“The [wealth management] industry has made many runs at engaging with women, and has failed,” says Sallie Krawcheck. She is talking to Euromoney in the Manhattan offices of Ellevest, the women-targeted robo-advisory firm she founded in 2014.

We are in the ‘Gloria’ room (named after Gloria Steinem). There are other glass-walled rooms: ‘Alice’ (Walker) and ‘Michelle’ (Obama). In one of them, a dozen women can be seen discussing investment strategy. In most other US and even European advisory firms, the assumption might be that it was a marketing meeting – after all, only some 15% to 20% of client advisers in the US are female.

|

|

Sallie Krawcheck, Ellevest |

As a veteran of the wealth management industry Krawcheck knows this only too well. She became the chief executive of brokerage Smith Barney (back when it was owned by Citigroup and not Morgan Stanley) and then oversaw Citi’s wealth management business, before running global wealth and investment management at Bank of America Merrill Lynch.

She didn’t leave either bank amicably due to clashes in management style, in part because of gender differences, she says. Male-dominated environments often tend to competition and profit maximizing, she points out. Female-dominated environments, on the other hand, tend to be relationship-focused.

Krawcheck knows this comment can be seen as a generalization, but it is not without substance. Women think differently to men when it comes to running businesses and finances, chiefly because their experiences from a young age differ to those of men. It is what many wealth management chief executives have yet to grasp and that’s why she started Ellevest, she says.

If the Gloria and Alice rooms sound gimmicky, they don’t feel it. Indeed they are refreshingly different, to the point of being somewhat surreal. It is easy to forget the norm in private banking is some combination of heavy doors, dark wood, leather seats, a copy of the Wall Street Journal on a glass table and art depicting railroads, skyscrapers or ships that together offer a reminder that wealth has been a man’s world for quite some time. While other industries began thinking about inclusive design back in the 1980s, following work of pioneers like Patricia Moore, the financial industry did not.

|

|

| Ellevest offices: Private banking for women begins with the design of the office |

Ellevest, in contrast, feels like entering any firm established in the 21st century – white, bright, clean and open. But all this is just preparation for the real comfort here: knowing that the advice you will get as a woman is going to be relevant to you. The team at Ellevest already knows that as a woman you likely earn only 81 cents for every dollar your male counterpart earns – and less if you are African American or Latina.

They know that the compound effect of that lower salary, combined with time away from your job caring for children or family, a longer life expectancy and a more conservative investment outlook will mean you are far less likely than a man to be able to support yourself in retirement.

They know your salary peaks in your 40s – for men it is their 50s – so that you have to save early and hard. They know that you will likely care less about outperforming benchmarks and more about meeting your financial goals than your husband, brother or father, and that you also probably want your investments to have a positive impact on the environment and society.

Goldman Sachs, Merrill Lynch (with its iconic bull mascot), Morgan Stanley – those are masculine brands – Sallie Krawcheck, Ellevest

They also know that while your financial acumen maybe the same as your male counterpart’s, your confidence is far lower – women are 44% less likely than men to describe themselves as financially knowledgeable. And finally, they know that you have very little free time, which means the products and strategies they offer are those you want, so no one’s time is wasted.

So, why is Ellevest the sole female-only focused advisory? Why are we, in 2019, still orienting investment services predominantly towards men? Indeed, why has the wealth management industry “failed” women, as Krawcheck suggests?

She answers: “Because it has spent more time talking on panels and marketing its existing approach to women rather than saying: ‘You are as you are, it’s us that needs to change.’”

Wealth transfer

Krawcheck has a head start on serving women – and $200 million in assets under management to prove it, but an industry-wide change is coming and she knows her competition over the next decade will increase.

Its driver will not be movements like #MeToo – we have seen many iterations of women’s movements over the last 40 years that have failed to move the needle in financial services. Rather it is going to happen because the fundamentals dictate it. Women will be the majority beneficiaries of the $30 trillion intergenerational wealth transfer that is due to occur within the next 25 years in the US alone – either as women outlive their husbands or as daughters inherit from their baby boomer parents.

Exactly how much of that $30 trillion they will receive is unknowable, but those pushing for change often cite a study from 2009 that says 70%.

