Is DBS becoming Asia’s bank? Could this decade be the moment a once provincial Singapore outfit sheds the last strands of its chrysalis and emerges as a pan-regional lender able to compete head on with the remaining handful of universal banks?

If that sounds far-fetched, think how far DBS has come.

“‘The Asian bank of choice for the new Asia.’ That was our tagline written in 2010, when were we were laggards,” DBS’s head of institutional banking, Tan Su Shan, tells Euromoney in her spacious corner office on the 46th floor of Singapore’s Marina Bay Financial Centre.

The word ‘laggard’ is carefully chosen, but the reality was far harsher: back then, DBS was nowhere, a poorly managed lender that lacked cohesion and direction.

Since then, external perception has begun to align with internal ambition.

Singapore’s economy held up well after the global financial crisis, an event that bathed the Lion City, with its regulatory prowess, strong banks and institutional solidity, in a soft warm light.

In the second half of the last decade, digital became DBS’s calling card. It wasn’t a first-mover, but in Piyush Gupta, an old hand from Citi, it had a chief executive secure in his position and shrewd enough to see disruption would start in retail before moving up the ladder into wholesale banking.

|

|

|

Piyush Gupta, DBS |

A man clearly comfortable in his own skin, Gupta draws a clear line between work and play. He is often found in Singapore’s Jurong Bird Park at the weekend in the company of friends, peering at Sundar woodpeckers and Crimson crested barbets through a pair of high-end Swarovski binoculars.

His positive management style, allied to a willingness to surround himself with clever and challenging division heads, helped DBS to secure first the title of best global digital bank from Euromoney then, in 2019, the mantle of world’s best bank.

In the words of a long-time colleague from Gupta’s Citi days, a one-time laggard was now “a supremely well-oiled machine, and a national and international champion.”

Meetings with senior executives in Singapore in February revealed a bank comfortable in its success – basking in it, even – but also confident enough to ask itself searching questions. Most notably: what’s next?

Critical stage

Surely the answer must be Asia. DBS is present in 18 markets, including China, India and Indonesia. It is Hong Kong’s sixth-largest commercial bank, where it is an entrenched and valued provider of services to the city’s small and medium-sized enterprises.

But there should be more. Asia is at a critical stage in its financial development, an interregnum between the retreat of many Western lenders and the inexorable outward sweep of China’s banks.

This is a once-in-a-generation period of transition, when a capable and savvy bank from a smaller market with tacit institutional benefits can emerge to fill the void. Can DBS be that bank? Gupta nods in agreement.

“This has been our investment thesis for 10 years, predicated on exactly what you said,” he replies. “Across Asia, local banks are just too local, China’s banks haven’t emerged yet, India’s banks don’t come out and Japan’s do, but they have limited capabilities.

“On the other side, international banks jump in and out of the region, and when they are here, they are an inch deep and a mile wide,” he adds. “When there is a down cycle, they come under immediate pressure from their board to be in low-return markets, so they tend to yo-yo back and forth.”

Examples of this vacillation include ANZ and Commonwealth Bank of Australia, which expanded in the first half of the 2010s before retreating to their heartlands.

To rely on Singapore is not sustainable. Our business needs to grow outside – China, Indonesia and India will help that – Piyush Gupta, DBS

That doesn’t mean DBS wants to be in every market. In 2018, it emphasized three arenas of growth: greater China, south and southeast Asia. Gupta in turn distils this list to six economies at different stages of development. More than a year on, that outlook hasn’t changed, he says.

“We are putting our chips on China, Indonesia and India, three markets with 40% to 50% of combined global growth, plus three rich, developed markets in Taiwan, Singapore and Hong Kong.”

Each market’s targets are calibrated.

In China, DBS has gone niche rather than big in a market where loans by foreign banks make up less than 1.5% of the total book.

“We are focused on the Greater Bay Area (GBA),” a sweep of land incorporating Hong Kong, Macau and south-central Guangdong province. “The key will be outbound business. We won’t be relevant to China, but China will be relevant to us.”

