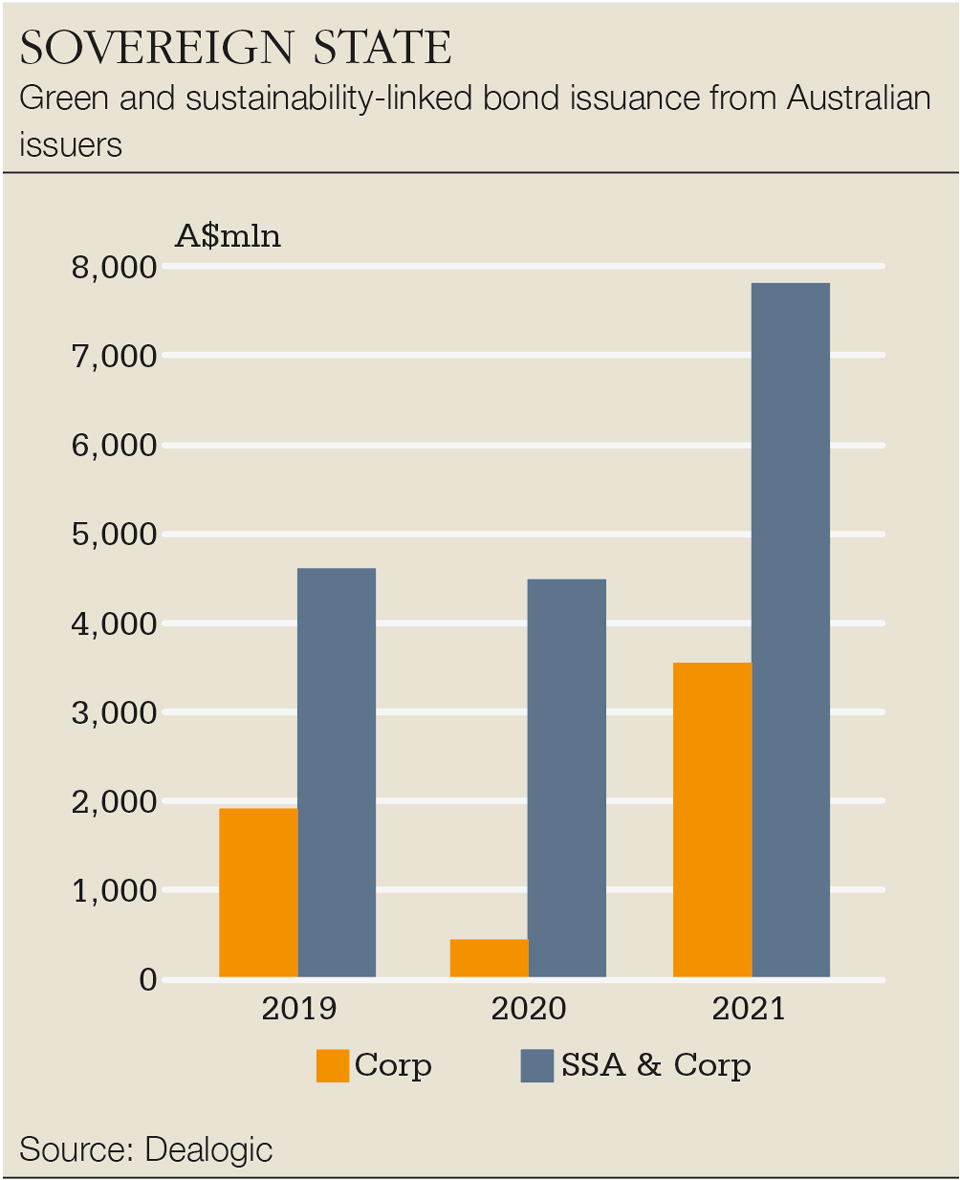

Indeed, figures from Dealogic show that for bonds from Australian corporate and sovereign, supranational and agency issuers, the A$7.8 billion ($5.6 billion) of issuance year to date by September is well on track to double the A$4.49 billion of 2020 and A$4.6 billion of 2019.