Add to this the fact that women are already the majority of the population, that they already control some $11 trillion in assets in the US alone, are the majority earners of graduate, masters and doctorate degrees and that they own 40% of US businesses (opening 1,821 net new ones a day), and it is clear that millions of women make a big market in need of investment advice. And even if they are not seeking it out, it is in the interest of the wealth management industry to find a way to get those dollars out of cash and into some fee-generating investments.

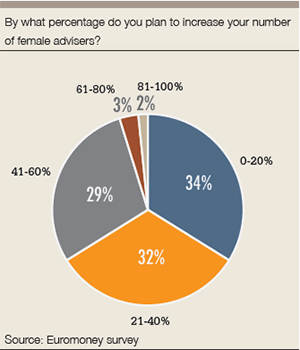

An investment industry inclusive of, or directed at, women is inevitable. Indeed 73% of 1,330 private banking industry participants surveyed by Euromoney at the end of last year say their firms have plans in 2019 to respond to the anticipated growth in female-owned wealth. What those plans are, however, should be the focus for the next decade.

|

|

Of those respondents that do have plans, the most popular response was ‘targeted marketing’ and ‘hiring female advisers’. But ‘creating different products and services’, as well as ‘internal training regarding the different needs of women’ scored lowest respectively.

These results offer some cause for concern.

There is an opportunity here, born of this confluence of wealth transfer and increased public attention on inclusion, that people like Krawcheck, who have fought hard for women to be noticed as financial clients, can see. If the investment industry develops along appropriate lines – understanding women’s relationship to money, offering the advice needed, and developing confidence around investing and growing their businesses – then the social impact will be important.

But if wealth managers do not think about changing everything from design and language to portfolio models, but rather resort to only marketing, then women won’t grow the wealth they inherit or create, the playing field will not be levelled and the list of the world’s wealthiest and most powerful individuals will be continue to be made up almost entirely of men.

There was some striking research by UBS in October 2017 that exemplifies the importance of good advice for women. Taking a fictional Joe and Jane, who each inherit $1 million at age 24 and earn $110,000 at age 25, pay gaps, career breaks, longer life expectancy and risk aversion could result in Jane having no investable assets at age 70, while Joe would be expected to have $5 million.

Thinking beyond marketing also makes sense for wealth managers. As Krawcheck points out, a rebrand towards women is going to be unconvincing at some of the typical brokerage or investment banking houses.

“Goldman Sachs, Merrill Lynch (with its iconic bull mascot), Morgan Stanley – those are masculine brands,” she says.

Changes

If wealth managers are sincere in their pronouncements that they want to help women create, grow and preserve wealth, what must they change?

Jackie VanderBrug runs impact investing at Bank of America Merrill Lynch. She is regarded as the mother of gender lens investing and has conducted years of research into women and their finances. She says the wealth industry by now should be well into the third phase of addressing women and wealth.

|

|

|

Jackie VanderBrug, |

“The industry started with offering networking events for female clients and seminars, then they collected data on what female clients want,” she says. “Now, we need to be letting that data inform our strategies when it comes to serving women.”

In reality, many wealth managers find themselves still in phase one or two, but it is in this third phase (where Krawcheck firmly sits) that real systemic change begins. Efforts are afoot at some of the large wealth managers, although it is too early to see any difference in behaviour as a result of such efforts.

BNP Paribas Wealth Management – one of the few banks with a female head overseeing the global business line – has made several changes to how it works with female clients based on data that it is putting to work to help women.

“Our research shows us that women entrepreneurs don’t use a lot of credit and tend not to IPO their companies. Rather they rely on self-financing,” says Sofia Merlo, co-head of BNP Paribas Wealth Management. “We have taken action to ensure that our female clients understand that bank finance or going public is a way to grow their business faster.”

The bank worked with Stanford University to run a programme for 150 women clients on the topic. She also says that relationship managers have been trained to know gender differences around financing.

UBS has also made some changes to how it serves women based on research it has carried out among female clients. It launched its programme in 2017 to develop more research around female entrepreneurs and women’s relationships to wealth, and focus the firm on the topics.

Eva Lindholm is head of UBS’s UK and Jersey wealth management business. She says that one client mentioned that despite being an astute business leader, she found financial jargon off-putting in advisory meetings. Another said that she would feel more comfortable discussing money at her home or in an environment that wasn’t an office. A third female client questioned why, given she had autonomy to choose her children’s nannies, her stylist, her dentist and so on, was she being “given” an adviser by the bank?

