Jón Gunnar Jónsson is looking more relaxed than might be expected. As the director general of Bankasýsla ríkisins, better known internationally as Icelandic State Financial Investments (ISFI), he must be wondering how much longer the organization he runs will even exist.

The latest privatization deal that the Icelandic government completed – a March 2022 accelerated bookbuild of shares in Íslandsbanki, the country’s second biggest bank by assets – sparked a public and political outcry that has now seen investigations opened by the country’s central bank and the National Audit Office.

Of more immediate concern to Jón Gunnar himself is the extraordinary response by Iceland’s government to the furore: a proposal to shut down ISFI altogether, announced on April 19.

The affair has dominated Icelandic politics for weeks; there have even been protests on the streets. At the time of writing, it was dominating municipal elections scheduled for May 14. Privatizations, it seems, are the gift that keeps on giving.

Jón Gunnar has been running ISFI since 2012, some three years after the body was set up to manage the banks that Iceland had to nationalize when its economy collapsed during the great financial crisis of 2008.

One of those, Kaupthing, was re-privatized as Arion Banki in 2018. Íslandsbanki, the former Glitnir, was floated in June 2021. Landsbankinn, the biggest of the three and reconstituted from the ashes of Landsbanki, is still state-owned. And with all that has happened in recent weeks, bringing it back to the public market looks a very distant prospect indeed.

But more of that later. Euromoney is on a Teams call with Jón Gunnar to talk first about Íslandsbanki’s IPO – Iceland’s biggest ever. If it is to be Jón Gunnar’s last IPO at ISFI, it is a good one to go out on.

Pandemic casualty

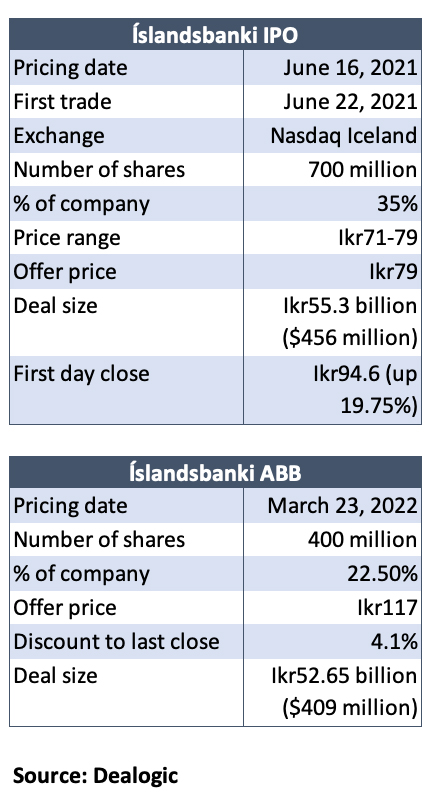

A deal like this – at IKr55.3 billion ($456 million), it was bigger even than the IKr33.9 billion IPO of Arion Banki – was always going to present serious challenges. But the pandemic added a few more for good measure.

It was on March 4, 2020, that ISFI submitted its proposal for the sale of at least one-fifth of the bank to the ministry of finance. That plan lasted precisely two weeks. On March 18 it was scrapped, an early casualty of uncertainty as coronavirus began to sweep its way from Asia across the world.

But the plan didn’t stay dormant for long. By December 2020, with the government borrowing to keep the country’s economy afloat, it was back on the agenda.

The tourism industry, which collapsed in the pandemic, accounted for fully one third of the country’s GDP in 2019. It was effectively put into hibernation thanks to government support, but the cost of doing so was mounting.

One of the brave things we did was decide on a single listing for Íslandsbanki

Jón Gunnar Jónsson, ISFI

“At the end of the day the government was running a deficit and could not borrow for ever, and so was increasingly looking to asset sales,” says Jón Gunnar. “Iceland was also coping with the pandemic better than had been expected, markets were strong domestically and the European banking sector was also doing reasonably well.”

So the government pressed ahead. ISFI submitted its proposal for the privatization in mid December 2020, and the finance ministry approved it in late January 2021.

Next up was the appointment of legal counsel – a protracted process that required ticking the boxes of Iceland’s government procurement laws and using the services of the country’s National Procurement Office.

Law firm White & Case was eventually picked as counsel to both ISFI and Íslandsbanki, and started work in March.

In the meantime, financial advisers and underwriters had been brought on board – a slightly quicker process given that hiring them is exempt from Iceland’s procurement laws, although ISFI still used the National Procurement Office to manage the process.