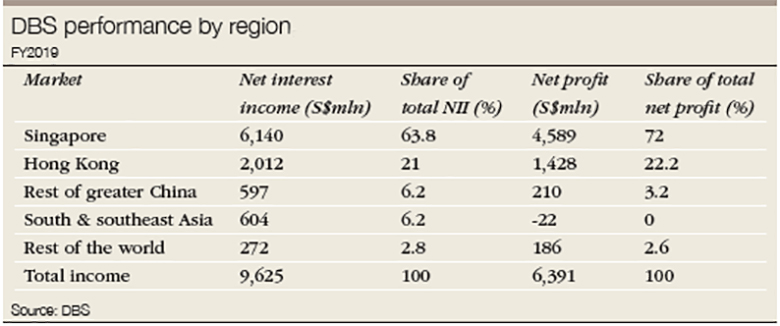

Greater China minus Hong Kong accounted for 3.2% of DBS’s net profit and 6.2% of net interest income in the full year 2019.

Most of the bank’s non-Hong Kong China book comprises lending to large GBA-based corporates and smaller firms with international ambitions, plus an army of wealthy mainlanders who see Singapore, not Hong Kong, as the safest place for their fortunes.

India and Indonesia offer different tests. DBS has invested heavily in its local digital offering in both, but learned from mistakes made in the first, where it cast its net too wide. In Indonesia it has narrowed its focus on a smaller group of retail clients.

Gupta is probably correct when he says that each of those target markets presents opportunities for lenders “with product capability and dollar funding, [and who are] able to play the game like a local bank”.

And he’s almost certainly right when he notes that two of the big corridors of global trade in the 2020s will be in Asia, linking north with south and east with west. DBS can be a valued ally to ambitious corporates keen to take on Asia, then the world.

But each market has risks and limitations. China’s economy is slowing, as is India’s, while Indonesia is a work in progress. The combined south and southeast Asia division posted a small loss in 2019 and accounted for less than 1% of net profit in 2018.

DBS is growing in both, but it must compete with local banks that have no intention of ceding market share.

Given that China’s capital account is still closed and India’s isn’t fully open, these countries are long-term plays.

That might explain why Gupta frames DBS as ‘Asia’s bank’ rather than ‘Asia’s universal bank’. It cannot hit every market, sell every product or serve every customer. Take Japan and Korea, where it is not very visible at present.

“There is a problem in having too many hobbies,” he says. “You can build a sub-scale business in too many countries. Cost-wise, that is a recipe for disaster.”

Stability

It’s worth taking a step back to remember how DBS got here. After all, good management will only get you so far.

Banks tend to grow in lockstep with their own markets, or when corporates and wealthy individuals want to do business with them rather than a lender from their home region. So why do so many ambitious young firms and individuals covet DBS’s products and services?

Head of institutional banking Tan admits the bank is “not going to be an HSBC or a JPMorgan”, a global lender able to bank a Siemens or a Unilever in every market.

Nor does it have Citi’s pulling power among MBA graduates.

Its products, notes one Hong Kong-based analyst: “Are good – under Gupta they have improved each year – but are their products and platforms as good as HSBC’s? No.”

On the other hand, unlike HSBC, it hasn’t been hauled over the coals by the US Department of Justice.

Comparing the two banks, the analyst says DBS is “just a little more flexible to deal with and gets accounts open faster and more seamlessly. I think of DBS as the default bank, a second-choice provider that many trust.”

|

|

|

Tan Su Shan, DBS |

That might seem a backhanded compliment, but there’s logic at work. Put yourself in the shoes of the chief executive of a big Chinese corporate or the head of a rich family.

“Many do business in Singapore, and they like DBS as a counterparty, as they believe its implicit government backing sets it apart,” says the analyst, alluding to DBS’s systemic status and the 11.11% stake held by the sovereign wealth vehicle Temasek.

“It is also an easy entrée to Singapore” he adds. “Perhaps you already do business with them in Hong Kong. In that case, it isn’t a big leap of faith to open an account in Singapore.”

And there’s a deeper issue at play here. The riots that rocked Hong Kong scarred its reputation as a destination for wealthy mainlanders; and Hong Kong’s pain was Singapore’s gain.

“A sharp rise in the number of family offices has been a huge boon to us,” says Joseph Poon, deputy global head of DBS’s private bank.

The number of local family offices quadrupled in the 24 months to the end of 2018 to 1,300, according to the Monetary Authority of Singapore, out of a global total of between 7,000 and 10,000. In recent months, new family offices have been set up in Singapore by the restaurateur Shu Ping, one of China’s richest women, and the British engineer James Dyson.