Diverse companies perform better, and having more women in wealth management will also generate different ideas that will help them serve women better – Jackie VanderBrug, BAML

Born out of this last conversation, UBS experimented in one female-focused campaign in the UK with having adviser bios online that included personal information such as hobbies and values, as well as professional expertise. Clients could browse through advisers to find their match.

The response from female clients was positive, although the bank never felt comfortable adopting a model that could be compared to a dating site. Lindholm says what the experience showed, however, is that it is clear that a connection is important for women when choosing their adviser and the industry will need to figure out how to respond to that preference. For example, UBS now offers clients a choice of relationship managers – and not just to its female clients.

Krawcheck says the monitoring of what women want should be continuous.

“We have found lots and lots of things that women have wanted and they are reflected in our products. It’s everything from big things (goals-based investing, rather than investing to beat the market) to more subtle usability issues on the website in terms of what order we present things to them.”

Female advisers

As Euromoney’s survey suggests, the usual assumption when thinking about connection is that female clients prefer female advisers. It makes for a simple solution to serving wealthy women – hire more women. But opinion is split on the validity of this assumption.

|

|

Krawcheck says: while “women will say they don’t mind which gender serves them, the majority will choose a woman when it comes down to it.”

More than 80% of her advisers are female.

Merlo, however disagrees.

“It’s easy to think that women want a female adviser,” she says, “but we each have had personal experiences that inform our decisions. I see female clients who prefer to have a male adviser and I see women who don’t have a preference at all. It’s about finding the right adviser.”

She says BNP Paribas has at least two people of both genders working with a client.

VanderBrug says it is really that women want someone who is gender smart and it is this that has been missing.

“Women above all want advisers who are going to give them the advice that is right for them – who know about their potential pay gaps and earnings life cycles for example, or who understand they may lack confidence or have certain investment preferences, like impact investing,” she says.

Do they also enjoy having an adviser with similar shared life experiences? Yes, she says, but it’s not as gender-specific as we perhaps think it to be. And of course, it is not a given that a female adviser knows the investment challenges of her gender. Training is necessary for all advisers.

|

|

Carolanne Minashi, UBS |

Carolanne Minashi, global head of diversity, at UBS agrees: “The aim is to bank women in a smarter and more gender-intelligent way, and that is not about female advisers and pink credit cards. It’s a business imperative to push ourselves to equip all our advisers with what they need to serve women better.”

Regardless of whether or not women prefer female advisers, the industry needs a far more diverse workforce than it has.

It is just obvious, says VanderBrug: “Diverse companies perform better, and having more women in wealth management will also generate different ideas that will help them serve women better.”

It is that old adage: You can’t see what you don’t know.

It is hard to imagine a firm that is so considered in its approach to women such as Ellevest being created by a male-only team, for instance.

It seems that part of the reason why the wealth management industry has not attracted women is because it has not tried to do so.

As Minashi says of UBS’s strategy, it is quite simple: hire more women, promote more women and seek to retain more women. She also makes the salient point that as hiring of female advisers ticks up, it will be essential not to simply poach from competitors.

“The available pool of female wealth managers is limited at present,” she says. “Yes, we want to be an employer of choice, but if we revert to poaching then we aren’t expanding that talent pool as an industry.”

|

|

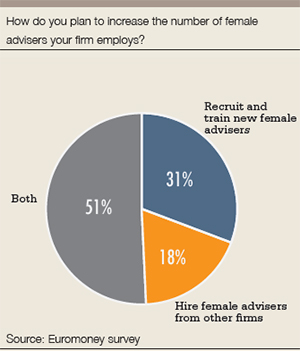

Of the Euromoney survey respondents who say their firms plan to increase the number of female advisers, 19% say they plan to hire them from competitors. Just over half say they would be both hiring from outside firms as well as tapping new and internal employees for training.

Several banks – UBS among them – have career comeback programmes, bringing women into the wealth advisory business who have had long career breaks, as a means to expand that pool. UBS is also engaging school leavers in an apprenticeship programme.