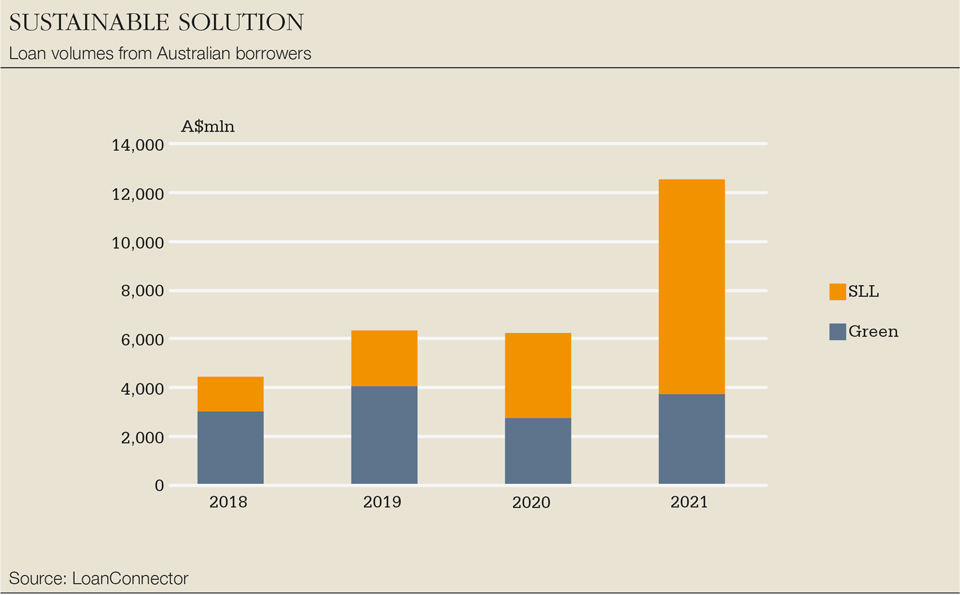

And according to LoanConnector, the sum of green and sustainability-linked loan (SLL) volumes from Australian borrowers in Australia stands at A$12.6 billion, compared with A$6.32 billion in 2019 and just A$4.41 billion in 2018. Hamish Kelly, HSBC’s head of global banking in Australia, says that in 2021, 20% of syndicated loans have been in sustainability-linked or green format. “That’s roughly one in five mandates and a big change.”

At the heart of this change has been a shift in demands of investors. This manifests itself most clearly in the powerful superannuation (pension) industry: an A$3.3 trillion asset pool as of June 2021, one of the largest pension fund pools in the world, despite the country’s modest population of 25 million. And the super funds are themselves being pushed to change by new attitudes in their underlying membership.

“Four years ago, it was a tiny sliver of the general membership of super funds [that cared about climate] and the focus was just thermal coal: if you’re exposed to thermal coal that’s a no-go area and we’re going to storm your offices,” says John Pearce, chief investment officer of Unisuper, one of the largest industry funds with over A$100 billion in funds under management. “Four years on it’s not just thermal coal but the whole fossil fuel spectrum. And it’s not just a cohort of the member base that is passionate about climate change; it’s well and truly mainstream.”

Government policy will be important, but it’s the consumers and major corporates that are going to drive this momentum at a global scale

Kate Vidgen, Macquarie Group

One can measure the shift quite precisely through Unisuper’s regular reports on its commitment to becoming a net-zero emissions fund by 2050, a common promise among super funds. In a report on August 18 this year, Unisuper said 40 of its top 50 Australian investments had set targets aligned with the Paris Agreement and a further five have committed to doing so by the end of the year. Four years ago, Pearce says, only a handful would have had Paris-aligned targets. In 2017 only 6% of companies in the fund’s global portfolio did so and they were mainly in Europe.

“CEOs and chairs don’t wake up in the morning and find religion on climate,” says Pearce. “They respond to pressure from shareholders.”

In time, these forces push their way through every level of industry and investment. Kate Vidgen, head of industrial transition and clean fuels at Macquarie Group, speaks of a multiplier effect. “That is, the large corporates have had to set targets and those targets will filter down. Already, it’s not just the big end of town that’s looking at emissions, but targets are being set across all value and supply chains.”

And the speed of action is another shift. “A big change of the last 18 months is that previously executives would set a target and think: it’s the next generation of executives who are going to have to deal with executing on that target,” says Vidgen. “But now there is accountability today. CEOs who go and do investor presentations to investors say that what they’re being asked is: ‘Tell me what you’re doing today, not just your targets.’ The super funds have really led the charge on this.”

The whole industry is seeing this and everyone has an informal metric to illustrate it. Jason Steed, head of Australian equity research at JPMorgan, says that in the August reporting season, the number of slides in results packs related to ESG matters roughly doubled. “There has been a tectonic shift in the past 12 to 24 months,” he says.

