One year into the global pandemic, the short-term emergency responses of central banks and governments from spring 2020 are starting to look like established features of the financial landscape.

European banks may be too dependent on them, adding to worries in a region where banks dominate provision of credit.

You have to expect that the asset side of banks will weaken, as government guarantees go away

Andreas Dombret

In February, national central banks in the eurozone will start accepting bids for the seventh allocation of subsidized three-year funding under the third targeted longer-term refinancing operations (TLTRO III) programme.

While the eurosystem processes these bids, the ECB is already beginning to fret about potential cliff effects on bank asset quality from the removal by overly indebted governments of fiscal support measures, including loan guarantees, offered in 2020 to keep defaults at bay.

Andreas Dombret, former member of the executive board of the Bundesbank and the Basel Committee on Banking Supervision and now a senior adviser to Deposit Solutions, tells Euromoney: “You have to expect that the asset side of banks will weaken, as government guarantees go away, and we then start to see the impact both on companies whose business models were already challenged pre-Covid and on those that have been challenged since Covid.”

He explains: “That is why the ECB continues to press banks to reserve for that weakening. And while there is no historical data for the credit impact of the pandemic, it is reasonable to expect it will turn out that some banks will have reserved adequately, and some will not.”

Meanwhile, the ECB’s own continuing support measures, now rather taken for granted, mean that banks may also be heading towards a second cliff on the liability side of their balance sheets.

Size of borrowing

Last year, the ECB adjusted the terms of the TLTRO III programme so that it pays banks anywhere from 50bp up to 100bp to borrow money from it, as long as they lend it out again to companies and households in anything other than mortgages.

Tim Sievers, chief executive of Deposit Solutions, tells Euromoney: “Look at how much TLTRO funding was taken up. The sheer size is quite astonishing.”

