Greenwich Associates recently published a survey of 87 investors – including institutional funds, insurance companies and asset managers in both the US and Europe, as well as US-registered investment advisers – that have used fixed income exchange-traded funds.

It finds that the overwhelming majority – 99% – were happy with the experience, including such factors as pricing, market impact and time to execute, and that 95% say they would trade ETFs again.

Some 60% of responding institutions have increased their use of bond ETFs in the past three years, with allocations now averaging roughly 18% of total fixed income assets. Greenwich concludes that the recent impressive growth of fixed income ETFs is set to continue.

Intriguingly, Greenwich finds that investors are using bond ETFs for much more than simply establishing a passive core to their portfolios. Just as many that use ETFs to hold market beta also now turn to ETFs as a liquid and low-cost way of gaining exposure to new markets and sectors to generate alpha and for making tactical adjustments to their portfolios.

The reasons are not hard to find. Concerns about deteriorating bond market liquidity have persisted through the last three years.

The situation appears particularly difficult in Europe, where an eye-opening 78% of institutions say trading, liquidity and security sourcing in fixed income markets has become more challenging. Over two-thirds of respondents reported that these changes are impacting their investment management processes.

“The banks don’t have as many positions on their balance sheets anymore, so they trade less,” a representative from an unnamed Dutch asset management firm wails to Greenwich.

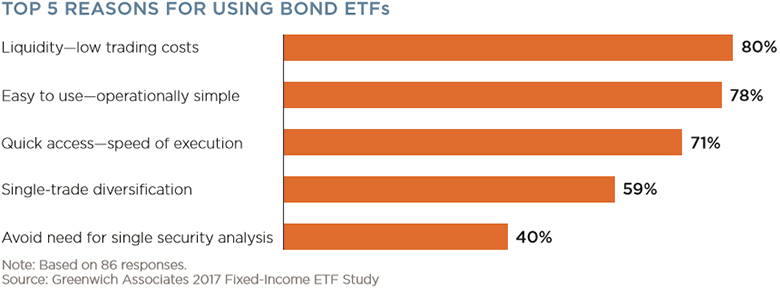

By contrast, it is easy and cheap to trade large blocks of ETFs.

Thirty percent of US study participants have executed a single ETF bond trade of at least $50 million, including 14% of institutions that report completing a single trade of more than $100 million.

This is how the cash bond markets themselves used to work years ago, when banks happily committed capital and financing – which was pretty much free – to accommodating their customers’ biggest and most strategic risk-transfer trades by taking on large principal positions while they found the other side.

‘Accelerated growth’

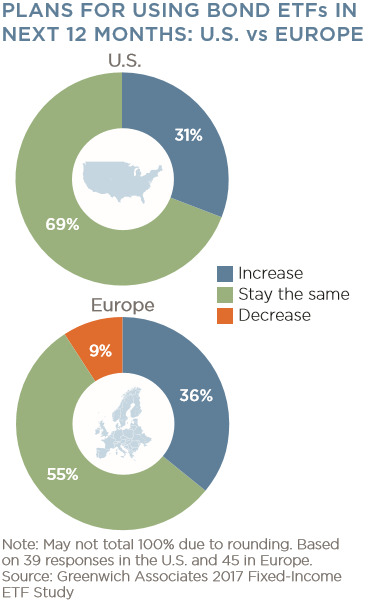

It sounds like ancient history. Now, Greenwich reports that one-third of current ETF investors plan to increase bond ETF allocations over the next 12 months, with European institutions planning to boost ETF allocations an average of 19%, and US institutions targeting increases of almost 30%.

|

Greenwich Associates managing director Andrew McCollum says: “Based on those results and investors’ continued concerns about bond market liquidity, Greenwich Associates expects steady and perhaps even accelerating growth in bond ETF usage and investment among US and European institutions for the next three to five years.”

In an earlier study published in May – looking at ETFs across longer established asset classes such as equities, newer uses in fixed income and emerging products such as commodity ETFs – Greenwich projected that total global institutional investment in ETFs will see $300 billion in flows annually by 2020.

Euromoney wonders if that is a good thing, given likely lower returns and higher volatility as rates rise, and whether investors have really found a solution to lack of liquidity in bond markets by buying liquid blocks in indexed portfolios. Like everyone else, we’ll be keeping a close eye on Italy, since the government published a budget in late September projecting wider than expected fiscal deficits of 2.4% of GDP over 2019-2021: this in the so-called good years for a country with public debt already at 133.4% of GDP.

“A failure to firmly improve fiscal sustainability while Italy is growing above potential could leave the economy exposed to significant risk come a future downturn,” says Dennis Shen, analyst at Scope Ratings, who adds that, notwithstanding the government’s optimistic growth projections, “the likelihood of Italy’s debt ratio taking an overall upward slope over a five-year horizon is non-negligible.”

Further pressure

It didn’t take long for bank analysts to start asking what it might take for Italy to be downgraded below investment grade; and what that might do to sovereign bond prices and to the finances of Italian banks whose treasuries have loaded up on these. The spread between Italian and German ten-year government bonds widened sharply in late September, in the days before rising US Treasury yields at the start of October put further pressure on European bond markets.

Sandra Holdsworth, head of rates and fixed income at UK investment manager Kames Capital, says: “It is worth mentioning, given the growth and popularity of passive and index tracking funds across the investment management industry, that these funds will not be able to reduce their allocation to Italian assets unless they are removed from their benchmarks.

“These funds of course are a low-fee way of accessing bond markets but you have to consider whether that is what you really want for your bond market allocation in this more challenging market environment. Low fees but full exposure to Italian bonds? Consideration of paying up for the optionality of not having that exposure must be worth a thought.”

Equity markets

|

|

Sandra Holdsworth, Kames Capital |

In the equity markets too, bankers are now beginning to worry about liquidity risk from widespread ETF ownership of small stocks.

Sebastien Lemaire, analyst at Société Générale, points out: “A trade is said to be crowded when positions are large enough to make exit costly. It is a key measure of liquidity risk. Lately, there has been growing concern about ETF crowding due to their size and expansion towards less liquid strategies.”

Lemaire and his team have begun compiling a database of aggregated ETF holdings relative to an individual stock’s free-float market cap and turnover and measured stock liquidity implicitly traded in the ETF. The aim is to compute ETF crowdedness based on stock crowdedness and index weighting.

Beyond ETF size, crowdedness is driven by the existence of multiple indices focusing on similar strategies and owning the same stocks, e.g. US small caps.

The conclusion is that crowdedness already exists, though it is for now limited to a few stocks and strategies. A hundred stocks, mostly constituents of the US Small Cap 600 and Nikkei 225 indices, turn out to be 20% or more owned by ETFs, with an average implied liquidity of 15%.

Is the greater liquidity of ETFs a mirage, enticing more investors into a trap that will close when the fundamental case for individual underlying cash assets collapses?

Italy may be a test case.

Fabio Fois, European economist at Barclays, says: “We believe that risks of a downgrade (by one notch) have increased remarkably following the publication of the revised deficit targets.” He adds: “Against the backdrop of weakening macroeconomic prospects, the likely aggressive deterioration of primary surplus conditions, combined with recent relaxation – and in some cases roll-back – of supply-side reform efforts, concerns regarding debt sustainability are likely to resurface, exposing Italy to swings in market confidence.”

Back in the bond markets, investors may be about to relearn the old lesson that prices can gap down in less traded instruments and that a few small trades can then impose new and sharply lower valuations on substantial passive holdings.