Pre-tax profit posted by DBS’s consumer banking and wealth management division rose 16% year on year in 2019, to S$2.78 billion ($2 billion), led by deposit and investment product income. At the end of 2019, DBS was the fifth-largest wealth manager in Asia ex-onshore China, with assets under management of S$245 billion.

Stability in this context can mean everything. DBS benefits not only from its own solidity – it is rated AA- by S&P and Fitch, and Aa1 by Moody’s – but also by the steadying hand of government and a business-friendly regulator.

Poon has enjoyed a ringside seat as personal fortunes created in China but stored beyond the reach of Beijing, transition from Hong Kong to Singapore.

“Most of it has been middle and lower-end wealth,” he says. “As of [the end of 2019], we had received 3,500 private banking applications, and opened over 3,000 of them, with the rest at the KYC [know-your-customer] stage. Everyone [in Hong Kong] is getting ready to move if they have to. We can be the offshore wealth management provider of choice for China.”

While China rightly catches the eye when the super-wealthy are mentioned, it’s worth noting that southeast Asia remains the source of so much of the fuel that drives private banking in Singapore.

“When a generational shift occurs, 80% of the money held by [high and ultra-high net-worth individuals] in the [Asean] region moves away from their parents’ bank,” says Poon. “We will be a major beneficiary of that.

“The next generation wants their money to be managed properly. They are more mobile, they want a better platform and they see that in us and in Singapore, with its rule of law and status as a global financial centre.

“Many regional entrepreneurs got wealthy while they were banking with us, and a lot of Asean people a carry a Singapore passport.”

Sustainability

If digital was DBS’s epic journey in the 2010s, what is its next great adventure?

“Sustainability is my epiphany,” Gupta says firmly. “That is my 2030. Last year, we did more than S$5 billion worth of sustainability-linked loans.”

Incentive schemes are being rolled out to encourage corporate clients to cut waste, eliminate energy inefficiencies and reduce environmental impact.

“When our clients hit sustainability targets, we reduce the rate of interest on their loans,” adds Gupta. “Take a five-year loan with X% interest rate at the start of the year. If a company hits 10 sustainability targets over the course of the year, we drop a pre-agreed percentage point off the loan’s rate. The leap of faith for any company is to believe that when it does something right from an ESG [environmental, social and governance] standpoint, its risk ratio will fall.”

He points to the work DBS does with a Singapore-based client Halcyon, one of the world’s leading rubber producers.

“We set up an exchange that allows them and us to track rubber from tree to mill, to ensure it is sustainable.”

Singapore, he believes, “can be a major global sustainability hub if we do it right. One of the biggest providers of carbon credits lies to the south of us in Indonesia, which has huge reserves of green and blue carbon.”

It won’t happen overnight – most Asian countries will be dependent on fossil fuels as their primary source of energy until the middle of the century.

|

|

|

Sim S Lim, DBS |

But the impact will be real and sustained, he warns; producers of thermal coal, which accounts for nearly 40% of the world’s electricity generation, are likely to face an “increasingly difficult [struggle] to find funding. We are stopping it, and if you look across the region, you find the number of big players willing to finance coal is falling in number every year.”

DBS could not have been in better shape. It posted net interest income of S$6.39 billion in the full year 2019, up 14% year on year, with net fee income up 10% over that period to S$3.05 billion. Fee income from wealth management rose 13%, trading income 24% and investment banking 66%.

At the end of February 2020, its market cap was a little under $60 billion. Excluding lenders from China and Japan, it is Asia’s third-largest bank by market capitalization and second largest, behind State Bank of India, in total assets. It took just 10 years for a solid but unspectacular Singapore lender to become a financial leader.

But the years ahead will test it in every conceivable way. Its chief executive, who joined in 2009 and who turned 60 in January 2020, will surely leave around the middle of the decade. Whoever takes up the baton will be responsible for one of the most coveted jobs in global banking: head of a trailblazing lender, in a super-safe city state, protected by its shareholding government, with satisfied customers across Asia.

The next CEO won’t have time to sit on his or her laurels. DBS will face growing pains, maybe in China as its debt-fuelled economic engine begins to wheeze, or in southeast Asia as the impact of climate change on low-lying land starts to bite. Perhaps protectionism will re-emerge in Asia and elsewhere.