And Ian Campbell, head of debt capital markets for Australia and New Zealand at Citi, says: “My time spent on ESG has gone from maybe 20% to 30% last year and before to 50% of my time being spent talking about issuance strategy and financing and integration frameworks.”

Landmarks

It wasn’t always like this, and we should be careful of presenting Australia’s progress as anything more than catching up with many other developed markets. But the shift is real and the capital markets offer the most visible illustration. This year has brought several landmarks that wouldn’t stand out particularly in Europe but are significant steps in Australia.

One example was a A$750 million green mortgage-backed securitization by Australian non-bank lender Firstmac, arranged by JPMorgan and backed by the Japanese bank Norinchukin and the public-sector Clean Energy Finance Corporation (CEFC).

“It was a meeting of three like-minded parties,” says Joonas Keranen, associate in the securitized products group at JPMorgan. “We came together and created a completely new green mortgage product.”

You can hand on heart say: these home loans are green

Joonas Keranen, JPMorgan

The homes funded through the securitization are among the most energy efficient in Australia. There is an Australian standard called the Nationwide House Energy Rating Scheme, which has a ranking from one to 10 on energy efficiency. Whereas New South Wales standards, for example, are broadly in line with a standard of six, the new green home loans on this deal set the target at seven or higher. The securities themselves comply with the pre-issuance requirements of the Climate Bonds Standard for Green Bond Issuances. “You can hand on heart say: these home loans are green,” says Keranen.

It is hoped this will be the first of many to use the structure. “On the back of the Firstmac trade, we went on and spoke to the majority of non-bank lenders here in Australia and it seems there is a huge push from all the stakeholders in these institutions to launch something quite similar to this deal,” Keranen says. Non-banks are starting to originate green home loans that can be distributed to investors both in Australia and offshore, and those investors are lining up with ESG mandates. It looks promising.

In September Australian supermarket operator Woolworths launched a €500 million 2028 sustainability-linked bond, its first, in the European market, a closely-watched deal. The bond is linked to emissions reduction performance, with, as is commonplace in these bonds globally but rather newer to Australia, penalties for failing to meet these targets. The deal was structured by HSBC with Citi, BNP Paribas, MUFG and SMBC Nikko as joint bookrunners.

It went well. The deal was upsized to €550 million by the time it launched, with widespread demand. But its significance was more about what it represented: taking Australia to an extremely discerning and experienced ESG base.

“The European market is still the most advanced ESG investor base in the world,” says Thomas. “In tapping into that market they engaged with some of the most forward-thinking investors and many dark green investors in Europe came in strongly.”

In truth Woolworths had a reasonably smooth ride in Europe. “We probably expected a higher degree of questioning on ESG than we ended up getting,” says Campbell at Citi. Partly this was because there was a lot of interest in Woolworths as an established green bond issuer but a first-timer in the European markets. It was also well credentialed on ESG standards and used a structure that investors were familiar with from Tesco’s sustainability-linked issues.

“It’s pretty clear Woolworths did a good job based on the demand, the lack of questions on the structure and the ultimate price outcome,” Campbell says. “They achieved what they set out to achieve, including diversification of funding.”

That should then have a knock-on effect on other issuers. “It’s not as scary when someone has done it before you,” says Campbell. Woolworths was actually the third deal of its kind: engineering firm Worley brought the first with a €500 million five-year Eurobond in June. There are now reasons to have confidence that the right Australian issuers can brave the European markets with sustainability-linked structures.

And that’s a big step forward. “When we were suggesting clients do a bond with KPI [key performance indicator]-based penalties built into it two years ago, no one was willing to support that,” says Campbell.

The shift from green bonds to sustainability-linked, which we have seen in multiple markets now, appears to have been particularly transformational in Australia.

“Green bonds are use-of-proceeds bonds: you need to have assets that meet certain criteria,” says Campbell. “But for the majority of Australian companies, unless you have a wind farm, a solar farm or other eligible assets that you can ring fence the money for, that’s difficult to build critical mass, which is why we haven’t had that many green bonds from corporate Australia.” Many of the larger green assets are yet to emerge or are owned via agreements or sold internationally, so there is a shortage of supply.

“But sustainability-linked, where the use of proceeds can be fungible and where there is a broader application such as decarbonizing my business, that is starting to attract more focus.”