Bank of America has begun hosting career nights, advertising on LinkedIn and other social media sites to source potential female candidates nationally. Female advisers at Merrill Lynch share their experiences at the online events and introduce the role to women who may not have otherwise considered wealth management.

Kirstin Hill, managing director and strategic performance executive at Merrill Lynch Wealth Management, says attracting female advisers in part requires simply educating women about the role.

“In addition to many of the benefits we offer, like 16 weeks of paid parental leave, childcare reimbursement programmes and back-up care programmes, being an adviser is a very attractive position for women,” says Hill. “There’s flexibility and the possibility of controlling your own hours, but it also gives you the opportunity to help other women and individuals achieve their life goals and to weather the hard times. The industry needs to be better at articulating these aspects of the job.” Merrill Lynch has been trying to build a pipeline. Some 27% of the trainees it hired in 2018 were women.

But retention and progression also play a role. All firms interviewed mentioned how they track progression of women up through the firm, which is more than they did 10 years ago. But the stats are still shockingly low when it comes to the total number of female advisers. UBS and Citi did not disclose their female financial adviser headcount numbers for this article – leaving one to assume they are low. At Merrill Lynch, it’s between 16% and 19%.

Is it a coincidence that firms with female heads – US Trust, JPMorgan, BNP Paribas – have higher numbers of female advisers than their peers? Or perhaps it is that those with more female advisers end up with more female heads of businesses? At BNP Paribas, Merlo says 42% of its relationship managers are female; at US Trust it is 30%, at JP Morgan it’s between 30% and 40%, the lower being advisors, the higher being client-facing employees.

Instilling confidence

Adapting products and services, hiring and training gender-smart advisers, improving internal diversity and career progression for women – these are all things the wealth management industry needs to be doing in the coming years to help women better manage their money. But it will be an evolving field for wealth managers. It took decades for them to understand how to manage money for men; women are an entirely new focus.

|

| A female customer in a man’s world. Picture courtesy of Merrill Lynch (1966) |

Expanding on VanderBrug’s phases, where phase two is collecting data and phase three is taking action based on data, then phase four will need to be ‘continued measuring of the impacts of all actions taken’. Are more women starting and growing businesses? Are women feeling more confident with their finances? Are women invested?

This line of questioning is crucial, because even with the last five years of beginning to address female investors, survey results are showing women’s confidence is still low. Around 61% of millennial females leave big financial decisions to their spouses.

“This is not a quick fix,” points out Krawcheck. “Women develop a lack of confidence around finance as children. Our culture and system has to change.”

She points to research that shows parents speak differently to sons and daughters about money.

Instilling confidence through financial education is one area in which the banks interviewed are engaged. UBS has a financial confidence initiative that invites women to better understand their own relationship to wealth and offers educational blogs. JPMorgan Chase sponsors a morning vlog called ChedHER on media site Cheddar, where female hosts interview women about finance to accompany its ‘Women on the move’ programme.

Merrill Lynch is hosting a 10-city event series for women, including topics on finance and health, and educating children about finances.

“We’ve got to start breaking open a dialogue,” says Hill. “Progression is just too slow. It’s not right that more women would rather speak about death than money.”

The aim is to bank women in a smarter and more gender-intelligent way, and that is not about female advisers and pink credit cards – Carolanne Minashi, UBS

Will these efforts by banks help? What messaging will best reach women and inspire action? Again, it is up to the industry to keep measuring the data and impact.

Krawcheck has her own method of educating women. She posts unproduced one-minute videos answering questions from women about the markets or what they should do with their raise. Why?

“Because women have questions and we want to answer them,” says Krawcheck.

She also posts video advice from her desk, couch or even running in Central Park. The clips are short, casual, informative, devoid of jargon and always point to an immediate action that can be taken. While you may be one of thousands of Ellevest’s clients online, it feels like Krawcheck is your personal adviser and mentor.

It may not be the model for all women – and perhaps not for those at the higher end of the wealth spectrum, or those who want their money managed alongside their male partners – but it is the closest the wealth management industry has right now to a model to work from when it comes to serving women.

This unpolished constant reminder from Krawcheck to women to think about their finances, while they watch a woman talk about investments, has more power than many will understand – it normalizes that conversation and that is exactly what the industry will need to do if it is to shift to a new normal.