Although the most recent indicators suggest Asia credit should hold steady for the next quarter or so, the prospect of Fed tapering in March, relatively high levels of leverage, a reduction in bank funding and lower capex suggest a more challenging long-term outlook for leading markets such as China, Korea and Indonesia.

Against this deteriorating backdrop, Asia Pacific (ex-Japan) corporate credit default risk is rising after 18 months of plain sailing, according to Moody’s Investors Service in Hong Kong. The agency says the trailing 12-month default rate for Asia high-yield corporates, which has been stuck at zero for the past six quarters, is started to rise as the tough operating environment begins to feed into financial performance, with steel and mining companies bearing the brunt of the downturn.

Asian high-yield defaults increased to 1.25% in October after Chinese coal miner Winsway’s $460 million distressed bond exchange for 8% senior notes due 2016, the first corporate default in Asia since the first quarter 2012.

Moody’s says the high-yield default rate could increase to as much as 1.9% before the end of the year if Indonesian mining company Bumi Resources closes its own $1.3 billion distressed restructuring deal with China Investment Corporation before the end of the year.

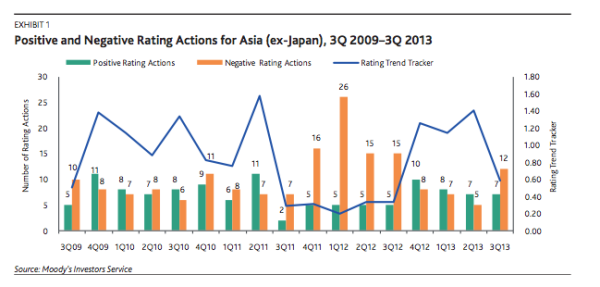

Indeed, Chinese, Mongolian, Korean and Indonesian mining and steel companies accounted for nearly half of the total negative ratings actions in the third quarter, as falling commodity prices have impacted profitability and reduced companies’ ability to meet their financial commitments.

|

For instance, seaborne thermal coal prices have declined more than 15% during 2013 as lower-cost producers have ramped up supply. This trend is likely to remain in place throughout 2014 as supply continues to exceed demand.

Meanwhile, steel demand is falling, given China’s reduced infrastructure investment. “The oversupply situation in the steel industry, owing to China’s record-high production levels and the destocking by steelmakers in the second half of 2013, has further aggravated the pressure on the sector as a whole,” says Moody’s. “Korean steel companies in particular are facing weak domestic and regional demand.”

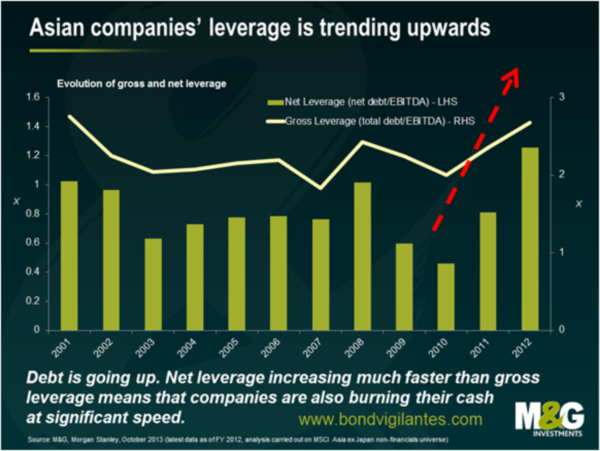

Increased pressure on Asia’s corporate balance sheets means less money will be available for capex, and a greater dependency on domestic bank lending and bond market investors for funding. Already, many Asian borrowers have lengthened maturity profiles and pre-financed 2014 funding needs in preparation for tighter lending conditions, as banks scale back lending activities in the face of rising leverage among Asian companies. Similarly, the region’s largest companies have started to cut back on capex.

|

| Source: Bond Vigilantes |

While such longer-term factors imply a more challenging future, and retail investors continue to withdraw money from emerging-market bond funds, both investment-grade and high-yield credit spreads have tightened since September, suggesting a return of institutional risk appetite for Asia credit.

Supported by reduced US interest-rate volatility and better-than-expected economic data from China, Asian spreads have narrowed by more than 50 basis points, according to market sources.

“With only two months left in 2013, we expect market volatility to ease, if somewhat erratically, as participants start positioning portfolios for next year,” says one credit market specialist. “Portfolio churning and the still-heavy primary pipeline should limit further general credit-spread compression as year-end approaches.”

Moreover, Asian investment-grade and high-yield credit looks relatively attractive on a relative-value basis when compared with its US counterpart, given relatively lower liquidity, poorer transparency and a more volatile macro-economic environment.

“The average spread differential per rating notch is 10bp to 15bp for single-A-and-above credits, and 30bp to 40bp for BBB credits,” the source says. “The differential is wider in the HY space, at 50bp to 60bp. Asia ex-Japan high-grade credits offer value over US credits in the AA and A rating buckets, but not in the BBB bucket. However, high-yield credits offer value across all rating categories.”

With most observers expecting Asian bond issuance to continue to grow into 2014 and 2015 as institutional investors grow their allocations to what they perceive as a core asset class, the health of the region’s corporate balance sheet and the willingness of local banks to extend funding, especially in China, are nonetheless growing in global significance.