Bank of America

Barclays

BBVA

BNP Paribas

Bradesco

CCB

Citi

Credit Suisse

DBS

Deutsche Bank

First Abu Dhabi

Goldman Sachs

HSBC

ICBC

Itau Unibanco

JPMorgan

Morgan Stanley

MUFG

Qatar National Bank

Royal Bank of Canada

Santander

Societe Generale

Standard Chartered

UBS

UniCredit

|

|

Welcome to the class of 2019, our annual examination of how our group of 25 of the world’s biggest global banks are faring. We have focused on seven metrics that we feel best illustrate the direction of travel for the industry. And we have stayed with the same group of banks, which offers a geographic and market spread that captures the key trends of the sector.

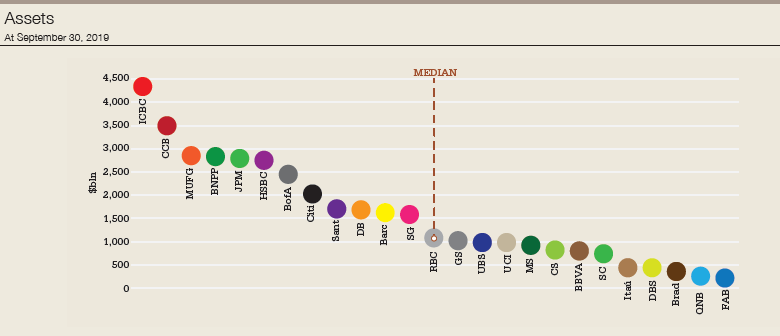

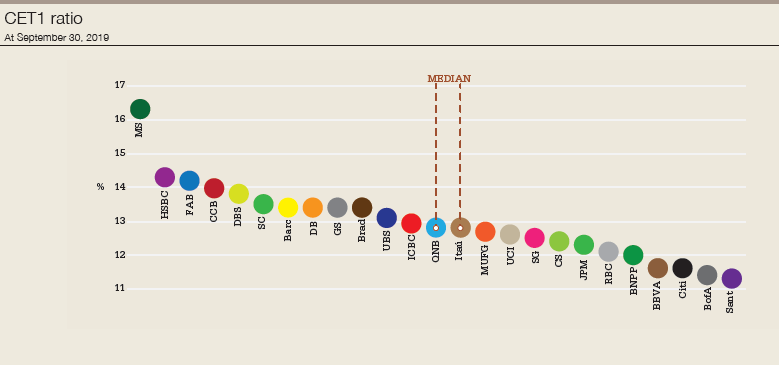

As our banks have generally not yet reported their full-year earnings for 2019, we have once again taken the first three quarters of the calendar year as our reference point. They are doing less with more. On average, capital – as measured by common equity tier-1 – is up, by 18 basis points to 13%. In dollar terms, the average balance sheet is also up, with assets rising 5% to $1.55 trillion.

But these rises are not yet translating into much in the way of gains elsewhere.

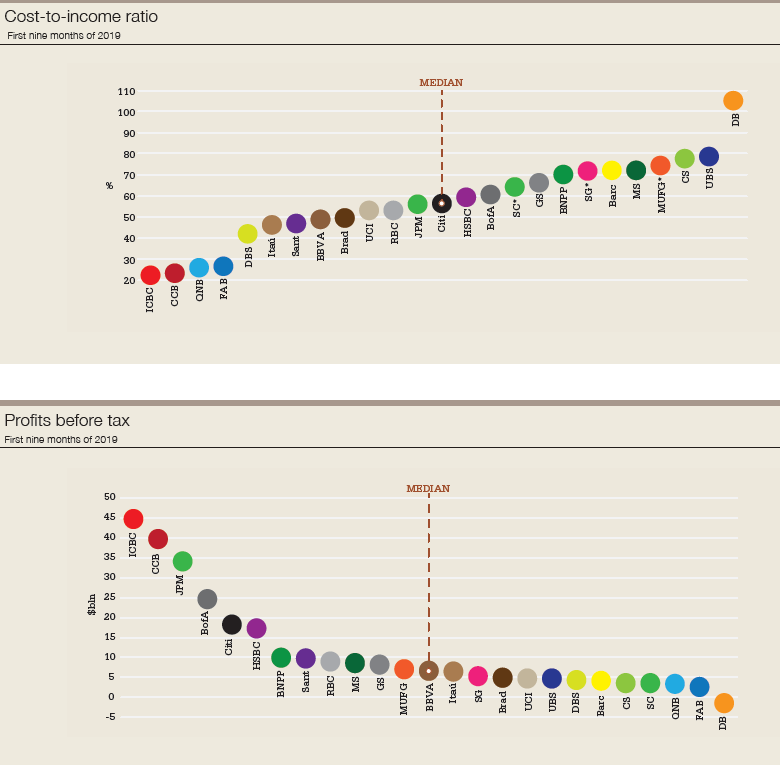

It is true that cost-to-income ratios have generally fallen: they are down at 15 banks within our group. But frequently the improvements have been very small. Stripping out the 15 percentage-point rise at Deutsche Bank, the average for the other 24 banks is 54.8%, only slightly better than 2018’s 55.5%.