We are at the turning point where investors are willing to take the tight spread because of their ESG mandates

Stephen Magan, JPMorgan

That’s a natural alignment of assets and priorities. “We don’t have many companies knocking the door down saying: ‘I’ve got a billion dollars of green eligible assets today,’” Campbell says. “But we have a lot of companies saying they understand ESG, they’re eager to understand best practice and get their organization aligned, they don’t want to be the last mover that impacts the cost of capital, they want to decarbonize.”

Again like other markets, now Australia has to undergo an evolution in pricing.

“The challenge with all these green transactions has been: how do we come up with a transaction that means the consumers get a cheaper loan for being green, so you reward the consumers?” says Stephen Magan, head of the securitized product group at JPMorgan.

Historically, in Australia a green label has not led to any tighter pricing, so the originator won’t have any cost savings to pass on to borrowers. “Without that tighter pricing, you’re not really going to get things moving, nor get to the overall design objective, which is to get people into greener homes.

“But we are now at the turning point where investors are willing to take the tight spread because of their ESG mandates,” says Magan. “You will see green transactions price tighter, that price will go through to the consumer and then you will see meaningful growth.”

In mainstream debt, a similar evolution is under way.

“Does this become the normal market, where if you are not issuing in ESG format, you pay a wider spread and ESG becomes the new fair value?” asks Campbell. “Yes, I think that’s possible, because the volumes and interest from investors and the broader community is going to continue to rise.”

And even if pricing doesn’t move, Woolworths shows how an ESG bond can open a whole new investor base. “We wouldn’t expect a dramatically different pricing outcome, but where we do see the difference is in the investor engagement and distribution,” says Thomas. “With ESG investors participating in these deals you have the potential for broader and more granular demand, which gives clients more options for executing the deal.”

‘Commodities are key’

The climate journey has been challenging for Australia because of the nature of its economy. Resources and commodities have always been a key part of Australian prosperity and despite the progressive talk one hears in Sydney and Melbourne, there are plenty of other voices too. This journalist spent half of 2020 researching a book amid the Queensland coal mining industry and can report that not everyone is on board with ideas of climate change mitigation or even the idea that man-made climate change exists.

In this environment it is crucial that transition, rather than outright replacement, is to the fore: that there is recognition that not everyone can flick a switch and go green overnight. Also, mining is going to be more enduringly important than one might think. “For example, for the world to decarbonize, the world needs steel, the world needs copper,” says Pearce. “Producing these things is emission intensive. We have to accept that.”

[Climate] has been an incredibly divisive issue in the political arena

Jason Steed, JPMorgan

A good example of this was BNP Paribas refinancing a bond for Pilbara Minerals in order to develop a lithium project. The $110 million senior secured debt facility it arranged was put together in partnership with CEFC.

“The interesting aspect of Pilbara, in addition to its own decarbonization ambitions, was to underline the role Australia has to play in supplying metals of the future,” says Chris Ruffa, co-head of investment banking in Australia for BNP Paribas, with a focus on energy and infrastructure. “That’s lithium, for obvious reasons, but also copper and nickel. You can’t build transmission lines and wind farms and contribute to the electrification of the global economy without those basic commodities.”

Thomas at HSBC, one of the biggest lenders in the sustainability space, agrees. “Commodities are key,” he says. “Without the extraction of certain metals, the energy transition won’t happen. We won’t achieve the levels of electrification required without copper and tin, and we won’t be able to decarbonize our energy systems.”

Thomas says that there needs to be recognition that helping companies become greener, if not outright green, is worthwhile and in fact essential. “We need to work hard to structure deals supporting those companies and clients with good, robust, ambitious strategies and methodologies to transition to a low-carbon economy,” he says. “These are deals where we can make a significant difference, hitting the heart of issues where our clients are setting ambitious targets.”

That message does appear to be getting through and with it come opportunities for banks. One is to look beyond the wind farm and the solar panels and to think what else that infrastructure needs.

“Australia has had a pretty remarkable run in terms of the level of renewable penetration,” Ruffa says. “So increasingly, banks are turning their minds to adjacencies to support current and future green penetration.

“That could be reinforcing the network to accommodate the shift in generation mix in the market. It could be capacity, dealing with the fact that solar plants aren’t able to generate electricity in the evening so you have to capture excess electricity generated during the day.”