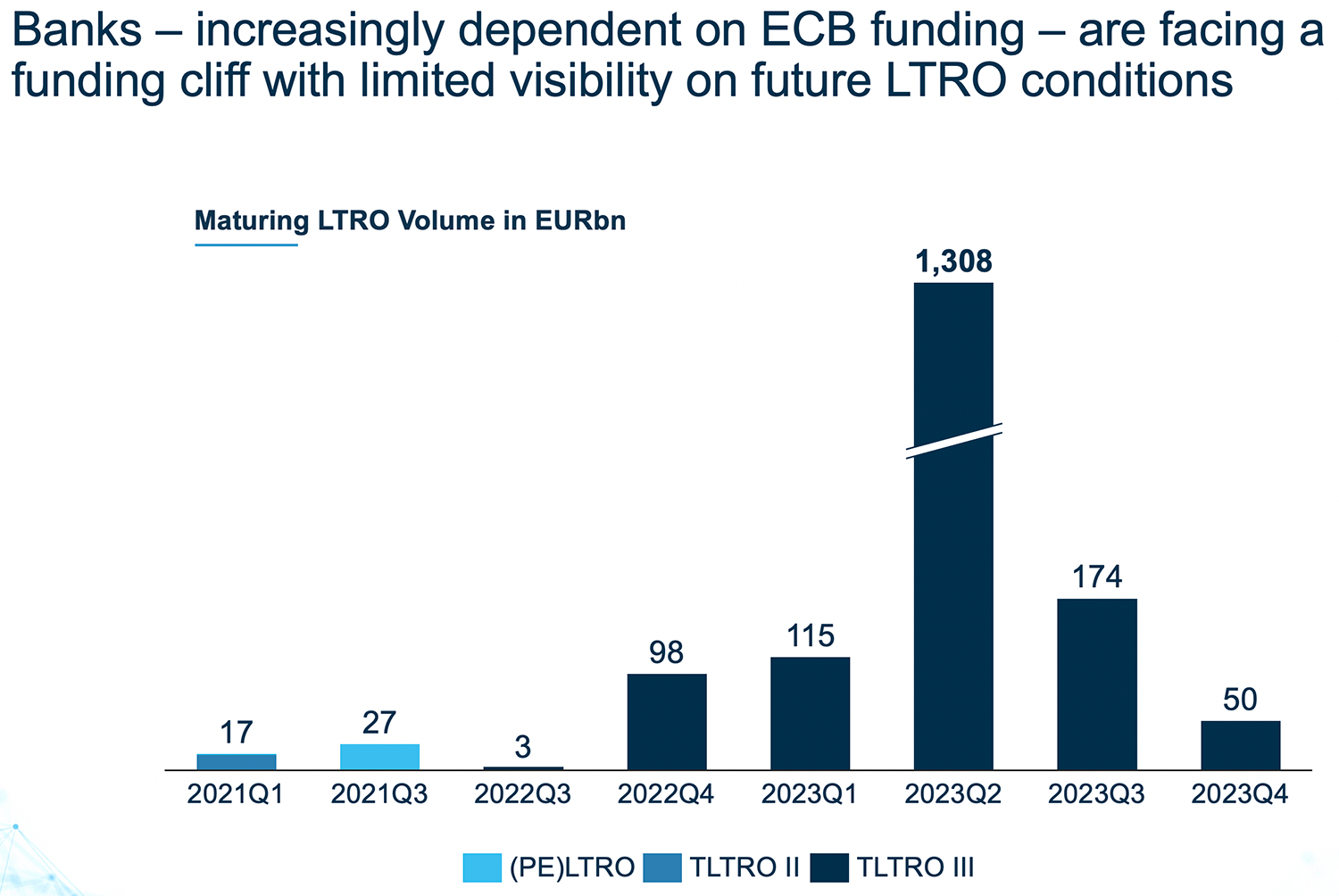

While more recent funding allotments have been sizeable – €50 billion in December 2020; €175 billion in September 2020 – European banks took down €1.31 trillion in June 2020.

Full-year data is still being assimilated, but by the start of the final quarter of 2020, European banks had borrowed €1.75 trillion from the ECB. That will have to be repaid or refinanced, while there is no guarantee that the ECB will roll over these programmes.

“And it’s not as if there weren’t other financing options,” Sievers points out. “Deposits have continued to flow into European banks – €400 billion of retail deposits in the first three quarters of 2020 alone – leaving the system in aggregate able to fund over 90% of loans. Not only is there now a refinancing cliff to come, there has also been a crowding out effect on customer deposits.”

Look at how much TLTRO funding was taken up. The sheer size is quite astonishing

Tim Sievers, Deposit Solutions

In the topsy-turvy world of negative rates, the ECB charges banks 50bp to store excess customer deposits that they cannot use to fund loans. So, any rational bank treasurer would grab an average 83bp payment to borrow from the ECB instead of from its own customers.

Autonomous Research estimates a boost of anywhere between €5 billion to €13 billion to bank earnings from this subsidy, equivalent to about 12% of 2019 profits. It suggests that further TLTRO easing could add 7.5% to annual profits through to 2022.

Banks may feel pressure to take up this cheap funding lest they be accused of not doing their best to support the real economy.

Let’s not forget: they’re part of the solution this time.

The danger for policymakers in prescribing short-term pain relief to banks under their charge is that patients become addicted.