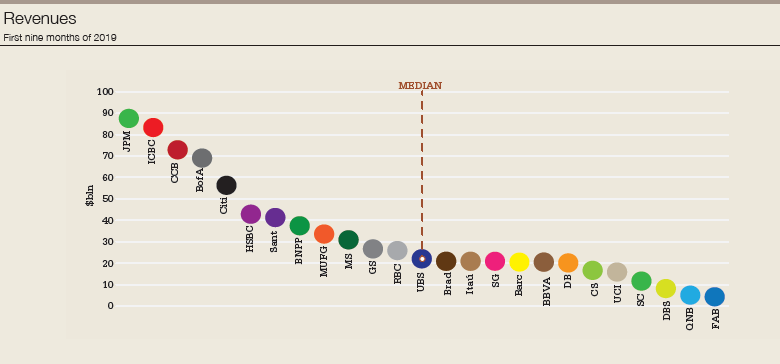

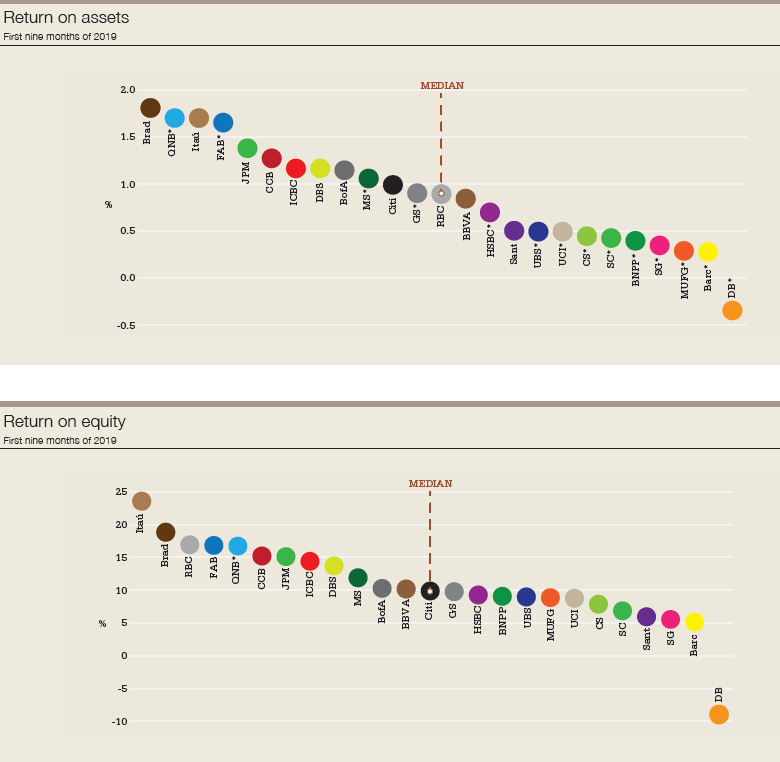

Total revenues for the 25 are up by a mere 1.1%, but the median has fallen 4.7%. Pre-tax profits are down 2.7% in dollar terms. For return on equity, the fall is about 100 basis points, a full percentage point drop from 12% to 11%.

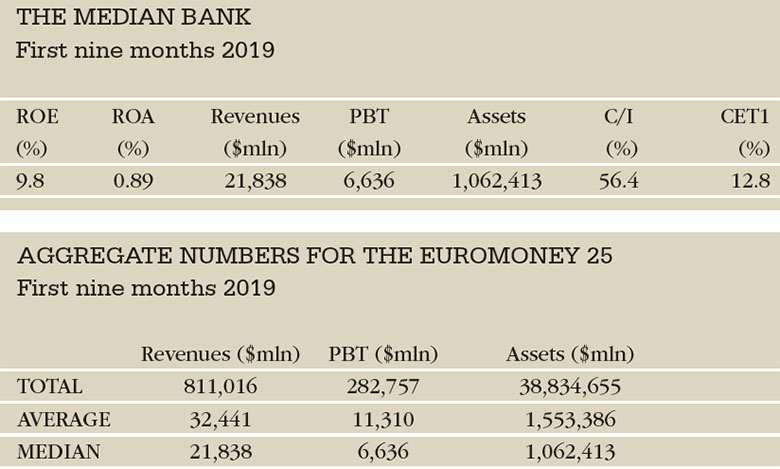

This year, our overall median bank has largely unchanged assets of $1.06 trillion. But return on equity is 9.8%, down from 10.8%; return on assets is 0.89%, down from 0.96%; revenues are $21.8 billion, down from $22.9 billion; pre-tax profits are $6.6 billion, down from $7.4 billion; the cost-to-income ratio is 56.4%, better than last year’s 57.3%; and finally CET1 has risen to 12.8% from 12.5%.

Which banks have made it to the prize-giving ceremony? Which ones need a detention and to put in some extra work? We reveal all.

The data

Disclaimers

All data as reported unless indicated by *

Figures within any category may not be precisely comparable between banks if reported numbers use adjustments

Where return on assets not reported, calculated by net income/average total assets

Banks use multiple different calculations for return on equity, and so may not be comparable

Where cost-to-income ratio not reported, calculated by operating expenses/revenues

MUFG fiscal year runs to end of March, that is its fiscal year 2019 begins April 2018. RBC fiscal year runs to end of October

CET1 figures are transitional where relevant. Where a bank reports Advanced and Standardized, the lower is shown

Assets, revenues and profit figures converted to dollars using the average FX rate of September 30, 2018 and 2019.

Bank of America

Barclays

BBVA

BNP Paribas

Bradesco

CCB

Citi

Credit Suisse

DBS

Deutsche Bank

First Abu Dhabi

Goldman Sachs

HSBC

ICBC

Itau Unibanco

JPMorgan

Morgan Stanley

MUFG

Qatar National Bank

Royal Bank of Canada

Santander

Societe Generale

Standard Chartered

UBS

UniCredit