For years, Beijing has been under fire from Washington for not letting the renminbi appreciate against the dollar to its market-implied value, with US policymakers arguing China’s illiberal currency stance is delaying the rebalancing of the global economy.

Against this backdrop, the IMF’s conclusion this week that the RMB was only “moderately” undervalued, citing a correction in China’s current account, as opposed to its previous stance that the currency was “significantly” undervalued was something of a bombshell in Washington.

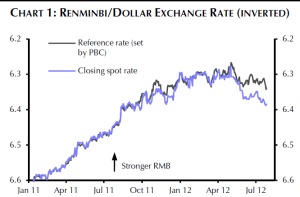

But, the gradual appreciation of the renminbi has taken a step backwards in recent months. Since May, the renminbi began to depreciate against the dollar, albeit only by 1%. This is the first sustained period of depreciation since the currency peg was loosened in 2005 – at the behest of the authorities.

|

| Source: Capital Economics |

For three crucial reasons, according to Capital Economics.

| The first was to break the taboo that has built up over falls in the value of the renminbi. The PBC has long needed to do this to make good on the promise of introducing more two-way movement in the exchange rate. With the market no longer seeing the renminbi as significantly undervalued and US political attention elsewhere now was a good time to shift. |

Secondly:

| …a weaker currency has obvious attractions when exports are slowing and inflation is falling. |

In May, export growth in China fell to 11.3% from 15.3% on the previous month as a lagging euro zone – China’s biggest trade partner in 2011 – meant that the demand for cheap Chinese exports has started to falter. By allowing the currency to depreciate, even this slightly, real trade losses may be skewed for the better. This is all the more important in a country where economic strength governs political and social stability. And thirdly:

| …we suspect that the PBC increasingly has one eye on the renminbi’s effective exchange rate. The bulk of the fall against the dollar came in May, just as the dollar was climbing against other major currencies. Indeed, the renminbi has still appreciated about 1% in trade-weighted terms since the beginning of May. In other words, recent weakness against the dollar has only partially offset the dollar’s strength against other currencies. |

In sum, the renminbi will probably trade effectively flat to the dollar by the end of the year, the research house concludes:

| The export outlook is poor, inflation looks set to remain low for the next few months and, on our forecasts at least, the dollar is likely to strengthen further against the euro. In those circumstances we can see nothing that would shift the PBC’s stance. |