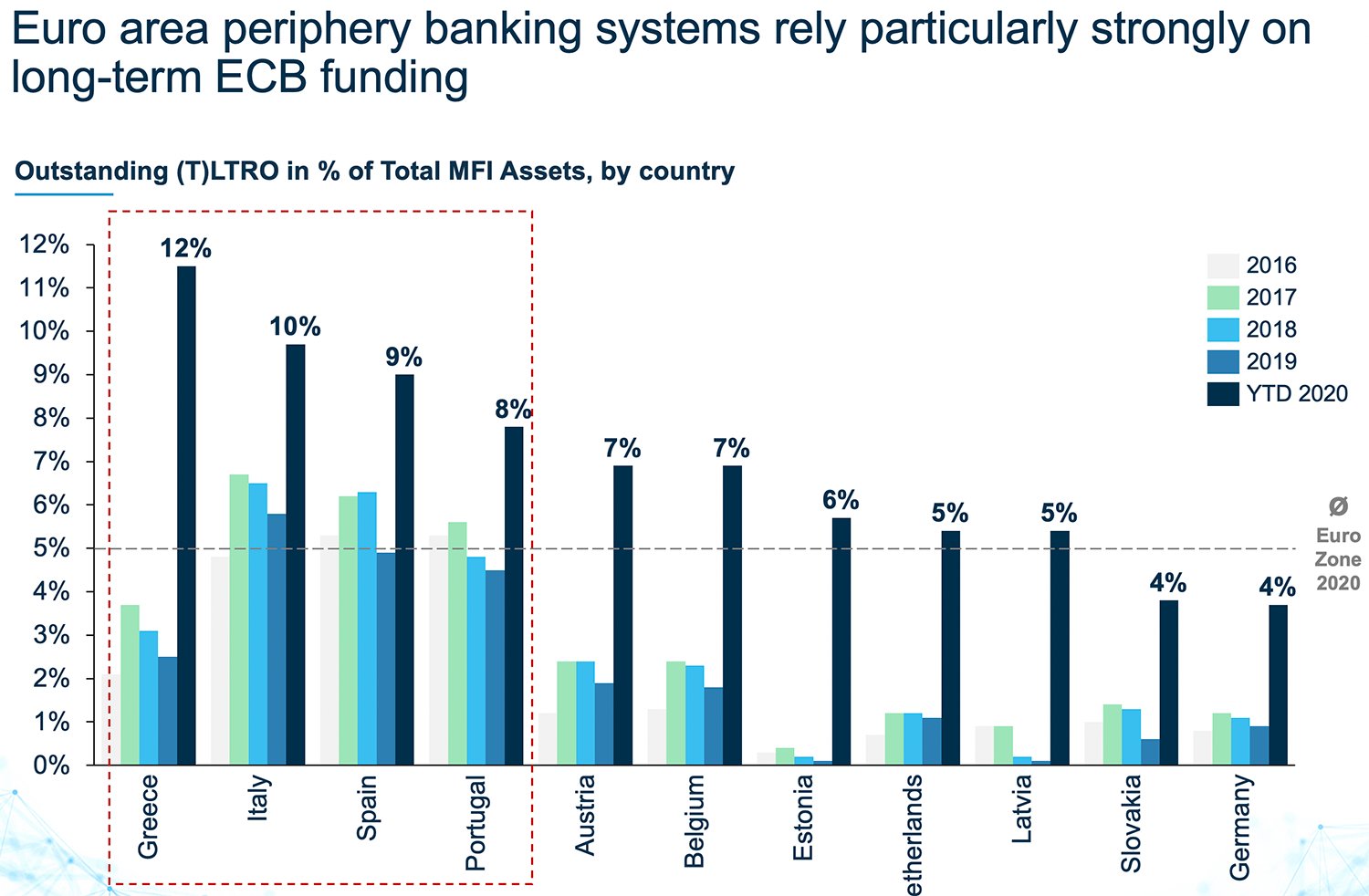

Deposit Solutions calculates that while French banks (€381 billion) and German banks (€333 billion) were particularly big users of subsidized funding last year, more than quadrupling their TLTRO drawdowns, it is in the periphery that banks may becoming dependent on the ECB for funding.

Outstanding TLTRO funding accounts for 12% of system-wide assets for Greek banks, 10% for Italian banks, 9% for Spanish banks and 8% for Portuguese, compared to just 4% for German banks.

The maturity cliff isn’t looming yet, but it looks quite precipitous starting towards the end of 2022, with just under €100 billion maturing in the fourth quarter. Another €115 billion comes due in the first quarter of 2023 and then the big one: €1.3 trillion maturing in the second quarter of 2023.

Dombret says: “The choice bank treasurers face right now is between keeping the full profit benefit of the TLTRO funding subsidy and willingly dispensing some of that to invest in alternative funding sources, which would be a good thing to do as it would make them more resilient, but which costs money.”

In its own November 2020 financial stability review, the ECB pointed to the hidden danger from record levels of reliance on central bank funding amid banks’ declining use of wholesale finance through the bond markets, particularly banks below G-SIB size.

Issuance by smaller banks in 2020 was 25% below that observed in the previous three years. The ECB stated that this “could pose financial stability challenges in the future, if central bank operations normalize more quickly than market depth can adjust”.

Away from issuing bonds, Sievers says: “We make the point to banks that there is an additional large addressable funding market in the form of insured deposits that they can access through our platform at low cost.”

Open banking

Deposit Solutions sees a €10 trillion market in deposits in Europe that is growing quite fast despite zero rates. Its open banking platform lets banks that are being flooded with customer deposits – Deutsche Bank, for example – enable customers to place those with other lenders that are more hungry for funding and that might even pay savers a tiny return on them.

It connects 200 banks in 20 countries and has intermediated more than €30 billion of deposits through its platform, reaching 30 million depositors across various channels.

None are yet questioning national deposit insurance schemes that would protect customers of a highly rated bank seeking a few basis points from placing savings with smaller banks.

“It has to be worth investing in these funding channels in good times for funding,” says Sievers. “You don’t want to be desperate to start accessing them in bad times.”

There are large forces at work here.

The ECB is paying a hefty subsidy to banks to borrow from it but telling them not to rely on this.

Retail customers are still flooding banks with deposits. UBS calculates that during 2020, deposits at European banks grew by €570 billion more than loans did, in theory further debasing their value to banks. But banks will not pass on negative rates to retail, presumably fearing that customers from which they profit through other products would be permanently lost to fintechs and neobanks.

These customers continue to view banks as contingent liabilities of the sovereign and dare not question sovereign debt sustainability.

There is no longer any semblance here of a true free market in bank funding.

The ECB’s warning over what might happen if central bank operations normalize too quickly seems bizarre. This is within its own control. If the ECB has built a funding cliff for banks, presumably it can also build a ladder to ease them down from it.

“You may think that, but it’s quite a dangerous bet,” says Dombret. “You can’t rely on it. That’s why banks need buffers including on the funding side.”