The bank has been growing at a double-digit rate at home, but it cannot over-depend on the Lion City. In the full year 2019, Singapore generated 64% of net interest income and 72% of net profit.

“To rely on Singapore is not sustainable,” says Gupta. “Our business needs to grow outside – China, Indonesia and India will help that.”

DBS is not the only bank that sees its future in Asia. Lenders from Malaysia (notably Maybank) and Thailand (Bangkok Bank), as well as Taiwan, the Philippines, South Korea and India are stretching their legs.

So too are local rivals UOB and OCBC. The latter, with its Jakarta-listed subsidiary, OCBC Nisp, and its 100-plus branches in Hong Kong, Macau and mainland China, under the umbrella of OCBC Wing Hang, is described by one analyst as “DBS’s biggest long-term regional rival”.

In my lifetime, or just outside, Asia’s premier financial centre will be Shanghai – Sim S Lim, DBS

China presents a different sort of two-sided challenge. On the one hand, it is an important source of current and future income, although DBS’s progress in Asia’s largest economy is erratic.

Earnings generated in mainland China and Macau quadrupled year on year in 2018, when it accounted for S$275 million of bank-wide net profit, but fell back in 2019 to S$210 million.

Hong Kong added S$1.43 billion to the earnings pot in 2019, marking a tripling of profits in less than 10 years – although a sizeable amount of that comes from DBS’s business with mainland firms and individuals.

As long as China doesn’t suffer a meltdown, in the face of rising debt or the coronavirus, its business there will continue to grow.

Yet China is also an enigma: no one is sure what the 2020s will bring. Its banks could emerge as regional and even global leaders by the end of the decade. Or, if another crisis hits, Beijing, rather than easing open its capital account, might slam the door shut.

It is possible to imagine Hong Kongers taking to the streets again to rage in protest about people-power and income inequality. Would that lead China to aggressively push Shanghai as its offshore financial centre of choice?

Such an event would harm Hong Kong, as listings migrate north and foreigners invest directly in Chinese assets and securities. More mainlanders might feel compelled to store wealth closer to home, hitting DBS and by extension Singapore. Yet the bank is confident.

“In my lifetime, or just outside, Asia’s premier financial centre will be Shanghai,” says DBS’s group head of consumer banking and wealth management, Sim S Lim.

Sweet spot

For now, the future looks rosy for DBS. It isn’t able to compete on an equal footing with the world’s universal lenders – perhaps it never will. But that shouldn’t matter. Its calling cards, beyond its digital excellence, are its solidity and geography.

It is, in the words of Tan: “Through and through an Asian bank with the best aspects of Asia. We have long-term relationships with our clients, who we stick with through good times and bad.”

DBS is in a sweet spot. Western banks remain in broad retreat. China’s lenders aren’t ready for the big time yet, while those from Japan, Korea and India focus on domestic clients.

For now, only DBS is outward-looking and ambitious enough to want to grasp the mantle of ‘Asia’s bank’.

“Pan-Asia, we want to be a number-two or number-three player in each [operating] market,” says Lim. “That is why we are investing in India and greater China. Asean is our backyard and Indonesia will be a top-10 economy in 20 years’ time. We want to be Asia’s number-one bank.”

It’s a bold statement of intent – and one that is perhaps ultimately unachievable. History offers no evidence of any bank successfully sustaining a high level of profitability and a top-three position in multiple markets across an entire region, let alone one as complex and diverse as Asia.

DBS could adopt an expansion-by-acquisition approach in the pursuit of regional dominance, but doing so would require unprecedented capital raising and put the bank’s reputation for safety-at-all-costs under threat.

There’s the organic route of course. Here, Gupta and his team believe DBS’s digital leadership and its willingness to adapt its award-winning platform to new markets can be the key to success.

But in most Asian markets there are typically at least three – and often more – well-run, digital-savvy banks.

It is difficult to imagine a foreign bank breaking into Singapore’s market and going toe to toe with the triumvirate of DBS, UOB and OCBC. So why should it be different for DBS in super-competitive markets such as India, China, Indonesia or Thailand?

Grand plans like these often end up with the bank in question performing well in some markets and poorly in others. If DBS can square that circle, build a sustainably profitable pan-Asian banking business and become a leader in multiple jurisdictions, it will be perhaps its greatest achievement of all.