BNP Paribas has been involved in a host of groundbreaking ESG transactions in Australia. Examples include the Downer sustainability-linked loan, which was Australia’s largest SLL in 2020, and a A$140 million equity-linked green bond linked to Australia’s first forward-looking climate index, known as Project Green Kangaroo.

Vena was a unique project … It shows to the market how the private sector and banks are ready to step up

Chris Ruffa, BNP Paribas

Another example is the Wandoan battery project developed by Vena Energy, a A$120 million battery energy storage system, the first of its kind to be funded with a privately procured financing in Asia Pacific.

“Vena was a unique project,” says Ruffa. “It was a standalone battery not linked to a specific renewable project; it was connected to the grid. But there was significant lender appetite, recognizing the pivotal role it plays in supporting renewable generation penetration in Australia. That appealed to the bank market.”

Although the public capital markets are beginning to embrace ESG, most financing of renewable assets themselves to date has been from private markets. This has a tendency to become self-fulfilling: quite often, listed renewable stocks are acquired by private capital seeking exposure, whether super funds or dedicated infrastructure funds.

Often, major institutional investors like super funds prefer to go direct. “Australian super funds have not traditionally been material direct investors in primary market bond or loan transactions, with investments instead flowing through outsourced investment mandates,” says Kelly at HSBC.

There is an interesting twist here. As super funds have started to bring their portfolio management in house, they can express their environmental preferences more clearly through public markets. “Why’s that important?” asks Jason Steed head of equities research for Australia at JPMorgan. “Unisuper, for example, has a member base of university teachers and professors, which generally speaking is a segment of society that is more active in looking at ESG-related matters and willing to voice their concerns. That means more money is concentrated in the hands of those who would tend to have a more active mindset around climate, social and governance issues.”

Many expect these funds to become more active in primary and secondary credit markets in particular. But in the meantime, there is a plainly insufficient stock of investable green assets in Australia.

“The universe of available assets is not large enough to satisfy demand. That has to change,” says Pearce. “At the moment there is too much money chasing not enough assets.”

For super funds, this presents a challenge: it never really makes sense to pile into clearly overvalued assets. “You can’t just do something because it fits in with a nice thematic,” says Pearce. “It has got to make sense in terms of economic outcome and some prices are not justified.”

Instrumental private sector

One of the interesting things about ESG progress in Australia is that it has come in spite of, rather than because of, the position of the federal government. The private sector has been absolutely instrumental because it has to be. Note that in the Vena battery transaction there was no government subsidy and no government offtake. Few deals like this have got away anywhere else in the world. As Ruffa says: “It shows to the market how the private sector and banks are ready to step up.”

Like it or not, climate is controversial with voters and industry. “This has been an incredibly divisive issue in the political arena: it has accounted for at least three prime ministers,” says Steed at JPMorgan. “So this has been less the political class, which has been very fearful of extending too far in terms of how they legislate around carbon and renewables, but about companies and investors doing their very best, in my view, making a meaningful effort to improve the emissions profile of their businesses.”

Consequently, market players who want to make a difference haven’t necessarily aimed at the government when seeking change.

“A lot of the tension in Australia is directed towards the government and the fact that Australia has not formally committed to net zero by 2050,” says Pearce.

“The message we give is: we understand the frustrations but we are not going to spend much time lobbying the government over this, because at the end of the day the fund doesn’t vote governments in and out. What we have influence over are corporates, investee committees. That’s where we are directing our attention.”

Vidgen at Macquarie agrees that there are other drivers beyond state direction. “Government policy will be important, but it’s actually the consumers and major corporates that are going to drive this momentum at a global scale,” she says.

But she thinks the idea of Australia being absent at a government level from ESG is too simplistic.

“Australia, like other jurisdictions around the world, does suffer in the division between state and federal government,” she says. “That makes it more complex.

“But we have some amazing conversations with all of the state and federal governments. The reality is if you’re doing something like trying to build a hydrogen hub, you want the right regulation around it; and we are finding governments flexible about the ways they can help beyond pure subsidies in a true public-private partnership.”

Nevertheless, legislation does matter, as it is hard to operate without clarity of rules. “Without legislation,” Steed says, “AGL and Origin have no certainty about what their regulatory landscape looks like in three, five, seven years; and that makes it very hard for boards to sign off on investments.”

Whether government stipulates it or not, Australia is moving towards the E of ESG in a way it never has before. The coincidence of direction between key investors and their investee companies is a powerful force.