Two dozen banks had made submissions. For its financial adviser, ISFI chose London-based STJ Advisors, the independent firm set up by former ECM banker John St John in 2008 that has since carved out a role for itself in equity transactions by helping issuers evaluate banks to lead and syndicate deals. Íslandsbanki, meanwhile, went with ABN Amro.

For Jón Gunnar, the choice of STJ Advisors was a reflection of the scale of the task and the fact that it was bigger than anything that had been attempted in Iceland before – the stakes were high, and independent advice in selecting the global investment banks that would be needed to pull in international accounts would be invaluable.

From the international candidates, Citi and JPMorgan were chosen to lead the deal as joint global coordinators. They were joined by Barclays and HSBC as bookrunners – less obvious choices perhaps, given their smaller IPO franchises, but who Jón Gunnar says were picked for specific reasons.

“Barclays had been quite active with Icelandic banks in debt capital markets, and we had been covered by their ECM bankers for 10 years – they had certainly demonstrated their interest in being there,” he says. “And Iceland at the time was becoming a member of frontier market indices at MSCI and FTSE Russell, and so we liked HSBC’s coverage of those kinds of investors.”

Bookrunners among the domestic banks were Íslandsbanki itself, Fossar Markets and Landsbankinn.

ABN Amro, meanwhile, might have looked at first glance a curious choice for adviser to Íslandsbanki, but ISFI is a similar animal to NL Financial Investments, the Dutch state holding company, and ABN’s experience with deals there was seen as a useful precedent.

Float format

Next up was a decision on the format of the float. When Arion Banki listed in 2018, it did so with a dual listing of Swedish depository receipts (SDRs) in Stockholm – the first dual listing from Iceland.

Only one other company has since done something similar, food processing services company Marel, which included a secondary listing in Amsterdam when it came to market in 2019 in a deal that STJ Advisors also worked on.

This time around, though, ISFI was keen to put all the emphasis on Iceland.

“One of the brave things we did was decide on a single listing for Íslandsbanki,” says Jón Gunnar. “One of our objectives enshrined in law is to work towards strengthening the domestic capital market, and the second reason was that in fact there is very little liquidity in those secondary listings.”

For a deal where the intention was to attract foreign investors, sticking exclusively to an Iceland listing was a risky option. So, the first job of the underwriters was to survey international accounts to see if they would even be willing to buy local stock.

“A lot of preparation went into that,” says Jón Gunnar. “We had to look at the settlement infrastructure and foreign exchange issues.”

At least one thing was simple: identifying a comparable. While different at a granular level – Íslandsbanki is more focused on Reykjavík than Landsbankinn is, for instance – the three Icelandic banks are broadly identical in size and in the segments in which they compete.

Arion Banki, having already listed, was the yardstick. It was arguably further along the route of capital optimization than Íslandsbanki and had worked to refine its business model, and so was expected to post a return on equity for the year of about 11%. Íslandsbanki had trended closer to 8%.

Jón Gunnar found himself digging out the classic regression line graph beloved of analysts, plotting various banks’ RoE on the x-axis against price-to-book on the y-axis. Below the line and you are undervalued, goes the theory.

“We felt that if we excluded the IPO discount, we should be on the line,” says Jón Gunnar. “Early indications were that investors would be willing to come in at 0.7 times price-to-book and upwards, tailing off at around 0.8 times.”

Happily for Jón Gunnar, that was pretty much on target.

Management

IPOs are tough to manage in good times. In a pandemic they might look tougher still – but not necessarily so. With the vast array of early looks, pilot fishing, analyst presentations and roadshows conducted through Zoom, Teams and the like, there was a lot of tech to navigate.

Jón Gunnar had taken heart from precedents. After all, Norwegian video-conferencing company Pexip had managed to float in May 2020 by using its own systems to sell its story to investors. Others had followed it, with issuers, bankers and investors all adapting to the new normal of roadshow via webcam.

Íslandsbanki would be no exception. Euromoney’s eyes widen when Jón Gunnar reveals that the very first simultaneous physical meeting of lawyers, advisers, selling shareholder and Íslandsbanki itself did not happen until the very day of pricing.

“We started in February and priced in June,” he says. “And one reason we could do that was because it was all virtual.”

The IPO was 0.86 times price-to-book – right on the regression line!

Jón Gunnar Jónsson

Investors were unfazed, piling into the deal to leave it nine times covered through the price range of IKr71 to IKr79, allowing pricing at the very top.

“That was 0.86 times price-to-book,” says Jón Gunnar – before adding, with some pleasure, “right on the regression line!”

