The potential for a bad debt crisis among China’s leading banks is one of the darkest fears circulating the world economy today. Corporate and local government leverage is high; there are concerns that stated NPL ratios do not reflect reality; the local debt market, though fabulously buoyant, is starting to look like an accident waiting to happen; and if China were to fall, then it would bring an awful lot of other things down with it.

In May, Euromoney spent several hours with the chairmen of two of the big four Chinese banks, and with the senior management of three. While these meetings were not for direct attribution, they do provide an interesting insight into how the biggest lenders in the country are facing questions of debt sustainability and risk management.

In summary: guarded confidence. “NPLs are surely a problem for Chinese banks,” says one of the chairmen. “But they are not as large a problem as people say.”

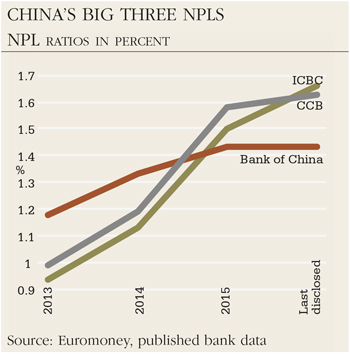

It is undeniable that NPLs have grown across the industry. Even taking only the big four banks, probably at the more prudent end of the Chinese banking sector, the numbers are clear. At ICBC, NPLs were 0.94% in 2013, 1.13% in 2014, and 1.5% in 2015 (and had reached 1.66% by the time of its first quarter results in April). At Bank of China over the same period, the figure has gone from 1.18% to 1.33% to 1.43%. At China Construction Bank, the figure was 1.19% at the end of 2014, 1.58% at the end of 2015 and 1.63% by March 31 this year.

|

None of these numbers suggest an endemic problem – when ICBC’s soon-departing chairman Jiang Jianqing took over the bank in 1999, the NPLs stood at 47.5%. But remember that ICBC granted new loans (not the total loan book) of Rmb2.76 trillion in 2015 alone. When you’re working on scale like that, the numbers are very big.

For example, ICBC’s first quarter total balance of non-performing loans was Rmb204.7 billion ($31.3 billion): yes, only 1.66% of lending, but that figure is, by comparison, bigger than the entire asset base of all but one bank in the Philippines.

“Rising NPLs in China’s banks are the direct result of an unprecedented five-year debt binge and a slowing economy,” says PricewaterhouseCoopers in a study which concludes that China’s official 1.59% NPL ratio at the end of 2015 would be more like 3%-5% if China followed international norms on recognizing bad loans.

“Over the last two to three years, the NPLs of Chinese banks have grown at a relatively fast pace,” says one of the big four chairmen. “The reason for this pace is because the Chinese economy is restructuring and is in a stage of destocking, reducing overcapacity. It is a process the Chinese economy must experience.”

NPLs, in his view, are more a function of the lack of growth than systemic problems with credit exposure. In this reading, it will be years before a new engine appears to push those growth rates back up and, logically, NPL ratios back down.

“We cannot say that the problem of low growth rates can be reversed in the next one or two years. The Chinese economy will grow faster after new industries replace traditional industries,” he says. “Then the leverage ratio of Chinese companies will decrease, and companies will become healthier and grow.”

In the meantime, ICBC, for example, which generated Rmb277 billion of net profit in 2015 despite negligible growth, deployed Rmb60 billion of cash to tackle NPLs that year, and is likely to do so in 2016 too. Should that fail to stem the tide of rising NPLs, the bank plans to do so again in 2017 and 2018.

“The worst position for a bank is to have high NPLs and low profit,” says one bank chairman. “We are very confident that in a few years’ time the NPL problems of our bank will be tackled.”

The problem is, this assumes that the actual failure rate of existing loans does not worsen dramatically, and there are reasons to doubt this assumption. In the first quarter of 2017, China’s total debt rose to 237% of gross domestic product, a national record and dramatically out of step with most emerging economies. The IMF is one of many world bodies to have warned that Chinese debt, if not properly managed, could become a global issue.

Chinese banks have reined in their lending practices out of concern. At China Construction Bank, for example, lending has been curtailed to any industry with excess capacity, notably iron and steel, cement and plate glass. Also lending to enterprises with leverage higher than 70% is closely controlled.

“We have established a credit management department to control credit risk, putting more emphasis on pre-loan due diligence and post-loan management,” says one bank chairman. “Previously, staff did not well understand credit policies and were not prudential.”

This chairman believes that “all the big Chinese banks have well controlled their loans to the high leverage ratio enterprises,” adding that he has pulled much of his bank’s lending from the retail sector for leverage reasons. “Since 2012 we have mainly issued loans to support quality infrastructure projects,” as well as a lot of personal loans, he says.

Instead, he sees reasons for concern in China’s burgeoning online lending marketplace. “Their weakness is inadequate risk control,” he says. “I think internet finance is not safe enough.”