And the pressure’s not going to let up. Vidgen notes that many investors have been pushing for remuneration to be linked to ESG targets. “These investors see that as an executive, when your short-term incentives are linked to emissions reductions, you reduce them in the coming year, not in year 10.”

Renewable energy the Macquarie way

Macquarie Group occupies a unique position in Australian ESG. The bank has invested in renewable energy through the infrastructure part of the business for many years. But the 2017 acquisition of Green Investment Bank, now Green Investment Group (GIG), accelerated the bank’s focus. There are now 450 people in this group worldwide and it has $17.6 billion of renewable energy assets under management, with more than 50 gigawatts of green energy projects in development, construction or operation.

Through this division, Macquarie: “Typically has invested in the development of new green energy assets, developing projects that we want to be attractive for long-term investors,” says Lachlan Creswell, executive director and head of the Green Investment Group for Australia and New Zealand. Sometimes Macquarie brings in partners as the development progresses, such as the Dutch Infrastructure Fund (DIF), which invested in the Kwinana thermal energy from waste project in Western Australia after GIG had brought the development to financial close. “As we develop and de-risk assets, we will then sell down to experienced investors,” says Creswell. In a presentation in June, Macquarie said GIG had more than 240 green projects in development.

Then on the advisory side, Macquarie arranges capital for renewable projects. An example is the bank’s advisory work for the Western Australian electricity generator Synergy, where it brought in DIF and the superannuation fund Cbus to build out renewable energy projects. “We approached that knowing that there is long-term capital looking for a particular type of investment,” says Creswell. “So whether it’s advising on funding structures for our clients or developing assets ourselves, we have that market interest in mind.”

Uniquely connected

Macquarie, therefore, can play this theme from many sides: investor, seller and investment banker. Either way it has been at the forefront for so long, with so much international experience, that it is uniquely connected, embracing green projects at a far earlier stage than almost any major investor.

It has therefore become a more than popular partner in renewables. Euromoney is aware of one recent opportunity Macquarie had identified in Europe, where there was a bidding war not for the asset for itself but even just to line up with Macquarie. Potential partners had to pitch with a fee structure, just to get to the start line.

So what’s the key to a successful project?

“The basics are risk allocation and access to relevant technical and commercial expertise to manage assets through the various phases of their life from construction into operation,” says Creswell. “And increasingly it’s a focus on: is there a growth pathway? Is there an opportunity to continue to invest in that particular strategy, rather than having to go off and compete to buy more assets and put them together?”

Macquarie’s track record makes it interesting to watch to get a sense of where industry priorities might go next. Right now, for example, Kate Vidgen, head of industrial transition and clean fuels at Macquarie, is spending much of her time on hydrogen projects. Again, this is partly about the gas and its applications, partly about adjacencies: one of the major barriers to the industry developing is sufficient storage and distribution technologies.

“There’s lots of funds being raised for projects in hydrogen, but at the moment the deals we are doing are, at most, A$10 million to A$20 million,” says Vidgen. “We do believe there’s going to be a J-curve in the deployment of capital in this sector. So our strategy is to invest small to establish options, get them developed and plan now for more significant capital deployment when we’ll need it in years three, five, seven.”

Long term

And the fact that a technology is difficult or not yet commercially viable is no longer a reason not to pursue it.

“There are projects where 12 months ago I would have said: ‘That’s nice, it’s a good site, but the economics don’t work,’” Vidgen says. “And now you’re seeing, because of societal pressure and people wanting to show a tangible path to decarbonization, these projects are being supported by long-term offtakes.”

Vidgen’s perspectives are particularly valuable because of the number of hats she wears in the industry. She is a member of the Australian Clean Energy Regulator board, which administers schemes legislated by the government around carbon emissions; and she is a non-executive director and chair of the remuneration and HR committee at Aurizon, Australia’s largest rail freight operator.

The GIG division is in a very good place: there’s decent money to be made in saving the world. “Sustainable finance is becoming the norm,” says Creswell. “Almost all banking covenants will start to have very significant disclosures around emissions.”

Vidgen adds: “The reality is super funds, like everyone else, are having to move up the risk curve. There is no shortage of capital.” But there is a shortage of assets, hence investors need to move their risk position if they want to deploy funds.

“That’s very interesting for us, because we are in some earlier stage assets, which naturally sit further up this curve, and that means there’s a broader scope of potential capital we can bring in,” says Vidgen.