A fully exercised overallotment option would take the final deal size to practically 700 million shares, some 35% of the bank.

Key to the result, Jón Gunnar argues now, was the strategy of creating pricing tension between domestic and international buyers. Iceland’s pension funds wield tremendous power – they hold about 40% of the country’s shares, Jón Gunnar estimates, and three alone hold about 60% of pension assets.

“That means they obviously tend to drive the price, so we wanted to create competition between the international and the domestic sides to demonstrate that the pension funds would not be the sole determiners of the price,” he says.

That works both ways, though.

International investors also needed to know that there was a commitment to serve the domestic buyer base so they also couldn’t railroad the process. Opting to sign up cornerstone investors from both camps was one way to do that.

Capital Group and RWC Partners – since rebranded as RedWheel – were pre-announced with 12% and 4.8% of the deal, respectively, while domestic pension funds Gildi and LV took 7.3% each, tying up more than 30% of the deal from the get-go.

The momentum gathered. A books-covered message went out at the end of the first day of subscriptions. Managing the retail demand would end up being a headache, not least because the finance ministry had decided to promise full allocations for anyone subscribing to up to one million shares. With the cornerstones already on board, it didn’t leave much for the rest.

Retail had been helped by being able to subscribe to the deal through an app developed by Íslandsbanki – another first for the country. They ended up with 30% of the deal, a highly unusual outcome and perhaps double the more typical level. International institutions got 30% and domestics 40%.

“The bank floated with 24,000 shareholders, more than any other listed company in Iceland,” says Jón Gunnar.

First-day fizz

However much work bankers think they have done in just getting a company to market, they know it can all be undone by a bad first day of trading. It was quickly obvious that they would not face that problem with Íslandsbanki.

The stock closed about 20% up from offer price on its first day; Arion Banki rose about 18% on its first day. But since then, the stocks have diverged a little. Íslandsbanki is up about 26% from its first day’s close. Arion Banki is up about 11% over the same period.

Was 20% on the cusp of being a little too frothy for day one? After all, it’s a fine line between ensuring some aftermarket juice and having to field accusations of under-pricing.

Jón Gunnar was more than happy with the outcome.

“It didn’t raise any eyebrows because there was such strong retail participation, so no one got any sense that the stock had been placed with friends and family at too low a price,” he says. “But it was slightly above expectations, I would say.”

But in any case, ISFI had to think from the perspective of a majority owner of the bank.

“When you are a holder of 65% of the stock, the last thing you want is a collapse in the price,” Jón Gunnar explains. “You can push the pricing, but that would be for short-term gain at huge long-term expense.”

Not only that, but privatizations are also political. Support for them is practically impossible unless you can sell at a higher price each time.

And so, when ISFI came back to market in March 2022 to sell another slug, after the expiry of its lock-up in December, the omens looked good. The stock was well up from the IPO, meaning that a deal of almost the same value could be possible even from selling a smaller stake – useful, given that a deal of any meaningful size was always going to be something of a liquidity event.

The deal was conducted as an overnight accelerated bookbuild for qualified investors across March 22/23. Upsized from 400 million to 450 million shares after being covered multiple times, it totalled 22.5% of the bank and pulled in proceeds of IKr52.65 billion.

It priced at IKr117, a 4.1% discount to the previous close, and traded up after execution – and is still up now, at around IKr124.

“We sold more than 300 days of volume in Íslandsbanki,” says Jón Gunnar. “Compare that to the first follow-on of Arion Banki in 2019, which was 150 days’ volume at an 8% discount.”

There were hedge funds in the book, but investor support from the best long names was also strong. One thing Jón Gunnar particularly likes is how Capital Group – which has been a high-profile seller of European bank stocks of late – took the opportunity to increase its stake.

ISFI is now locked up for another 90 days, expiring on June 21, although true ECM junkies might be interested by the fact that ISFI negotiated an exemption in the underwriting agreement that would allow it to sell into Íslandsbanki’s buyback programme if it chose to, something that is fairly unusual.

Looking at the two Íslandsbanki deals side by side, Jón Gunnar now judges the March sale as even more successful than the IPO.

But in Iceland right now, his is a lonely voice.

The ministry list

April 6 was a day of drama, when Iceland’s finance ministry published a complete list of the 209 investors in the accelerated bookbuild alongside a detailed description of the deal. That was unexpected, especially at ISFI, which had advised against it.

