Here’s the good news for private banks: the rich are getting richer, and there are more rich being created. And that means more business for the world’s wealth managers.

Where will you be investing? Global, in 2015 |

|

Source: Euromoney Research Group |

Euromoney asked more than 2,000 private bankers if their bank’s revenues would increase this year: 78% said they would. In north America bankers were even more bullish: 91% said they expected revenues to push higher. But when it comes to profits, it is a different story. Costs are rising faster than revenues can, and profit margins are falling.

Ray Soudah, founder of wealth management M&A adviser Millenium Associates, says: “Despite record stock-market levels, which have trebled in the past five years, revenues at many international private banks, especially Swiss franc-based ones, are still displaying relatively high cost/income ratios, reflecting narrow operating margins.”

UBS Wealth Management’s cost/income ratio was 70.5% for 2014, up from 65.8% in 2012. Credit Suisse’s cost/income ratio in its private banking business at the end of 2014 was 82.5%, up from 74.8% at the end of 2013.

Regulation, compliance and legal costs have seen the largest increases for banks, but not complying is obviously costlier still.

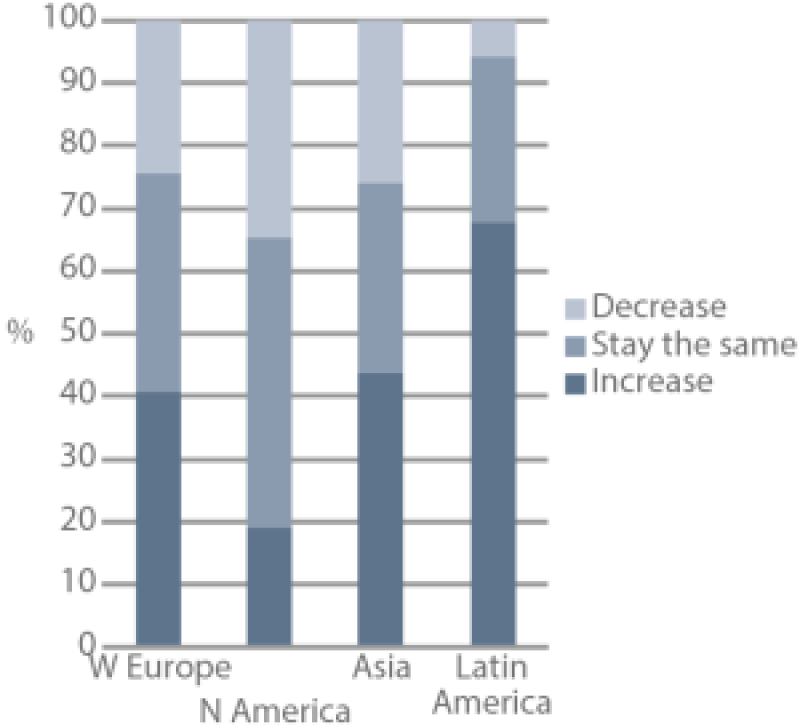

Will the importance of branches in your country change? |

|

Source: Euromoney Research Group |

Seb Dovey, managing partner at wealth management consultants Scorpio Partnership, says: “The perfect storm has now been in place for over five years in terms of cost pressures. The drive for operational efficiencies will require firms to look at how to determine if their personnel are truly delivering a maximized value.” But these pressures are leading private bank chiefs to reconsider their entire cost bases. The use of technology is at the forefront of the discussion. And as private banks invest heavily in apps and other online services for their clients, the question asked across boardrooms is this: can technology replace face-to-face interaction, cutting costs and boosting relationships?

Or to put it another way: is it time to start closing physical branches of private banks?

|

Ray Soudah, founder, |

The answer depends on the state of development of private banking services. Of Latin American respondents to the Euromoney survey, 68% said their firm would increase branches this year. In the more mature North American markets, the majority of respondents said their number of branches would stay the same or decrease.

Don’t write off the value of branches just yet. Société Générale Private Banking, for example, formed a partnership with its retail bank in France and added some €2 billion in assets under management. The branch network played a large role in that.

As part of the partnership, qualifying private-banking clients in the retail bank were asked whether they wanted to stay with their day-to-day branch, with access to all the private bank’s experts, or whether they would prefer to be with a specialized private-banking centre: 95% opted to stay where they were.

“Proximity is key,” says Patrick Folléa, deputy head of Société Générale Private Banking and CEO of the French private bank. “Our private-banking services are now available in the 2,300 branches of the SG branch network in France.”

How does your firm plan to increase profits over 2015? |

|

Source: Euromoney Research Group |

Yet the role of technology cannot be ignored. As Euromoney reported in February, Credit Suisse Private Bank is launching its new digital capabilities this quarter in the Asia-Pacific region, with a global roll-out to follow. Hans-Ulrich Meister, chief executive, told the magazine: “This platform will streamline our existing infrastructure to deliver a sophisticated, cutting-edge multi-channel experience to clients. They will gain closer contact with their relationship managers, who have new tools and resources to meet their evolving needs. They will also be able to easily identify and access information that is important to them from across our integrated bank. For example, clients will be able to access their relationship managers through these new mobile channels and receive market research and portfolio alerts.” In the same issue Phil Di Iorio, CEO of JPMorgan Private Bank, explained that both digital and human interactions are required. “Face-to-face interaction will always be important in the private-banking industry, but clients want more autonomy around basic services,” he said.

“We have started investing in digitizing some of the basic banking services, but that’s the easy part. It’s the enhancements that are challenging.

“The winners in the industry in the next three to five years will be those that provide an adviser-led in-person relationship complemented with digital capabilities. That is going to require significant investment from the industry.”