“Yes, I was surprised that they published it,” says Jón Gunnar now. “We objected to publication based on confidentiality provisions in the laws on financial undertakings in Iceland, but given the fact that we are under the ministry of finance we had to provide it to them.

“The ministry decided to publish it against our recommendation, even though we told them there was absolutely no precedent for publishing such a list in Iceland or by European governments.”

In its statement the ministry said that it had decided to publish the list after determining that the information was not covered by banking secrecy rules and was in the interests of transparency.

The Icelandic media was quick to highlight that one of the buyers was a company owned by Benedikt Sveinsson, the father of finance minister Bjarni Benediktsson. In a radio interview on April 7, Bjarni argued that he had had no idea that his father had participated.

Iceland’s bank privatizations fall under the purview of the finance minister and are governed by legislation, chiefly the ‘Act 155/2012 on the sale process of the state’s holdings in financial undertakings’, which came into effect on January 3, 2013.

According to an official translation of the act, Article 4 stipulates that once ISFI has delivered its assessment of offers for a holding, “the minister decides whether an offer is accepted or rejected and signs agreements on behalf of the state regarding the sale of a holding”.

The finance ministry has said that it has asked the National Audit Office to assess whether or not the sale had complied with law and best practice.

On April 19 there was more to come from the government, with a statement released after a meeting of the governing parties in which it said that the sale did not fully meet the government’s expectations on transparency and disclosure of information. The government also noted that the central bank’s Financial Supervision Authority had begun its own investigation into aspects of the sale.

The sale process has been criticised in both the public and political space in Iceland

Íslandsbanki earnings report

And then the killer blow for ISFI: confirmation that the government would propose to parliament that the body be abolished, and a new arrangement found to manage state holdings in the banks.

But the statement also noted how the country had profited from privatization, arguing that income from state holdings and their sale had been used for the benefit of the public.

As for Íslandsbanki itself, it noted in its first-quarter earnings report on May 5 that: “The sale process has been criticised in both the public and political space in Iceland. As a result, the process will be investigated by both the Central Bank and the Icelandic National Audit Office and further steps in the government sell-down will not take place until their findings are in place.”

As is the nature of these things, in the public outcry multiple complaints are being jumbled together in a cacophony of anger and confusion. Why was the stock sold at a discount when the deal was oversubscribed? Why weren’t retail investors able to participate? Why were “speculators” allocated shares, only to sell them? Why did a firm owned by the finance minister’s father buy shares?

Discounted pricing and the lack of retail are perhaps the simplest to tackle. This is how accelerated bookbuilds are executed.

Íslandsbanki CEO Birna Einarsdóttir said when presenting the bank’s first-quarter earnings that the ensuing debate was probably down to a lack of familiarity in Iceland with the method.

Jón Gunnar, who seems bemused by the backlash on the sales process, agrees. But he also concedes that “in hindsight, perhaps we and the government could have done a better job in terms of informing the public about the process”.

What might have been useful to explain was that a marketed offer with a retail tranche would have been a far riskier option; there are reasons why deals like that are rare. The UK government – with a long heritage of retail-targeted privatizations – toyed with the idea of it when it came to sell down the 43% stake it had taken in Lloyds Banking Group during the 2008 crisis but ended up selling via two accelerated bookbuilds and dribbling out the rest through trading plans.

As the UK’s own National Audit Office noted in a 2018 report on the return of Lloyds to private ownership, “a retail offer would expose the government to higher execution risk, incur higher cost and require a substantial discount to market value to be successful”.

Ultimately, though, these are mere technicalities when set against the politics. Once Iceland’s finance minister himself was fielding questions about his own connections to the sale, that was inevitably going to be the focus. The minister’s Independence Party, the largest party in parliament and governing in coalition with the Progressive Party and the Left-Green Movement, will bear the brunt of that.

Opposition politicians have called for an independent inquiry into the sale.

Whatever the eventual impact on Iceland’s reputation in financial markets, suspending privatizations looks like a temporary halt to the globalization of Iceland’s capital markets. This is a sad state of affairs just as the country was anticipating more index upgrades, with FTSE Russell scheduled to confirm by the end of June whether or not Iceland is moving into its Secondary Emerging classification.

And it certainly seems far less likely now that there will be any further sell-downs of state holdings during the current government, whose term runs to 2025.

And for Jón Gunnar, what does the future hold? A former credit banker, he at least now has some ECM experience under his belt, which might be useful if he finds himself looking for a role elsewhere.

Does he know what the plan is for ISFI or what, if anything, might replace it?

A resigned half-smile crosses Euromoney’s laptop. “I have no idea.”